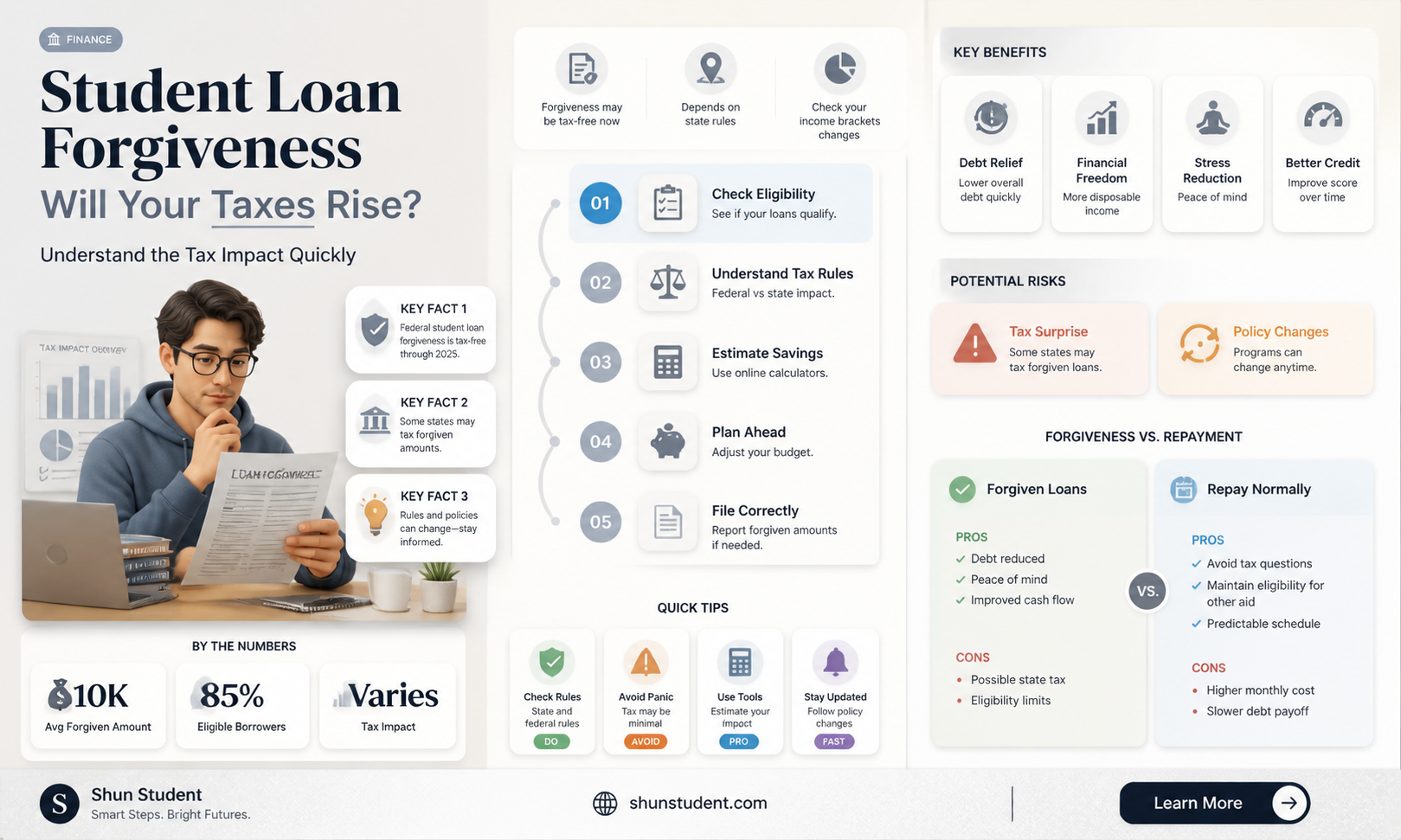

The recent announcement of student loan forgiveness has sparked widespread debate, with many taxpayers wondering if this policy will lead to an increase in their taxes. While the program aims to alleviate the financial burden on millions of borrowers, concerns have arisen regarding its potential impact on the federal budget and, consequently, individual tax liabilities. Proponents argue that the economic benefits of debt relief, such as increased consumer spending and reduced defaults, could offset costs, while critics worry that the government may need to raise taxes or cut other programs to fund the initiative. As the details of implementation and funding mechanisms remain under scrutiny, taxpayers are left to speculate about whether they will ultimately bear the cost of this ambitious policy.

