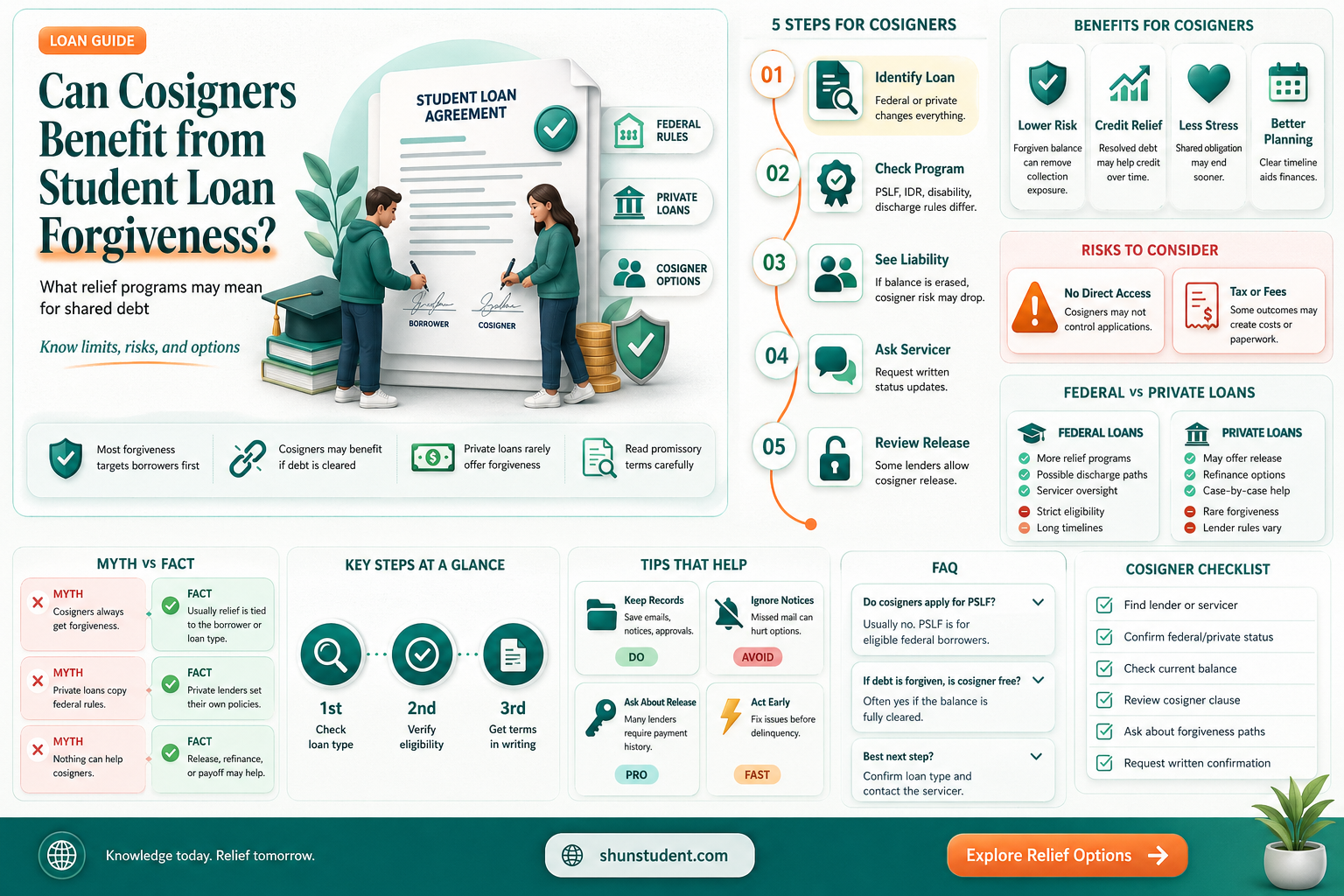

The question of whether cosigners are eligible for student loan forgiveness is a critical concern for many borrowers and their financial supporters. When a cosigner agrees to share responsibility for a student loan, they often wonder if they can benefit from forgiveness programs designed to alleviate the borrower's debt burden. Typically, student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, focus on the primary borrower’s eligibility based on their employment, income, or repayment history. Cosigners, while legally liable for the debt, are generally not considered direct beneficiaries of these programs unless they are also the primary borrower. However, in some cases, if the borrower qualifies for forgiveness, the cosigner’s liability may be extinguished once the debt is discharged. Understanding the nuances of these programs and the role of cosigners is essential for both parties to navigate their financial obligations effectively.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Cosigners are generally not eligible for student loan forgiveness programs. Forgiveness programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or income-driven repayment (IDR) plans apply to the primary borrower, not the cosigner. |

