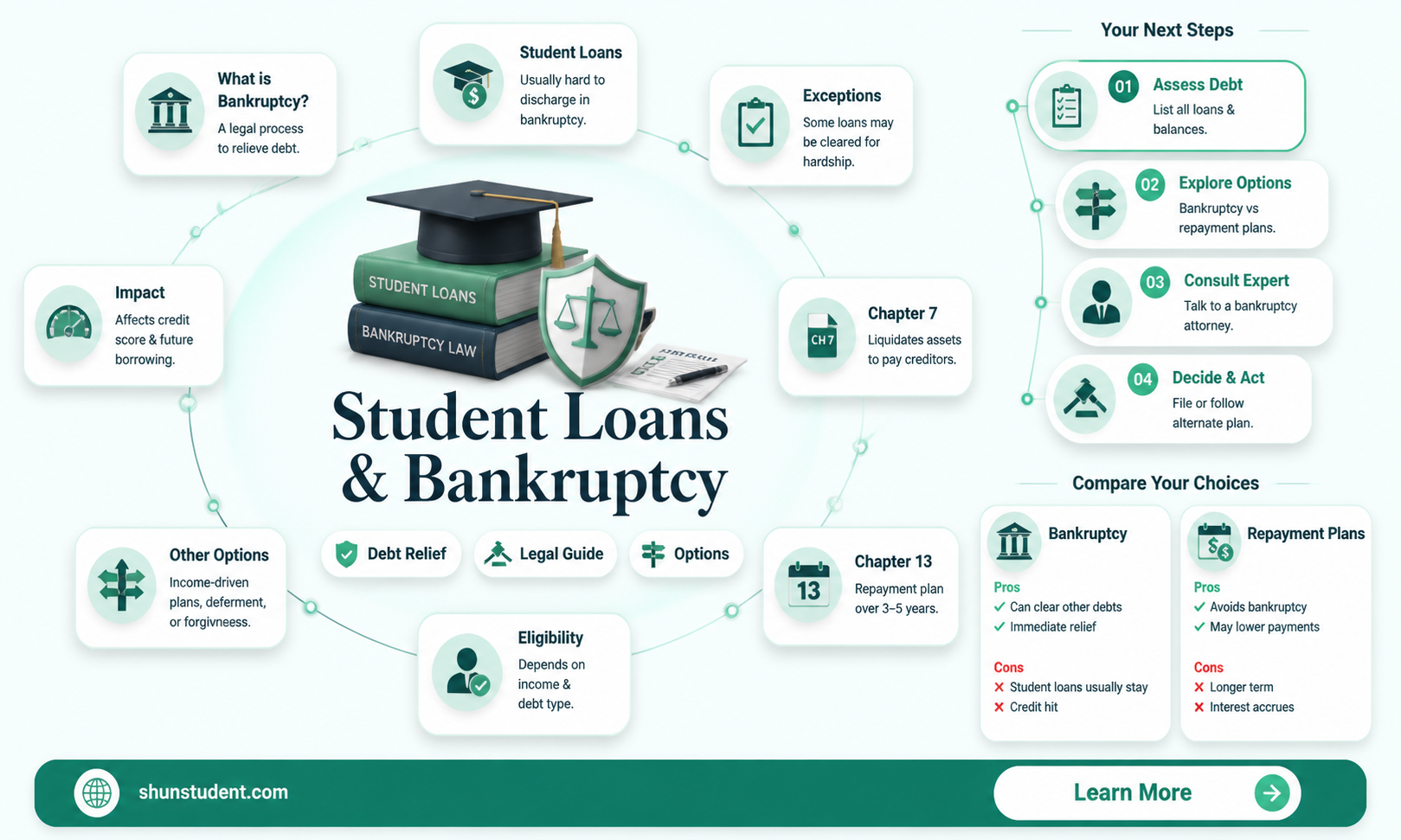

Student loan debt has become a significant financial burden for millions of Americans, and many borrowers wonder if bankruptcy can offer a solution. While bankruptcy is designed to provide a fresh start for individuals overwhelmed by debt, discharging student loans through this process is notoriously difficult. Under current U.S. law, student loans are generally considered non-dischargeable unless the borrower can prove undue hardship, a stringent standard that requires demonstrating extreme financial distress with little likelihood of improvement. This high bar means that only a small fraction of borrowers successfully eliminate their student loans through bankruptcy. As a result, many are left seeking alternative relief options, such as income-driven repayment plans or loan forgiveness programs, to manage their debt.

