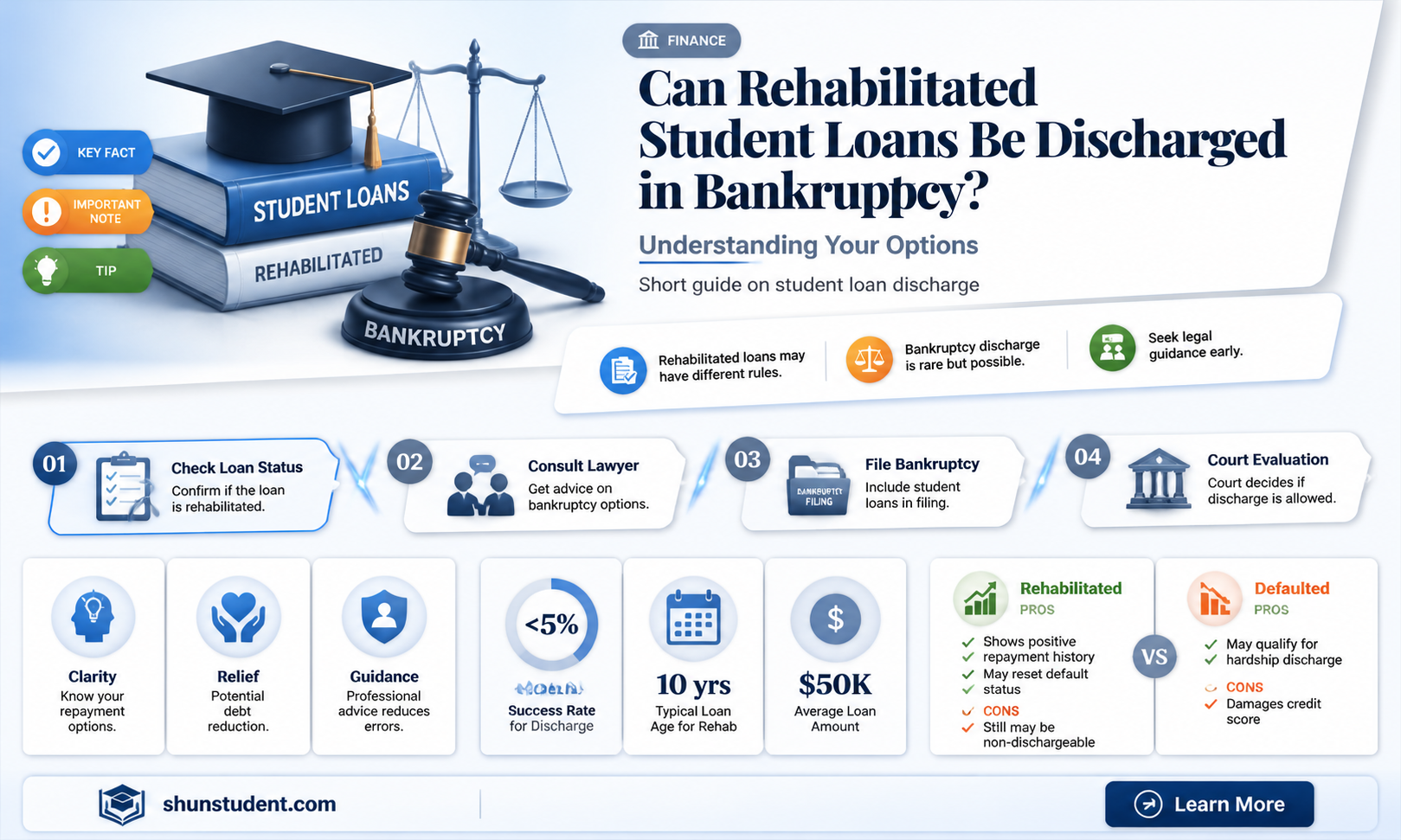

Rehabilitated student loans, which are typically federal loans brought out of default through a structured repayment plan, present a complex scenario when it comes to bankruptcy forgiveness. While most student loans, whether federal or private, are notoriously difficult to discharge in bankruptcy due to the undue hardship standard, rehabilitated loans may have slightly different considerations. Rehabilitated loans regain eligibility for certain benefits, such as access to federal repayment plans and loan forgiveness programs, but they do not automatically become dischargeable in bankruptcy. Borrowers must still meet the stringent criteria of proving undue hardship, which requires demonstrating extreme financial distress and a long-term inability to repay the debt. As a result, while rehabilitation can improve loan management, it does not inherently make these loans eligible for bankruptcy forgiveness, leaving many borrowers to explore alternative solutions for long-term relief.