| Responsibility for Debt | Cosigners remain equally responsible for the loan debt unless it is fully repaid or forgiven for the primary borrower. Forgiveness for the primary borrower does not automatically release the cosigner from liability. |

| Exceptions | In rare cases, specific forgiveness programs or settlements might include provisions for cosigners, but these are not standard. For example, certain legal settlements or lender-specific policies may offer relief. |

| Release Options | Cosigners can seek release from the loan through options like cosigner release programs (after a certain number of on-time payments) or refinancing the loan in the primary borrower’s name only. |

| Impact of Forgiveness on Cosigner | If the primary borrower’s loan is forgiven, the cosigner’s credit report will reflect the loan as paid in full, but they are not directly forgiven of any obligation unless explicitly released. |

| Legal Considerations | Cosigners may need to pursue legal avenues or negotiate with lenders for relief if the primary borrower’s loan is forgiven but the cosigner remains liable. |

| Recent Updates (as of 2023) | No widespread changes have been made to include cosigners in federal student loan forgiveness programs. Policies remain focused on primary borrowers. |

Explore related products

What You'll Learn

![]()

Cosigner responsibilities and risks in student loans

Cosigning a student loan is a significant financial commitment that extends beyond moral support. As a cosigner, you’re legally obligated to repay the loan if the primary borrower fails to do so. This responsibility doesn’t vanish if the borrower encounters financial hardship, changes their mind about repayment, or even passes away. Federal student loans, for instance, are discharged upon the borrower’s death, but private loans often require the cosigner to continue payments. Understanding this liability is critical, as it can impact your credit score, debt-to-income ratio, and overall financial stability.

Consider the risks: cosigning ties your creditworthiness to the loan’s performance. Late payments or defaults by the borrower will appear on your credit report, potentially lowering your score and limiting your ability to secure future loans or credit cards. For example, if a $30,000 loan goes into default, the cosigner becomes responsible for the full amount, plus any accrued interest and collection fees. Private lenders may also pursue legal action against cosigners, leading to wage garnishment or asset seizure. These risks highlight the importance of assessing the borrower’s financial reliability before agreeing to cosign.

One common misconception is that cosigners are automatically eligible for student loan forgiveness programs. In reality, most forgiveness options, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, apply only to the primary borrower. Cosigners cannot claim forgiveness benefits unless they assume the loan through consolidation or refinancing in their own name, which removes the original borrower’s obligation. However, this step is rarely straightforward and may require the cosigner to qualify for the loan independently, based on their credit and income.

To mitigate risks, cosigners should establish clear agreements with borrowers. Document expectations for repayment, including monthly contributions and timelines. Encourage the borrower to explore income-driven repayment plans or deferment options if they face financial difficulties. Additionally, consider requesting to be released from the loan once the borrower demonstrates consistent repayment history, typically after 12 to 48 on-time payments, depending on the lender. This proactive approach can protect your financial future while supporting the borrower’s educational goals.

Ultimately, cosigning a student loan is a decision that demands careful consideration. While it can open doors to education for someone in need, the risks to your financial health are substantial. Before committing, evaluate the borrower’s financial discipline, explore alternatives like scholarships or federal loans without cosigner requirements, and consult a financial advisor if necessary. Being informed and cautious ensures you’re prepared for both the responsibilities and potential pitfalls of this arrangement.

Unlocking Student Loan Forgiveness: 10-Year Path to Debt-Free Future

You may want to see also

Explore related products

![]()

Forgiveness programs excluding cosigners' debt relief

Cosigners often face a harsh reality when it comes to student loan forgiveness programs. Despite their significant financial contribution and shared liability, most federal and private forgiveness initiatives explicitly exclude cosigners from debt relief. This exclusion stems from the legal framework of cosigning, where the cosigner is equally responsible for the loan, but not the primary borrower. As a result, forgiveness benefits are typically limited to the borrower, leaving cosigners on the hook for the remaining balance if the borrower qualifies for relief.

Consider the Public Service Loan Forgiveness (PSLF) program, a federal initiative designed to forgive student loans for borrowers who work in qualifying public service jobs after 120 eligible payments. While the borrower’s debt may be wiped clean, the cosigner remains liable for the full amount if the borrower defaults or fails to meet program requirements. Similarly, income-driven repayment (IDR) plans, which offer forgiveness after 20–25 years of payments, do not extend relief to cosigners. This disparity highlights a critical gap in forgiveness programs, leaving cosigners—often parents or relatives—vulnerable to long-term financial strain.

The exclusion of cosigners from debt relief is not merely a technical oversight but a reflection of broader policy priorities. Forgiveness programs are designed to alleviate the burden on borrowers, particularly those in low-income or public service roles, rather than addressing the risks assumed by cosigners. For instance, the recent one-time student loan cancellation initiatives under the Biden administration focused solely on borrowers, disregarding cosigners’ contributions. This approach underscores the need for cosigners to carefully weigh the risks before agreeing to share liability, as their financial exposure remains unchanged even if the borrower receives relief.