| Characteristics | Values |

|---|---|

| Tax Increase Due to Student Loan Forgiveness | No direct increase in taxes for most individuals. The cost of forgiveness is funded through existing government budgets and deficit spending, not new taxes. |

| Impact on Federal Budget | Estimated cost of $300-$400 billion over 10 years, according to the Congressional Budget Office (CBO). This is offset by reduced loan repayments and interest. |

| Taxpayer Responsibility | General taxpayers indirectly bear the cost through increased national debt, but individual tax rates are not directly raised for this purpose. |

| Income-Driven Repayment Changes | Changes to income-driven repayment plans may reduce future tax liabilities for some borrowers by capping payments and forgiving remaining balances after 10-20 years. |

| Taxability of Forgiven Debt | Under the American Rescue Plan (2021-2025), forgiven student loans are not considered taxable income. |

| State Tax Implications | Some states may treat forgiven student loans as taxable income, depending on state tax laws. |

| Political and Policy Debate | Ongoing debate about fairness and economic impact, but no current proposals to raise taxes specifically for student loan forgiveness. |

| Eligibility for Forgiveness | Up to $20,000 in forgiveness for Pell Grant recipients and $10,000 for non-Pell Grant recipients, based on income limits ($125,000 individual, $250,000 married). |

| Long-Term Economic Effects | Potential boost to consumer spending and economic growth, but also concerns about inflation and long-term fiscal sustainability. |

Explore related products

What You'll Learn

![]()

Impact on federal budget deficit

The federal budget deficit is expected to increase by approximately $400 billion over the next decade due to the student loan forgiveness program, according to the Congressional Budget Office (CBO). This figure, while significant, represents a complex interplay of fiscal policy, economic assumptions, and long-term budgetary impacts. To understand this better, consider that the CBO’s estimate assumes continued economic growth and no additional changes to tax or spending policies. However, if economic conditions worsen or if other costly programs are introduced, the actual impact on the deficit could be larger.

Analyzing the mechanics of this impact reveals that student loan forgiveness effectively shifts a portion of private debt onto the federal balance sheet. This is because forgiven loans are treated as outlays in the federal budget, similar to direct spending programs. For context, the $400 billion estimate is roughly equivalent to 1% of the projected federal budget over the next decade. While this may seem small relative to the total budget, it compounds existing fiscal challenges, such as rising entitlement costs and interest payments on the national debt. Taxpayers, directly or indirectly, bear the burden of this increased deficit through higher taxes, reduced government services, or increased borrowing costs.

A comparative perspective highlights that the cost of student loan forgiveness is less than the $1.9 trillion American Rescue Plan but more than the annual budget for the Department of Education. This places it squarely in the category of significant but not unprecedented fiscal interventions. Critics argue that such spending should be offset by cuts elsewhere or new revenue sources to avoid exacerbating the deficit. Proponents counter that the economic benefits of debt relief, such as increased consumer spending and reduced defaults, could partially offset the cost. However, quantifying these benefits remains challenging, as they depend on behavioral changes that are difficult to predict.

To mitigate the deficit impact, policymakers could consider phased implementation or means-testing for loan forgiveness. For example, limiting eligibility to borrowers below a certain income threshold could reduce the program’s cost while targeting relief to those most in need. Another strategy is to pair forgiveness with reforms to the student loan system, such as income-driven repayment plans or caps on borrowing for graduate programs, to prevent future debt accumulation. Individuals concerned about tax increases should monitor legislative proposals for deficit reduction, such as tax hikes on high earners or corporations, which are often floated as solutions to offset new spending.