| Characteristics | Values |

|---|---|

| Eligibility for Bankruptcy Discharge | Rehabilitated student loans are generally not automatically discharged in bankruptcy. They must meet the undue hardship standard, which is difficult to prove. |

| Undue Hardship Requirement | Borrowers must demonstrate extreme financial hardship, inability to repay, and a lack of improvement in their financial situation. |

| Rehabilitation Impact | Loan rehabilitation does not make the loan eligible for bankruptcy discharge unless undue hardship is proven. |

| Bankruptcy Chapter | Applies to both Chapter 7 and Chapter 13 bankruptcies. |

| Legal Process | Requires filing an adversary proceeding in bankruptcy court to request discharge based on undue hardship. |

| Success Rate | Very low success rate due to the stringent undue hardship criteria. |

| Alternative Options | Borrowers may explore income-driven repayment plans or loan forgiveness programs instead of bankruptcy. |

| Rehabilitation Benefits | Removes default status, improves credit, and restores eligibility for federal aid, but does not impact bankruptcy dischargeability. |

| Recent Legal Changes | No significant changes as of 2023; undue hardship remains the primary criterion. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Loan Rehabilitation

Rehabilitating a student loan is a structured process designed to bring defaulted loans back into good standing. To qualify, borrowers must meet specific eligibility criteria, which vary depending on the type of loan and the lender’s policies. For federal student loans, rehabilitation typically requires making nine voluntary, on-time payments within 10 months. These payments are often calculated as 15% of the borrower’s discretionary income, but can be as low as $5 per month if the borrower demonstrates financial hardship. Private loans, however, may have stricter or more flexible terms, often requiring full repayment of past-due amounts or a lump-sum settlement. Understanding these criteria is the first step toward restoring financial stability and potentially regaining eligibility for bankruptcy forgiveness.

The rehabilitation process is not automatic; borrowers must proactively engage with their loan servicer or collection agency to set up a payment plan. This involves submitting documentation to verify income and expenses, which helps determine the affordability of the proposed payments. For federal loans, the servicer will calculate the monthly amount based on the borrower’s adjusted gross income and family size. Private lenders may require a more detailed financial review, including credit history and debt-to-income ratio. Borrowers should be prepared to negotiate terms if the initial proposal is unmanageable, as servicers often have some flexibility to adjust payments to fit the borrower’s budget.

One critical aspect of loan rehabilitation is the impact on credit reporting. Once rehabilitation is complete, the default status is removed from the borrower’s credit report, though the record of late payments remains. This can significantly improve creditworthiness, making it easier to access other forms of credit or financial products. However, borrowers should be aware that rehabilitation does not erase the loan’s history entirely; it simply resets the loan to a current status. For those considering bankruptcy, rehabilitated loans may still be eligible for discharge, but the process is complex and depends on meeting the “undue hardship” standard in court.

A common misconception is that rehabilitation automatically leads to loan forgiveness. While rehabilitated federal loans regain eligibility for income-driven repayment plans and deferment options, they are not forgiven unless the borrower completes a separate forgiveness program, such as Public Service Loan Forgiveness (PSLF). Private loans rarely offer forgiveness options, even after rehabilitation. Borrowers should carefully weigh the long-term implications of rehabilitation versus other strategies, such as loan consolidation or bankruptcy, to determine the best path forward. Consulting a financial advisor or attorney can provide clarity tailored to individual circumstances.

Finally, timing is crucial in the rehabilitation process. Borrowers must act promptly to avoid further consequences of default, such as wage garnishment or tax refund interception. For federal loans, rehabilitation must be completed before the loan is sold to a collection agency or referred for litigation. Private lenders may have shorter windows for negotiation, and delays can result in more aggressive collection efforts. By understanding and meeting the eligibility criteria for rehabilitation, borrowers can take control of their financial future and potentially create a pathway to bankruptcy forgiveness if other options are exhausted.

Capitalized Student Loan Interest Forgiveness Under PSLF: What You Need to Know

You may want to see also

Explore related products

![]()

Bankruptcy Discharge Process for Student Loans

Student loans are notoriously difficult to discharge in bankruptcy, but it’s not impossible. The process hinges on proving "undue hardship," a legal standard that varies by jurisdiction but generally requires demonstrating severe financial distress with no foreseeable improvement. For rehabilitated student loans—those brought out of default through a structured repayment plan—the bankruptcy discharge process remains equally stringent. Rehabilitation itself does not automatically qualify the loan for discharge; instead, it resets the loan’s status, removing default from the borrower’s credit report but leaving the debt intact. Borrowers must still navigate the same legal hurdles to seek relief.