Practical steps can mitigate the risks for cosigners, though they do not guarantee relief. First, cosigners should explore options for *cosigner release*, a process available with some private lenders after the borrower makes a certain number of consecutive, on-time payments (typically 12–48 months). Second, cosigners should encourage borrowers to pursue forgiveness programs aggressively, as any reduction in the borrower’s debt indirectly benefits the cosigner by lowering the risk of default. Finally, cosigners should maintain open communication with borrowers about repayment plans and financial stability, ensuring they are aware of their ongoing liability.

In conclusion, while forgiveness programs offer a lifeline to borrowers, they leave cosigners in a precarious position. The exclusion of cosigners from debt relief underscores the need for proactive risk management and informed decision-making before cosigning a loan. Until policies evolve to address this gap, cosigners must navigate the system with caution, leveraging available tools to protect their financial future.

SAVE Program: Unlocking Student Loan Forgiveness Opportunities Explained

You may want to see also

Explore related products

$32.98 $44.99

![]()

Cosigner release options for student loans

Cosigning a student loan is a significant commitment, often undertaken by parents or guardians to help students secure financing for their education. However, many cosigners eventually seek to be released from this obligation to protect their credit and financial future. Fortunately, several cosigner release options exist, though they vary by lender and loan type. Understanding these options is crucial for both cosigners and borrowers to navigate the process effectively.

One common pathway to cosigner release is through consistent on-time payments. Most private student loan lenders require 12 to 48 consecutive months of on-time payments before considering a release. For example, lenders like Sallie Mae and Discover offer release options after 12 months of timely payments, provided the borrower meets credit and income requirements. This approach not only frees the cosigner but also helps the borrower establish a solid credit history. To maximize success, borrowers should set up automatic payments and monitor their credit score to ensure eligibility.

Another option is refinancing the loan in the borrower’s name alone. Refinancing involves taking out a new loan with more favorable terms, often at a lower interest rate, and using it to pay off the original loan. This effectively removes the cosigner from the equation. Platforms like SoFi and CommonBond specialize in student loan refinancing and may approve borrowers with strong credit and stable income. However, refinancing is not without risks; federal loans lose protections like income-driven repayment plans and forgiveness programs when refinanced with a private lender. Borrowers must weigh these trade-offs carefully.

For federal student loans, cosigner release is less common because most federal loans do not require a cosigner. However, if a cosigner is involved through a Direct PLUS Loan, the borrower can pursue a “co-signer release” after making 12 consecutive, on-time payments. Alternatively, the borrower can consolidate the PLUS Loan into a Direct Consolidation Loan and then apply for an income-contingent repayment plan, which may indirectly alleviate the cosigner’s liability over time. It’s essential to note that federal loans do not offer traditional cosigner release like private loans, so borrowers should explore other strategies to protect their cosigner.

Finally, some lenders may consider a cosigner release if the borrower can demonstrate significant financial stability or improved creditworthiness. This might involve providing proof of a higher income, a lower debt-to-income ratio, or a substantial credit score increase. Borrowers should proactively communicate with their lender to understand specific requirements and submit a formal request for release. Documentation, such as recent pay stubs or credit reports, can strengthen the case. While not all lenders offer this flexibility, it’s worth exploring as a potential solution.

In conclusion, cosigner release options for student loans depend on the loan type, lender policies, and the borrower’s financial situation. Whether through consistent payments, refinancing, or demonstrating financial stability, both cosigners and borrowers have pathways to achieve release. Proactive planning, clear communication with lenders, and a thorough understanding of the terms are key to success. By taking these steps, cosigners can protect their financial future while supporting the borrower’s educational journey.

Can Churches Access Federal Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Impact of borrower default on cosigners

Cosigning a student loan is a significant financial commitment, often undertaken by parents or guardians to help students access education funding. However, the repercussions of borrower default extend far beyond the primary borrower, directly impacting cosigners in ways that can be financially devastating. When a borrower defaults, the lender typically turns to the cosigner for repayment, leveraging their creditworthiness to recover the debt. This process can lead to wage garnishment, legal action, and a damaged credit score for the cosigner, even if they were unaware of the borrower’s financial struggles. Understanding these risks is crucial for anyone considering cosigning a loan.

One of the most immediate consequences of borrower default is the damage to the cosigner’s credit score. A single missed payment can drop a credit score by 50 to 100 points, depending on the cosigner’s credit history. Over time, this can limit the cosigner’s ability to secure future loans, credit cards, or even housing. For example, a cosigner with a previously excellent credit score of 800 could see it plummet to the mid-600s, making them ineligible for prime interest rates or certain financial products. This long-term impact underscores the importance of open communication between borrowers and cosigners to prevent default.