In practical terms, the impact on the federal budget deficit translates to a gradual but persistent pressure on fiscal policy. For taxpayers, this could mean higher taxes in the long run, particularly if lawmakers opt for broad-based tax increases to address the deficit. Alternatively, it could lead to cuts in discretionary spending, affecting areas like infrastructure, education, or defense. While the immediate effect on individual taxes may be minimal, the cumulative impact of unchecked deficits poses risks to economic stability, such as inflation or reduced government credibility in financial markets. Staying informed about fiscal policy debates and advocating for sustainable solutions can help individuals navigate these potential consequences.

Can Cosigners Benefit from Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Tax increases for non-borrowers

The debate over student loan forgiveness often centers on fairness, but one overlooked aspect is the potential tax implications for non-borrowers. While borrowers may celebrate debt relief, those who never took out loans or have already paid them off might wonder: will I shoulder the cost through higher taxes? This concern is valid, as government programs are funded by taxpayers, and student loan forgiveness is no exception. However, the extent to which non-borrowers will be affected depends on several factors, including the program’s funding mechanism and broader fiscal policies.

Analyzing the funding structure of student loan forgiveness programs reveals that direct tax increases on individuals are unlikely to be the primary funding source. Instead, governments often rely on reallocating existing funds, deficit spending, or increasing taxes on corporations or high-income earners. For instance, the Biden administration’s 2022 student loan forgiveness plan was funded through the Higher Education Relief Opportunities for Students (HEROES) Act, not through new taxes on the general population. Non-borrowers in lower or middle-income brackets are therefore less likely to see a direct tax increase solely due to forgiveness programs.

That said, indirect economic effects could still impact non-borrowers. If forgiveness programs contribute to increased government debt, it might lead to inflationary pressures or future tax hikes to balance the budget. For example, if the government borrows to fund forgiveness, interest payments on that debt could crowd out other spending priorities, potentially leading to tax increases down the line. Non-borrowers should monitor fiscal policies and inflation trends to gauge long-term implications, as these factors can affect purchasing power and overall financial health.

A comparative perspective highlights that not all forgiveness programs are created equal. In countries like Germany or Norway, where higher education is free or heavily subsidized, taxpayers already contribute to education costs without direct student loans. In the U.S., where loans are prevalent, forgiveness programs shift the burden from borrowers to the broader taxpayer pool, but this shift is often minimal for individual non-borrowers. For instance, if a $10,000 forgiveness program costs $400 billion, the per-taxpayer cost would depend on the number of taxpayers and how the burden is distributed, often resulting in negligible increases for most.

To mitigate concerns, non-borrowers can take proactive steps. First, stay informed about legislative proposals and their funding mechanisms. Second, advocate for transparent fiscal policies that minimize reliance on regressive taxes. Finally, consider the broader societal benefits of student loan forgiveness, such as increased consumer spending and reduced financial stress, which can stimulate economic growth. While non-borrowers may not directly benefit from forgiveness, understanding the nuances of funding and economic impact can alleviate fears of disproportionate tax increases.

Understanding Student Loan Forgiveness: Timeline and Eligibility Explained

You may want to see also

Explore related products

![]()

Inflationary effects on economy

The student loan forgiveness program, while providing much-needed relief to millions of borrowers, has sparked concerns about its potential inflationary impact on the economy. To understand this, let's delve into the mechanics of inflation and how such a policy could influence it.

The Spending Surge: When student loan debt is forgiven, borrowers experience an immediate increase in disposable income. This extra money in their pockets can lead to a surge in consumer spending. Imagine a scenario where a significant portion of the population, previously burdened by loan repayments, now has additional funds to spend on goods and services. This increased demand can put upward pressure on prices, especially in sectors like housing, education, and consumer goods, which are already facing supply constraints. For instance, a recent study by the Federal Reserve suggests that every $100 billion in student debt forgiveness could potentially boost consumer spending by $8 billion annually.