| Characteristics | Values |

|---|---|

| Eligibility for Discharge | Extremely rare; requires proving "undue hardship" under the Brunner Test. |

| Brunner Test Criteria | 1. Cannot maintain minimal living standard if forced to repay. |

| 2. Circumstances unlikely to change. | |

| 3. Made good-faith effort to repay. | |

| Chapter 7 Bankruptcy | May discharge other debts but rarely student loans. |

| Chapter 13 Bankruptcy | Can restructure payments but does not discharge student loans. |

| Federal vs. Private Loans | Both federal and private loans are treated similarly under bankruptcy. |

| Recent Legal Changes | No significant changes; undue hardship remains the primary standard. |

| Alternative Options | Loan forgiveness programs, income-driven repayment plans, or settlements. |

| Success Rate | Less than 1% of bankruptcy filers successfully discharge student loans. |

| Legal Representation | Required for "adversary proceeding" to challenge student loan discharge. |

| Impact on Credit Score | Bankruptcy negatively impacts credit; student loans remain on credit report. |

| Time Frame | Lengthy process due to court proceedings and adversary hearings. |

| Documentation Required | Extensive financial records, medical evidence, and repayment history. |

| Appeals Process | Possible but rarely successful due to strict undue hardship standards. |

| State Variations | No significant state-level differences in bankruptcy treatment of student loans. |

Explore related products

What You'll Learn

- Eligibility Criteria: Specific conditions required for student loan discharge in bankruptcy cases

- Undue Hardship Test: Legal standard to prove inability to repay student loans

- Chapter 7 vs. Chapter 13: Differences in handling student loans under bankruptcy chapters

- Adversary Proceedings: Court process to challenge student loan dischargeability

- Alternatives to Bankruptcy: Forgiveness programs and repayment plans outside bankruptcy

![]()

Eligibility Criteria: Specific conditions required for student loan discharge in bankruptcy cases

Student loans are notoriously difficult to discharge in bankruptcy, but it’s not impossible. The key lies in meeting the stringent eligibility criteria outlined in the Bankruptcy Code. Specifically, borrowers must prove "undue hardship" through an adversary proceeding, a separate lawsuit within the bankruptcy case. This process requires demonstrating that repaying the loans would impose an insurmountable financial burden, preventing even a minimal standard of living. Courts evaluate this using tests like the Brunner Test, which assesses inability to maintain basic needs, the likelihood of persistent hardship, and good-faith efforts to repay.

To initiate this process, borrowers must file a complaint with the bankruptcy court, detailing their financial situation and why repayment constitutes undue hardship. Documentation is critical—gather evidence such as medical records, employment history, and budget statements to support your case. While success rates are low, certain circumstances, like permanent disability or long-term unemployment, strengthen the argument. For instance, individuals over 50 with limited job prospects or those with chronic illnesses may have a more compelling case.

It’s essential to understand that not all student loans qualify for discharge. Private loans often face stricter scrutiny compared to federal loans, though both require the same undue hardship standard. Additionally, bankruptcy does not automatically discharge student loans; borrowers must actively seek this relief through the adversary proceeding. Consulting an attorney specializing in bankruptcy and student loan law is highly recommended, as they can navigate the complexities and improve the chances of a favorable outcome.

Finally, while bankruptcy offers a potential path to student loan discharge, it’s a last resort with long-term financial implications. Filing for bankruptcy affects credit scores for up to 10 years, limiting access to credit, housing, and employment opportunities. Borrowers should explore alternatives like income-driven repayment plans, loan forgiveness programs, or settlements with private lenders before pursuing this route. Discharging student loans in bankruptcy is rare but possible for those who meet the strict eligibility criteria and are prepared for the legal and financial challenges ahead.

College Misconduct? How to Secure Student Loan Forgiveness for Improper Practices

You may want to see also

Explore related products

![]()

Undue Hardship Test: Legal standard to prove inability to repay student loans

Student loans are notoriously difficult to discharge in bankruptcy, but it’s not impossible. The key lies in proving "undue hardship," a legal standard so stringent that it often feels like an uphill battle. This test, rooted in the Bankruptcy Code, requires debtors to demonstrate that repaying their student loans would impose an insurmountable financial burden, leaving them unable to maintain even a minimal standard of living. Unlike other debts, student loans are presumed nondischargeable, shifting the burden of proof entirely onto the borrower.

The undue hardship test is typically evaluated using the Brunner Test, a three-pronged framework adopted by most courts. First, the debtor must show that maintaining a minimal standard of living is impossible if forced to repay the loans. This isn’t about luxury—it’s about basic necessities like food, housing, and healthcare. Second, the debtor must prove that their financial situation is unlikely to improve in the future. Age, health, job prospects, and education level are all considered here. Third, the debtor must demonstrate good faith efforts to repay the loans, such as enrolling in income-driven repayment plans or making partial payments. Failing to meet any one prong means the loans remain undischarged.