The first step in pursuing bankruptcy discharge for rehabilitated student loans involves filing for either Chapter 7 or Chapter 13 bankruptcy. Chapter 7, a liquidation bankruptcy, typically offers a quicker resolution but requires passing a means test to qualify. Chapter 13, a reorganization bankruptcy, allows borrowers to restructure debts over a 3- to 5-year repayment plan. Regardless of the chapter chosen, borrowers must file an adversary proceeding, a separate lawsuit within the bankruptcy case, specifically targeting the student loan debt. This proceeding is where the undue hardship argument is presented to the court.

Proving undue hardship requires meeting the Brunner Test, a three-pronged standard used in most jurisdictions. First, the borrower must show that maintaining a minimal standard of living is impossible if forced to repay the loan. Second, this financial hardship must be expected to persist for most of the loan’s repayment period. Third, the borrower must have made good-faith efforts to repay the loan. For rehabilitated loans, evidence of consistent payments post-rehabilitation can strengthen the good-faith argument, but it does not guarantee success. Courts scrutinize income, expenses, employment prospects, and even health conditions to assess the borrower’s situation.

Practical tips for navigating this process include gathering comprehensive financial documentation, such as tax returns, pay stubs, medical bills, and loan statements. Consulting a bankruptcy attorney experienced in student loan cases is crucial, as they can tailor arguments to the specific circumstances and jurisdiction. Borrowers should also consider alternative relief options, such as income-driven repayment plans or loan forgiveness programs, if bankruptcy discharge seems unlikely. While rehabilitated loans do not receive special treatment in bankruptcy, understanding the process and preparing thoroughly can improve the chances of a favorable outcome.

In conclusion, the bankruptcy discharge process for rehabilitated student loans is complex and demanding. Rehabilitation resets the loan’s status but does not alter the stringent requirements for discharge. Borrowers must file an adversary proceeding, meet the undue hardship standard, and provide robust evidence of their financial plight. While success is not guaranteed, strategic preparation and professional guidance can make a significant difference in achieving relief from this burdensome debt.

Colorado's Potential Tax on Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Undue Hardship Requirements in Bankruptcy

Rehabilitated student loans, while no longer in default, still carry significant weight in bankruptcy proceedings. The key hurdle? Proving "undue hardship," a stringent standard that demands more than mere financial inconvenience. This legal doctrine, rooted in the Bankruptcy Code, acts as a gatekeeper, ensuring student loan debt isn't discharged lightly.

Understanding the undue hardship test is crucial for anyone seeking bankruptcy relief from rehabilitated student loans. It's a three-pronged evaluation, known as the Brunner test, requiring borrowers to demonstrate:

- Inability to Maintain a Minimal Standard of Living: This goes beyond temporary belt-tightening. It means proving that repaying the loan, even in part, would force you and your dependents into a life of poverty, lacking basic necessities like food, shelter, clothing, and healthcare.

- Persistence of Circumstances: Your financial hardship can't be a temporary setback. You must show that your inability to repay is likely to continue for a significant portion of the loan repayment period. This could be due to chronic illness, disability, lack of employable skills, or a persistently low-paying career path.

- Good Faith Effort to Repay: Even if your situation is dire, courts scrutinize your past efforts to repay. This includes making payments when possible, exploring income-driven repayment plans, and seeking loan consolidation or rehabilitation options.

Meeting all three prongs is a high bar. Courts are hesitant to discharge student loans, viewing them as investments in future earning potential. However, for those facing genuine, long-term financial distress, the undue hardship test offers a potential path to relief.

Is DeVry Included in Student Loan Forgiveness Programs? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Impact of Loan Rehabilitation on Bankruptcy

Rehabilitated student loans, while a lifeline for many borrowers, do not automatically qualify for discharge in bankruptcy. This is a critical distinction borrowers must understand. Loan rehabilitation, a process involving nine on-time payments over ten consecutive months, removes the loan from default status and restores eligibility for benefits like deferment, forbearance, and income-driven repayment plans. However, it does not erase the loan's history or its classification as a student loan, which remains subject to the stringent discharge standards outlined in the Bankruptcy Code.

