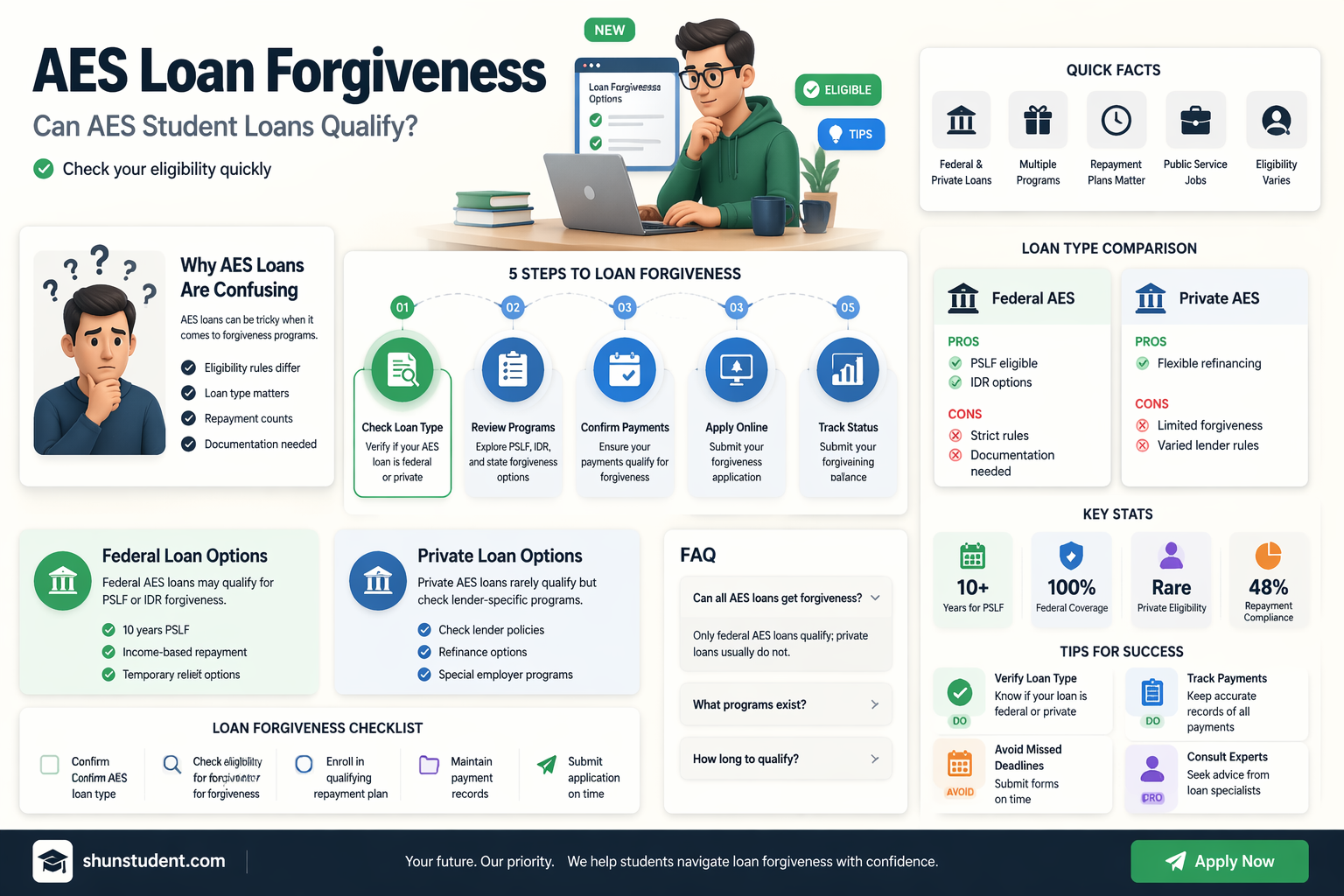

The question of whether AES (American Education Services) student loans are eligible for forgiveness is a critical concern for many borrowers navigating the complexities of student debt relief. AES primarily serves as a loan servicer, managing both federal and private student loans, which means the eligibility for forgiveness largely depends on the type of loan held. Federal student loans serviced by AES may qualify for forgiveness programs such as Public Service Loan Forgiveness (PSLF), income-driven repayment (IDR) forgiveness, or other federal initiatives, provided borrowers meet specific criteria. However, private student loans serviced by AES generally do not qualify for federal forgiveness programs, leaving borrowers with limited options for debt relief. Understanding the distinctions between federal and private loans, as well as the requirements of available forgiveness programs, is essential for AES borrowers seeking to manage or eliminate their student debt effectively.