Beyond credit damage, cosigners may face aggressive collection tactics from lenders. These can include frequent phone calls, letters, and even lawsuits. In extreme cases, cosigners’ wages can be garnished, with up to 15% of their disposable income redirected to repay the loan. For instance, a cosigner earning $50,000 annually could lose $600 per month, significantly straining their budget. Additionally, if the loan is in private hands, cosigners may be responsible for collection fees, attorney fees, and other costs associated with recovering the debt, further exacerbating their financial burden.

A lesser-known but equally critical impact is the emotional and relational strain default places on cosigners. Many cosigners are family members who cosign out of goodwill, only to find themselves in a contentious situation if the borrower defaults. This can lead to strained relationships, resentment, and even legal disputes within families. For example, a parent who cosigned a loan for their child might feel betrayed if the child stops making payments, creating a rift that extends beyond financial matters. Such outcomes highlight the need for clear agreements and expectations before cosigning.

To mitigate these risks, cosigners should take proactive steps. First, ensure the borrower has a realistic repayment plan and a stable source of income. Second, consider setting up automatic payments to reduce the risk of missed deadlines. Third, explore options like cosigner release, which some lenders offer after a certain number of on-time payments (typically 12 to 36 months). Finally, cosigners should regularly monitor their credit reports to catch any signs of default early. While cosigning can be a helpful tool, it requires careful consideration and ongoing vigilance to avoid becoming collateral damage in the event of borrower default.

Obama Loan Forgiveness: Did Students Receive Reimbursement?

You may want to see also

Explore related products

![]()

Eligibility criteria for cosigner loan forgiveness

Cosigning a student loan is a significant financial commitment, often undertaken by parents or guardians to help students secure funding for their education. However, the question of whether cosigners are eligible for student loan forgiveness is complex and depends on specific eligibility criteria tied to various forgiveness programs. Understanding these criteria is crucial for cosigners seeking relief from this obligation.

Program-Specific Requirements: Eligibility for cosigner loan forgiveness primarily hinges on the type of loan and the forgiveness program in question. For federal student loans, programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans typically focus on the borrower’s eligibility, not the cosigner’s. For instance, PSLF requires the borrower to make 120 qualifying payments while working full-time for a qualifying employer, with no direct benefits extending to cosigners. Similarly, IDR plans forgive remaining balances after 20–25 years of payments, but this forgiveness applies to the borrower’s debt, not the cosigner’s liability.

Private Loan Limitations: Private student loans present even greater challenges for cosigners seeking forgiveness. Unlike federal loans, private lenders rarely offer forgiveness programs, and cosigners remain equally responsible for the debt unless explicitly released by the lender. Some private lenders may offer cosigner release options after the borrower demonstrates a history of on-time payments (typically 12–48 months), but this is not forgiveness—it merely removes the cosigner from the loan obligation.

Exceptional Circumstances: In rare cases, cosigners may find relief through bankruptcy or death/disability discharge. Federal student loans can be discharged if the borrower or cosigner files for bankruptcy and proves undue hardship, though this is difficult to achieve. Additionally, if the borrower dies or becomes permanently disabled, federal loans may be discharged, releasing the cosigner from liability. Private loans, however, often lack these protections unless specified in the loan agreement.

Practical Steps for Cosigners: To mitigate risks, cosigners should explore proactive strategies. First, encourage the borrower to pursue federal forgiveness programs or IDR plans to reduce the overall debt burden. Second, request a cosigner release from private lenders once the borrower meets eligibility criteria. Finally, maintain open communication with the borrower to ensure timely payments and avoid default, which could trigger immediate repayment demands from lenders.

In summary, while cosigners are generally not directly eligible for student loan forgiveness, understanding program specifics and taking proactive steps can help manage their financial exposure. Borrowers and cosigners alike must carefully review loan terms and explore all available options to navigate this complex landscape effectively.

Teacher Loan Forgiveness: A Step-by-Step Guide to Debt Relief

You may want to see also

Frequently asked questions

Cosigners themselves are not eligible for student loan forgiveness programs, as these programs are designed for the primary borrower. However, if the primary borrower qualifies for forgiveness, the loan, including the cosigner's liability, may be discharged.

Yes, if the primary borrower qualifies for student loan forgiveness, the entire loan, including the cosigner's obligation, is discharged. This effectively releases the cosigner from any further liability.

If the loan is forgiven and reported as "paid in full" or "settled," the cosigner’s credit score may improve, as the debt is no longer outstanding. However, any negative history prior to forgiveness (e.g., late payments) may remain on the credit report.

If the borrower defaults, the cosigner becomes fully responsible for repaying the loan. Cosigners are not protected from liability in cases of default and may face collection efforts, credit damage, and legal consequences.