A Comparative Perspective: To put this into context, consider the economic principles behind quantitative easing (QE). Central banks often employ QE to stimulate economies by increasing the money supply, which can lead to inflation if not managed carefully. Similarly, student loan forgiveness injects money into the economy, but instead of directly increasing the money supply, it does so by reducing debt obligations. This indirect approach might have a more targeted effect on specific sectors, but the inflationary consequences could still be significant, especially if the overall economy is already operating near full capacity.

Long-term Implications and Mitigation: The inflationary effects of student loan forgiveness are not just a short-term concern. Over time, sustained increases in demand can lead to persistent inflation if not countered by appropriate monetary policies. Central banks might need to adjust interest rates to curb inflation, which could have broader economic implications. However, it's essential to note that the impact on individual taxpayers might be indirect. While inflation can erode purchasing power, the direct link to increased taxes is not immediate. Tax policies are typically adjusted to account for inflation, ensuring that taxpayers are not disproportionately burdened.

Practical Considerations: For individuals, understanding these economic dynamics can help in financial planning. Borrowers benefiting from loan forgiveness should consider allocating their newfound financial flexibility wisely. Instead of solely increasing consumption, investing in assets that traditionally hedge against inflation, such as real estate or inflation-indexed securities, could be a prudent strategy. Additionally, staying informed about monetary policies and their potential impact on personal finances is crucial for making informed decisions in an evolving economic landscape.

In summary, while student loan forgiveness provides relief to borrowers, its inflationary consequences on the economy warrant careful consideration. The potential surge in consumer spending can lead to price increases, especially in high-demand sectors. However, the direct impact on individual taxes is not immediate, as tax policies are typically adjusted for inflation. Navigating these economic shifts requires a nuanced understanding of monetary policies and their interplay with personal financial decisions.

Student Loan Forgiveness Blocked: Timeline and Potential Resolution

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![]()

State-level tax implications

Student loan forgiveness, while a federal initiative, can have ripple effects on state-level taxes, creating a patchwork of implications across the U.S. Unlike federal taxes, which uniformly exclude forgiven student loans from taxable income through 2025, state tax treatment varies widely. This disparity stems from how states conform to federal tax codes. Some states, like California and New York, fully conform to federal exclusions, meaning forgiven student loans won’t increase your state tax liability. Others, such as North Carolina and Wisconsin, partially conform or decouple entirely, potentially treating forgiven amounts as taxable income. This means residents in these states could face unexpected state tax bills, even if their federal taxes remain unaffected.

To navigate this complexity, taxpayers must first determine their state’s conformity status. For instance, Indiana and Virginia have recently updated their tax codes to align with federal exclusions, offering relief to residents. Conversely, states like Massachusetts and Pennsylvania maintain their own rules, which may not mirror federal treatment. Taxpayers in these states should consult state revenue department guidelines or a tax professional to assess their exposure. For example, if $10,000 in student loans is forgiven, a taxpayer in a non-conforming state with a 5% state tax rate could owe an additional $500 in state taxes.

Another critical factor is the timing of forgiveness. Some states may adopt federal exclusions retroactively, while others may not. For instance, Arkansas passed legislation in 2022 to exclude forgiven student loans from state taxes, but only for forgiveness occurring after January 1, 2022. Taxpayers who received forgiveness prior to this date may still face state tax consequences. This underscores the importance of tracking both federal and state legislative updates, as changes can occur rapidly in response to federal actions.

Practical steps for taxpayers include reviewing state-specific tax forms and instructions, which often clarify how forgiven student loans are treated. For example, Form 540 in California explicitly excludes forgiven student loans, while Wisconsin’s Form 1 requires reporting such income. Additionally, taxpayers should consider estimated tax payments if their state treats forgiven loans as taxable. Failing to account for this could result in penalties and interest on underpaid taxes. Proactive planning, such as setting aside a portion of the forgiven amount for potential state tax liability, can mitigate financial surprises.