| Characteristics | Values |

|---|---|

| Loan Type | Private student loans serviced by AES (American Education Services) |

| Eligibility for Forgiveness | Generally not eligible for federal student loan forgiveness programs |

| Exceptions | Possible eligibility for forgiveness through specific lender programs or state-based initiatives |

| Federal Loan Forgiveness Programs | Not applicable (e.g., Public Service Loan Forgiveness, Teacher Loan Forgiveness) |

| Bankruptcy Discharge | Extremely rare and difficult to achieve |

| Lender-Specific Forgiveness | Some private lenders may offer forgiveness or settlement options in cases of hardship or disability |

| State-Based Programs | Limited programs may exist, depending on the state and occupation |

| Refinancing Options | Refinancing with a new lender may provide better terms but does not equate to forgiveness |

| Loan Discharge for Death or Disability | May be available, depending on the lender's policies and loan agreement |

| Current Status (as of 2023) | No widespread forgiveness programs for private AES student loans |

| Recommendation | Contact AES or the loan holder directly to discuss potential options or explore refinancing opportunities |

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Forgiveness

Income-Driven Repayment (IDR) plans offer a lifeline for borrowers struggling to manage their student loan debt, including those with AES-serviced loans. These plans adjust monthly payments based on income and family size, capping them at a percentage of discretionary income (typically 10-20%). After 20 or 25 years of qualifying payments, any remaining balance is forgiven. This forgiveness isn’t automatic; borrowers must stay enrolled in an IDR plan and meet all requirements, including annual recertification of income. For AES borrowers, understanding these plans is crucial, as they provide a structured path toward potential loan forgiveness.

To qualify for IDR forgiveness, borrowers must first enroll in one of four plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), or Income-Contingent Repayment (ICR). Each plan has specific eligibility criteria, such as demonstrating partial financial hardship. For instance, REPAYE is available to all borrowers regardless of income, while PAYE requires loans taken out after October 1, 2007. AES borrowers should carefully review their loan types and disbursement dates to determine the best fit. Once enrolled, consistent, on-time payments are essential, as missed or late payments can reset the forgiveness clock.

A critical but often overlooked aspect of IDR forgiveness is the tax implications. The forgiven amount may be considered taxable income by the IRS, potentially resulting in a significant tax bill. However, under the American Rescue Plan Act of 2021, student loan forgiveness through IDR plans is tax-free until 2025. AES borrowers should consult a tax professional to plan for potential tax liabilities beyond this date. Additionally, keeping detailed records of payments and correspondence with AES can help resolve disputes or discrepancies that may arise during the forgiveness process.

For AES borrowers, navigating IDR forgiveness requires proactive management. Start by submitting income documentation annually to recertify eligibility and adjust payments. Monitor your loan servicer’s communications for updates on policy changes or program requirements. Consider setting up automatic payments to avoid missed deadlines. Finally, track your progress toward forgiveness using tools like the Department of Education’s Loan Simulator. While the journey to forgiveness is lengthy, staying informed and organized can make the process more manageable and increase the likelihood of success.

Student Loan Forgiveness: Essential Steps and Timing for Debt Relief

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF)

To pursue PSLF, borrowers must meet strict criteria. First, they must work full-time for a qualifying employer, such as a government organization, 501(c)(3) nonprofit, or other eligible entities. Second, they must make 120 payments under an income-driven repayment plan, which caps monthly payments based on income and family size. For example, a single borrower earning $40,000 annually might pay as little as $150 per month under the Revised Pay As You Earn (REPAYE) plan. Third, payments must be made on time and in full to count toward the 120-payment requirement.

