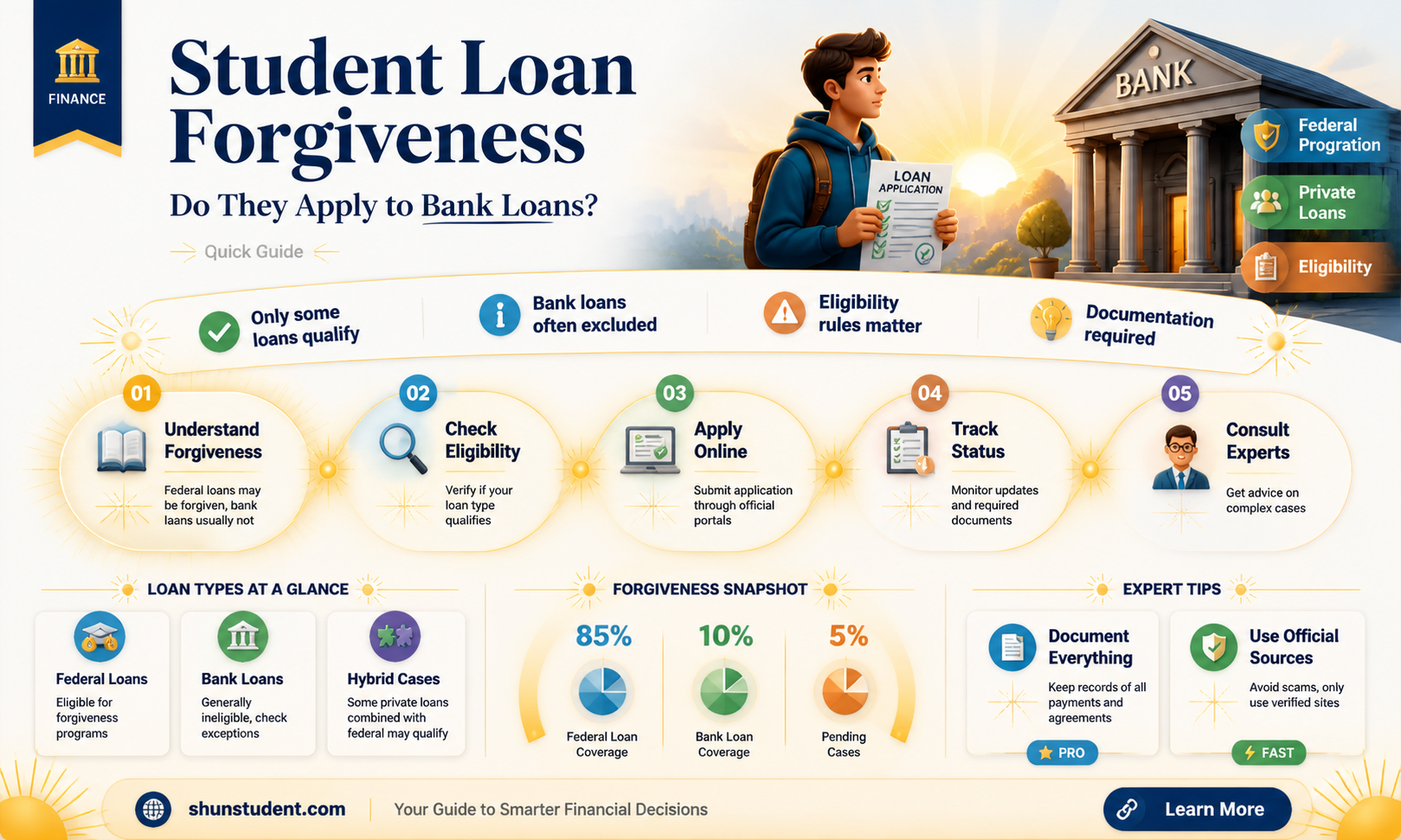

The topic of student loan forgiveness programs often raises questions about their applicability to bank loans, as many borrowers wonder if such initiatives can alleviate their financial burdens. While student loan forgiveness programs are primarily designed to address federal student loans, their relationship with bank loans is less direct. Typically, private student loans issued by banks are not eligible for federal forgiveness programs, as these initiatives are funded by the government and focus on loans held by the Department of Education. However, some states or private organizations may offer assistance programs that include provisions for private loans, though these are less common and often come with specific eligibility criteria. Understanding the distinctions between federal and private loans is crucial for borrowers seeking relief, as it clarifies which programs they can access and what steps they need to take to manage their debt effectively.