Consider the case of *Brunner v. New York State Higher Education Services Corp.*, the landmark decision that established this test. The debtor, a single mother with limited income and no prospect of higher earnings, successfully argued that her student loans constituted undue hardship. However, such victories are rare. Courts interpret the Brunner Test narrowly, often siding with lenders unless the debtor’s circumstances are exceptionally dire. For instance, a 55-year-old with chronic illness, no savings, and minimal Social Security income might stand a chance, but a 30-year-old with entry-level job prospects likely wouldn’t.

To navigate this process, debtors should gather comprehensive documentation: medical records, employment history, budget statements, and loan repayment efforts. Consulting a bankruptcy attorney specializing in student loan cases is crucial, as they can tailor arguments to meet the Brunner Test’s strict criteria. While the undue hardship test is daunting, it’s not insurmountable. For those truly trapped in a cycle of debt and despair, it remains the only viable path to relief.

In practice, fewer than 1% of student loan debtors who file for bankruptcy attempt to prove undue hardship, and even fewer succeed. Yet, for those facing lifelong financial ruin, it’s a battle worth fighting. The takeaway? The undue hardship test is a high bar, but with meticulous preparation and a compelling case, some borrowers can break free from the chains of student debt.

Can Private Student Loans Be Forgiven? Exploring Options and Realities

You may want to see also

Explore related products

![]()

Chapter 7 vs. Chapter 13: Differences in handling student loans under bankruptcy chapters

Student loans are notoriously difficult to discharge in bankruptcy, but the process differs significantly between Chapter 7 and Chapter 13 filings. Understanding these differences is crucial for borrowers seeking relief from overwhelming educational debt. Chapter 7, often called liquidation bankruptcy, requires debtors to pass a means test and typically results in the sale of non-exempt assets to pay creditors. However, student loans are treated as non-dischargeable unless the debtor can prove "undue hardship," a stringent standard rarely met. In contrast, Chapter 13, a reorganization bankruptcy, allows debtors to restructure their debts over a 3- to 5-year repayment plan. While student loans still aren’t dischargeable, Chapter 13 provides temporary relief by pausing collections and including student loan payments in the plan, potentially lowering monthly obligations.

To illustrate, consider a debtor with $50,000 in student loans and $20,000 in credit card debt. Under Chapter 7, the credit card debt might be discharged, but the student loans remain unless undue hardship is proven. In Chapter 13, the debtor could propose a plan that prioritizes paying off higher-interest credit card debt while making reduced payments on the student loans during the plan period. This approach doesn’t eliminate the student loans but provides breathing room to manage other debts. The key takeaway here is that Chapter 13 offers more flexibility in handling student loans, even if it doesn’t discharge them outright.

Proving undue hardship in either chapter is a high bar, requiring debtors to demonstrate extreme financial distress, long-term inability to repay, and good-faith efforts to repay the loans. Courts use the Brunner Test, which evaluates whether the debtor cannot maintain a minimal standard of living, if the hardship is likely to persist, and if the debtor has made good-faith efforts to repay. For example, a 45-year-old debtor with permanent disabilities and no prospect of increased income might meet this standard, but a recent graduate with entry-level income likely would not. This underscores the rarity of student loan discharge in bankruptcy, regardless of the chapter filed.

Practically speaking, debtors should consult an attorney to assess their eligibility for undue hardship and weigh the pros and cons of Chapter 7 versus Chapter 13. For instance, Chapter 7 is faster, typically lasting 3–6 months, but requires asset liquidation, while Chapter 13 takes years but allows debtors to retain property. Additionally, Chapter 13 can stop wage garnishments and provide a structured path to financial stability, even if student loans remain. Borrowers should also explore alternatives like income-driven repayment plans or loan forgiveness programs, which may offer more viable solutions outside of bankruptcy.

In conclusion, while neither Chapter 7 nor Chapter 13 guarantees student loan discharge, Chapter 13 provides more tools to manage these debts during the bankruptcy process. Debtors must carefully evaluate their financial situation, consult legal counsel, and consider all available options to make an informed decision. The goal isn’t necessarily to eliminate student loans but to create a manageable path forward in the face of overwhelming debt.

Is Biden's Student Debt Forgiveness Plan Legally Sound?

You may want to see also

Explore related products

![]()

Adversary Proceedings: Court process to challenge student loan dischargeability

Student loans are notoriously difficult to discharge in bankruptcy, but it’s not impossible. One pathway borrowers can pursue is an adversary proceeding, a formal court process within the bankruptcy case to challenge the dischargeability of student loans. This process requires proving "undue hardship" under the Brunner Test, a three-pronged standard used in most jurisdictions. While the bar is high, understanding the steps, challenges, and potential outcomes of adversary proceedings can empower borrowers to make informed decisions.

The first step in an adversary proceeding is filing a complaint with the bankruptcy court. This document outlines the borrower’s argument for undue hardship, supported by evidence such as medical records, income statements, and expense documentation. The lender (usually the U.S. Department of Education or a private loan servicer) then has the opportunity to respond, often contesting the claim. This back-and-forth sets the stage for a trial, where both parties present their cases before a judge. Borrowers should be prepared for a lengthy and costly process, as legal fees and court expenses can quickly accumulate.