One common pitfall is assuming all payments made while working in public service qualify. Only payments made *after* October 1, 2007, under a qualifying repayment plan, count toward PSLF. Borrowers should submit the Employment Certification Form (ECF) annually to ensure their employer and payments meet PSLF criteria. This proactive step helps identify issues early, such as incorrect payment counts or ineligible employment, which can derail forgiveness.

For AES borrowers with FFEL loans, consolidation is the first step toward PSLF eligibility. However, consolidating resets the payment count, meaning previously made payments no longer count toward the 120 required. Borrowers must carefully weigh this trade-off, as consolidation can extend the time to forgiveness but is the only path to PSLF for non-Direct Loans. Additionally, consolidating during the CARES Act payment pause (which counts toward PSLF) can maximize qualifying payments.

In conclusion, while PSLF is a powerful tool for AES borrowers, eligibility hinges on loan type, employment, and repayment plan. Borrowers must navigate these requirements carefully, consolidating if necessary and staying vigilant about qualifying payments. With proper planning, PSLF can erase thousands in student debt, offering financial freedom to those committed to public service.

National Guard Service: Unlocking Student Loan Forgiveness Benefits Explained

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Eligibility

Teachers burdened by student loan debt may find relief through the Teacher Loan Forgiveness program, a federal initiative designed to incentivize and support educators in low-income schools. This program offers a unique opportunity for eligible teachers to have a portion of their federal student loans forgiven, providing a significant financial boost to those dedicated to shaping young minds.

Eligibility Criteria: Unlocking the Benefits

To qualify for this program, teachers must meet specific requirements. Firstly, educators must have been employed full-time for five consecutive academic years in a low-income school or educational service agency. This commitment ensures that the program benefits those serving in areas with the greatest need. Additionally, the teacher's role must be as a highly qualified teacher, as defined by the No Child Left Behind Act, ensuring a certain level of expertise and professionalism.

Loan Types and Forgiveness Amounts: A Closer Look

The Teacher Loan Forgiveness program applies to Direct Subsidized and Unsubsidized Loans, as well as Subsidized and Unsubsidized Federal Stafford Loans. The forgiveness amount varies depending on the teacher's subject area and the school's eligibility. For instance, teachers of mathematics, science, or special education in eligible schools can receive up to $17,500 in loan forgiveness, while other eligible teachers may receive up to $5,000. This tiered approach acknowledges the varying demands and challenges of different teaching roles.

Application Process: Navigating the Steps

Applying for Teacher Loan Forgiveness involves several steps. Teachers must submit an application to their loan servicer after completing the required five years of teaching. This application includes certification from the chief administrative officer of the school or agency, verifying the teacher's employment and the school's eligibility. It is crucial to ensure all documentation is accurate and complete to avoid delays or rejections.

A Strategic Approach to Debt Relief

For teachers considering this program, it is essential to plan strategically. This includes choosing the right loan repayment plan during the five-year teaching period, as certain plans may offer lower monthly payments, making it easier to manage debt. Additionally, teachers should stay informed about any changes to the program and explore other forgiveness or repayment options, such as Public Service Loan Forgiveness, to maximize their debt relief potential. By understanding the intricacies of Teacher Loan Forgiveness, educators can make informed decisions to alleviate their financial burden and focus on what matters most—educating the next generation.

Is My Biden Student Loan Forgiven? Understanding the Latest Updates

You may want to see also

Explore related products

![]()

Disability Discharge for AES Loans

Borrowers with AES student loans who experience a permanent disability may qualify for a total and permanent disability (TPD) discharge, a federal program that forgives federal student loans. This option is particularly relevant for AES loans that are federally backed, such as FFEL Program loans. To initiate the process, borrowers must provide documentation proving their disability, typically through the Social Security Administration (SSA), the U.S. Department of Veterans Affairs (VA), or a physician’s certification. Approval results in the complete forgiveness of the loan balance, relieving the borrower of repayment obligations.

The application process for disability discharge involves several steps. First, borrowers must obtain proof of their disability, such as a Notice of Award from the SSA or a VA disability determination. Alternatively, a physician can certify that the borrower is unable to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. Once the documentation is gathered, borrowers submit it to their loan servicer, AES, which reviews the application and determines eligibility. It’s crucial to continue making payments until the discharge is approved to avoid delinquency.