The impact of rehabilitation on bankruptcy proceedings is twofold. Firstly, it demonstrates a borrower's good faith effort to repay the debt, which can be a factor in an undue hardship claim. Under the Brunner test, used in most jurisdictions, borrowers must prove that repaying the loan would cause undue hardship, that this hardship will persist, and that they have made good faith efforts to repay. Rehabilitation can strengthen the "good faith" prong of this test, potentially improving the chances of a successful undue hardship claim. However, it is not a guarantee, as the overall burden of proof remains high.

Secondly, rehabilitation may influence the court's perception of the borrower's financial situation. By successfully rehabilitating a loan, borrowers show they can manage payments, which could undermine arguments that repayment is an insurmountable burden. This underscores the importance of strategic timing: borrowers considering bankruptcy should weigh the benefits of rehabilitation against its potential to complicate a future undue hardship claim. Consulting with a bankruptcy attorney before initiating rehabilitation can help align these efforts with long-term financial goals.

Practical tips for borrowers include documenting all rehabilitation payments and communications with loan servicers, as this evidence can support a good faith argument in court. Additionally, exploring alternative repayment plans, such as income-driven options, before or after rehabilitation can provide a more sustainable path to managing debt outside of bankruptcy. While rehabilitation does not directly enable student loan discharge in bankruptcy, it can be a strategic step in a broader financial recovery plan, provided borrowers navigate its implications carefully.

Is Student Loan Forgiveness a Real Possibility for Borrowers?

You may want to see also

Explore related products

![]()

Alternatives to Bankruptcy for Loan Relief

Rehabilitated student loans, while not automatically discharged in bankruptcy, offer a pathway to financial recovery through alternative relief options. These alternatives focus on restructuring payments, reducing interest, or negotiating settlements, providing borrowers with manageable solutions without the long-term consequences of bankruptcy. Here’s a focused guide to navigating these options effectively.

Income-Driven Repayment Plans: Tailoring Payments to Your Earnings

For federal student loans, income-driven repayment (IDR) plans adjust monthly payments based on income and family size. Plans like Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) cap payments at 10-20% of discretionary income. After 20-25 years of consistent payments, the remaining balance is forgiven, though forgiven amounts may be taxed. For example, a borrower earning $40,000 annually with $50,000 in loans might see payments drop from $500 to $200 monthly under REPAYE. Caution: Private loans are ineligible for IDR, and enrolling requires annual recertification of income.

Loan Consolidation: Simplifying Multiple Debts

Consolidating multiple federal loans into a Direct Consolidation Loan streamlines payments into a single bill and may lower monthly payments by extending the repayment term up to 30 years. This option is particularly useful for rehabilitated loans, as it resets the loan’s status, potentially improving eligibility for IDR plans or Public Service Loan Forgiveness (PSLF). However, consolidating can restart the forgiveness clock, so weigh the long-term interest costs against immediate payment relief.

Loan Forgiveness Programs: Targeted Relief for Specific Careers

Programs like PSLF offer tax-free forgiveness after 10 years of qualifying payments for borrowers working in government or nonprofit sectors. Similarly, Teacher Loan Forgiveness provides up to $17,500 in relief for educators in low-income schools. Private loans are ineligible, but borrowers can refinance into federal loans to qualify. Pro tip: Certify employment annually to ensure payments count toward forgiveness, even if not yet eligible.

Negotiating Settlements: A Last Resort for Private Loans

Private lenders may accept lump-sum settlements for less than the total owed, particularly if the borrower demonstrates financial hardship. For instance, a $30,000 private loan might settle for $15,000 if the borrower can prove inability to pay. This approach damages credit but avoids bankruptcy. Always get settlement terms in writing and verify the debt is reported as “paid in full” afterward.

While rehabilitated student loans remain challenging to discharge in bankruptcy, these alternatives provide viable paths to relief. By leveraging IDR plans, consolidation, forgiveness programs, or settlements, borrowers can address debt without the stigma and long-term credit impact of bankruptcy. Each option requires careful consideration of eligibility, costs, and long-term goals, but with strategic planning, financial stability is achievable.

Can Student Loan Forgiveness Face Legal Challenges in Court?

You may want to see also

Frequently asked questions

Rehabilitated student loans are still considered federal student loans and generally remain ineligible for discharge through bankruptcy unless the borrower can prove "undue hardship" under the Brunner Test. Rehabilitation does not change their status in bankruptcy proceedings.

Rehabilitation removes the default status but does not make the loans eligible for automatic bankruptcy forgiveness. The borrower must still meet the stringent "undue hardship" criteria to have them discharged in bankruptcy.

Rehabilitation does not directly improve the chances of bankruptcy forgiveness. The eligibility for discharge still depends on meeting the "undue hardship" standard, regardless of the loan’s rehabilitation status.