One critical aspect of adversary proceedings is the Brunner Test, which requires borrowers to meet three criteria: (1) they cannot maintain a minimal standard of living if forced to repay the loans, (2) their financial situation is likely to persist, and (3) they have made good-faith efforts to repay the loans. Meeting these standards is challenging, as courts interpret them strictly. For example, a borrower with a chronic illness and no prospect of increased income might satisfy the first two prongs but could still fail if they haven’t explored income-driven repayment plans or made partial payments. Practical tip: Document every attempt to repay the loans and gather detailed evidence of financial hardship to strengthen your case.

Comparatively, adversary proceedings are riskier than other bankruptcy options but offer a unique opportunity for complete discharge. Chapter 7 and Chapter 13 bankruptcies may provide temporary relief through automatic stays, but they rarely eliminate student loans entirely. In contrast, a successful adversary proceeding can result in full discharge, freeing the borrower from the debt burden permanently. However, the success rate is low—only about 40% of cases result in partial or full discharge—so borrowers must weigh the potential benefits against the financial and emotional toll of litigation.

In conclusion, adversary proceedings are a high-stakes, last-resort option for borrowers seeking to discharge student loans in bankruptcy. While the process is demanding and outcomes uncertain, it remains a viable pathway for those facing insurmountable financial hardship. Borrowers should consult with an experienced bankruptcy attorney to evaluate their eligibility, prepare a robust case, and navigate the complexities of the court system. With careful planning and persistence, some borrowers may find relief from the crushing weight of student debt.

Does Sallie Mae Offer Student Loan Forgiveness? What You Need to Know

You may want to see also

Explore related products

![]()

Alternatives to Bankruptcy: Forgiveness programs and repayment plans outside bankruptcy

Student loan debt can feel like an insurmountable burden, and bankruptcy often seems like the only escape hatch. However, discharging student loans through bankruptcy is notoriously difficult, requiring proof of "undue hardship" – a high bar to clear. Before resorting to this extreme measure, explore the surprisingly robust landscape of forgiveness programs and repayment plans designed to alleviate the strain.

Public Service Loan Forgiveness (PSLF): A Commitment Rewarded

For those dedicated to public service, PSLF offers a beacon of hope. This program forgives the remaining balance on Direct Loans after 120 qualifying payments (10 years) while working full-time for a qualifying employer, such as government organizations, non-profits, or certain public service entities. Teachers, social workers, and healthcare professionals often find this path particularly beneficial. Remember, meticulous record-keeping and annual certification of employment are crucial for success.

Income-Driven Repayment (IDR) Plans: Tailoring Payments to Your Reality

IDR plans adjust your monthly payments based on your income and family size, making them more manageable. Plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) cap payments at a percentage of your discretionary income, typically 10-20%. After 20-25 years of consistent payments, any remaining balance is forgiven. While this forgiveness is taxable as income, it provides a realistic path to debt relief for borrowers with limited means.

Teacher Loan Forgiveness: A Thank You to Educators

Teachers who serve in low-income schools for five consecutive years can qualify for up to $17,500 in loan forgiveness. This program recognizes the dedication of educators in underserved communities and provides a financial incentive to continue their vital work.

Exploring Other Options: State and Employer Programs

Many states offer loan repayment assistance programs (LRAPs) for professionals in high-demand fields like healthcare, law, and education. Additionally, some employers provide student loan repayment benefits as part of their compensation packages. Researching these opportunities can uncover hidden gems of financial support.

Beyond Forgiveness: Refinancing and Consolidation

While not forgiveness, refinancing and consolidation can significantly reduce monthly payments and interest rates. Refinancing replaces your existing loans with a new private loan, ideally at a lower interest rate. Consolidation combines multiple federal loans into one, simplifying repayment and potentially lowering monthly payments. However, be cautious: refinancing federal loans with a private lender means losing access to federal forgiveness programs and protections.

Student Loan Forgiveness Update: Did the Relief Plan Pass?

You may want to see also

Frequently asked questions

It is extremely difficult to discharge student loans through bankruptcy. Under the U.S. Bankruptcy Code, student loans are generally not dischargeable unless the borrower can prove "undue hardship," which is a very high legal standard to meet.

The "undue hardship" test typically requires the borrower to prove that repaying the student loans would cause them and their dependents to live in poverty, that their financial situation is unlikely to improve, and that they have made good faith efforts to repay the loans. This test varies by jurisdiction but is rarely successful.

Yes, there are federal programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment (IDR) plans that can lead to loan forgiveness after meeting specific criteria. Additionally, some states and employers offer student loan repayment assistance programs. These options are separate from bankruptcy and may provide relief for eligible borrowers.