One critical aspect of disability discharge is the post-approval monitoring period. For borrowers approved through SSA or physician certification, a three-year monitoring period follows. During this time, borrowers must provide annual documentation confirming their income does not exceed the poverty guideline for their family size and that their disability status remains unchanged. Failure to comply with these requirements can result in loan reinstatement. VA-approved discharges do not require this monitoring period, offering immediate and permanent relief.

While disability discharge provides significant financial relief, borrowers should be aware of potential tax implications. Before 2018, forgiven amounts were considered taxable income, but the Tax Cuts and Jobs Act temporarily excluded discharged student loans due to disability from taxation through 2025. Borrowers should consult a tax professional to understand their specific obligations. Additionally, discharged loans may impact eligibility for future federal aid, though this is rarely a concern for those with permanent disabilities.

In summary, disability discharge offers a lifeline for AES borrowers facing permanent disabilities, eliminating the burden of student loan debt. By understanding the eligibility criteria, application process, and post-approval requirements, borrowers can navigate this option effectively. While the process requires thorough documentation and adherence to specific guidelines, the long-term relief it provides makes it a valuable resource for those in need.

Can Nonprofit Work Erase Student Debt? Exploring Loan Forgiveness Options

You may want to see also

Explore related products

![]()

Closed School Discharge Criteria

Borrowers with AES student loans may qualify for discharge if their school closed while they were enrolled or shortly after withdrawal. This relief, known as Closed School Discharge, is a federal provision designed to protect students from financial liability when institutional failure disrupts their education. To apply, borrowers must meet specific criteria outlined by the U.S. Department of Education, ensuring the process is both targeted and fair.

First, eligibility hinges on the timing of the school’s closure relative to the borrower’s enrollment. If the school closed while the borrower was actively enrolled, they automatically qualify. Those who withdrew within 120 days of closure are also eligible, provided they did not complete their program. For example, a student who withdrew 90 days before their college shut down would meet this criterion, whereas someone who left 150 days prior would not. Borrowers must submit a discharge application to AES or the loan holder, along with documentation verifying their enrollment status at the time of closure.

Second, borrowers must not have transferred credits to another institution in a similar program. If a student transferred credits and continued their studies elsewhere, they are ineligible for Closed School Discharge. This rule prevents double benefits, ensuring forgiveness is reserved for those whose education was genuinely interrupted. For instance, a nursing student whose credits transferred to another nursing program would not qualify, whereas one whose credits were not accepted would.

Third, borrowers must not have received a discharge for other reasons, such as borrower defense to repayment or bankruptcy. Closed School Discharge is a standalone relief option, and overlapping claims are not permitted. Additionally, borrowers must act promptly; waiting too long to apply may result in denial. AES or the loan holder will review applications on a case-by-case basis, and approved discharges will eliminate the loan balance, including accrued interest and fees.

Finally, borrowers should be aware of potential tax implications. While discharged amounts are generally not considered taxable income under current law, it’s advisable to consult a tax professional for personalized advice. Closed School Discharge offers a critical safety net for AES student loan borrowers, but navigating its criteria requires attention to detail and timely action. By understanding these rules, borrowers can maximize their chances of securing the relief they deserve.

Mastering Student Loan Forgiveness: Avoid Rejection with Proven Strategies

You may want to see also

Frequently asked questions

Yes, AES student loans may be eligible for PSLF if they are federal Direct Loans and meet all program requirements, such as making 120 qualifying payments while working full-time for a qualifying employer.

Yes, if AES services federal student loans enrolled in an IDR plan, borrowers may qualify for loan forgiveness after 20–25 years of qualifying payments, depending on the specific plan.

AES-serviced federal student loans may be eligible for the one-time forgiveness program, but eligibility depends on income limits and the type of federal loan held. Private loans serviced by AES are not eligible.

No, private student loans serviced by AES are not eligible for federal forgiveness programs like PSLF or IDR forgiveness. Only federal student loans qualify for these programs.