In conclusion, while federal student loan forgiveness aims to alleviate financial burdens, its state-level tax implications demand careful attention. Taxpayers must research their state’s conformity status, monitor legislative changes, and take proactive steps to avoid unanticipated tax liabilities. By understanding these nuances, individuals can better navigate the intersection of federal relief and state taxation, ensuring they are fully prepared for any financial impact.

Is DeVry Included in Student Loan Forgiveness Programs? What Borrowers Need to Know

You may want to see also

Explore related products

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![]()

Long-term fiscal sustainability concerns

The Biden administration's student loan forgiveness plan, which aims to cancel up to $20,000 in debt for eligible borrowers, has sparked debates about its long-term fiscal sustainability. While the immediate relief for millions of Americans is undeniable, the program's potential impact on the federal budget and taxpayer obligations warrants careful examination.

Consider the numbers: the Congressional Budget Office (CBO) estimates that the forgiveness plan will cost approximately $400 billion over the next three decades. This substantial expense raises questions about how the government will finance this initiative without exacerbating the national debt. One possible scenario is that the burden may eventually fall on taxpayers, either through direct tax increases or indirect measures like reduced funding for other essential services. For instance, if the government allocates a larger portion of its budget to debt forgiveness, programs like infrastructure development, healthcare, or education might receive less funding, effectively shifting the financial burden to future generations.

A comparative analysis of similar debt relief programs in other countries provides valuable insights. In Australia, the Higher Education Loan Program (HELP) has faced challenges due to the increasing number of borrowers and the rising cost of living. As a result, the Australian government has implemented measures to recover debts more aggressively, including garnishing wages and tax refunds. While the US system differs significantly, this example highlights the potential consequences of unsustainable debt relief policies. To avoid such outcomes, policymakers must explore alternative funding mechanisms, such as allocating a portion of future tax revenues from forgiven loan recipients or introducing targeted tax reforms that minimize the impact on lower-income households.

As the student loan forgiveness plan unfolds, it is crucial for taxpayers to understand the potential trade-offs and long-term implications. A persuasive argument can be made for prioritizing fiscal responsibility while addressing the urgent need for debt relief. One practical approach is to advocate for a means-tested forgiveness program that targets borrowers with the greatest financial need, rather than providing blanket relief. This strategy would not only reduce the overall cost but also ensure that resources are allocated efficiently. Additionally, taxpayers can stay informed by monitoring legislative proposals, such as the potential introduction of a financial transactions tax or adjustments to income tax brackets, which could be used to offset the cost of loan forgiveness.

In the realm of long-term fiscal sustainability, a descriptive analysis of the current economic landscape reveals both opportunities and challenges. With interest rates rising and inflation persisting, the government's borrowing costs are increasing, making it more expensive to finance debt. In this context, the student loan forgiveness plan must be viewed as part of a broader fiscal strategy that balances debt reduction, economic growth, and social welfare. By adopting a nuanced approach that considers the interconnectedness of these factors, policymakers can work towards a solution that alleviates the burden on borrowers without compromising the financial well-being of future generations. This may involve difficult choices, but it is essential for ensuring the long-term viability of the program and the overall health of the economy.

Does American Express Offer Student Loan Forgiveness? What You Need to Know

You may want to see also

Frequently asked questions

No, student loan forgiveness does not directly increase individual taxes. The cost of forgiveness is typically covered through federal spending, not by raising taxes on the general public.

Some states may treat forgiven student loans as taxable income, potentially increasing your state tax liability. However, this varies by state, and federal taxes are not affected.

While it’s possible that future tax policies could change to address federal deficits, there is no direct or immediate plan to raise taxes specifically to fund student loan forgiveness.

Forgiven student loans are generally not considered taxable income at the federal level under current law, so they should not affect your tax bracket or overall federal tax burden. State taxes may differ.

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)