Explore related products

What You'll Learn

- Eligibility Criteria: Income limits, loan types, repayment plans, employment requirements, and application deadlines for forgiveness

- Public Service Loan Forgiveness (PSLF): Requirements, qualifying employers, certification process, and forgiveness after 120 payments

- Income-Driven Repayment Forgiveness: Plan options, payment calculations, forgiveness timelines, and tax implications

- Teacher Loan Forgiveness: Eligibility, teaching requirements, award amounts, and application process for educators

- Loan Discharge Options: Disability, school closure, borrower defense, and total permanent disability discharge criteria

![]()

Eligibility Criteria: Income limits, loan types, repayment plans, employment requirements, and application deadlines for forgiveness

Student loan forgiveness programs often hinge on strict eligibility criteria, and understanding these requirements is crucial for borrowers seeking relief. Income limits are a cornerstone of many forgiveness programs, particularly income-driven repayment (IDR) plans. For instance, the Revised Pay As You Earn (REPAYE) plan caps monthly payments at 10% of discretionary income, with forgiveness available after 20–25 years of qualifying payments. Borrowers must annually recertify their income and family size to remain eligible, ensuring payments adjust to their financial situation. Exceeding the income threshold can disqualify applicants, making it essential to monitor earnings and plan accordingly.

Not all loan types qualify for forgiveness, creating a significant barrier for some borrowers. Federal loans, such as Direct Loans and FFEL Program loans, are typically eligible, while private bank loans are almost always excluded. For example, the Public Service Loan Forgiveness (PSLF) program requires borrowers to have Direct Loans or consolidate other federal loans into the Direct Loan program. Borrowers with Perkins Loans or private bank loans must first consolidate into a Direct Consolidation Loan to qualify, a step often overlooked. Understanding loan type eligibility is the first step in determining whether forgiveness is even a possibility.

Repayment plans play a pivotal role in forgiveness eligibility, with IDR plans being the most common pathway. Plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and REPAYE require borrowers to make consistent, qualifying payments for 20–25 years. However, enrolling in a non-IDR plan, such as the Standard Repayment Plan, does not count toward forgiveness. Borrowers must actively choose an IDR plan and maintain enrollment through annual recertification. Failure to recertify on time can reset the payment counter, delaying forgiveness by years.

Employment requirements are particularly stringent for programs like PSLF, which mandates 10 years of full-time work with a qualifying employer, such as a government or nonprofit organization. Part-time workers must meet specific hourly thresholds, and employment gaps can disrupt eligibility. Borrowers must submit an Employment Certification Form periodically to ensure their job qualifies. For example, a teacher working at a low-income school must provide documentation proving the school’s eligibility under PSLF guidelines. Missteps in employment verification are a common reason for denial, making meticulous record-keeping essential.

Application deadlines vary by program but are universally unforgiving. PSLF, for instance, requires borrowers to submit a forgiveness application after completing 120 qualifying payments, with no retroactive consideration for missed deadlines. Other programs, like Teacher Loan Forgiveness, have specific application windows and documentation requirements. Borrowers must plan ahead, tracking their payments and gathering necessary forms well in advance. Missing a deadline can mean losing out on thousands of dollars in forgiveness, underscoring the need for proactive management of the application process.

Will Biden Deliver on Student Loan Forgiveness? What We Know Now

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Requirements, qualifying employers, certification process, and forgiveness after 120 payments

Public Service Loan Forgiveness (PSLF) is a federal program designed to alleviate the burden of student debt for borrowers committed to public service careers. Unlike general student loan forgiveness programs, PSLF specifically targets those working full-time for qualifying employers, offering tax-free forgiveness after 120 eligible payments. This program is not tied to bank loans but rather to federal Direct Loans, making it a unique opportunity for those in public service roles.

Eligibility Requirements: Who Qualifies?

To qualify for PSLF, borrowers must meet specific criteria. First, the loan must be a federal Direct Loan; other types, such as Perkins or FFEL loans, require consolidation into a Direct Loan. Second, the borrower must work full-time for a qualifying employer, defined as a government organization at any level (federal, state, local, or tribal), a 501(c)(3) nonprofit, or certain other nonprofit organizations providing public services. Part-time workers can qualify if they meet the employer’s definition of full-time or work at least 30 hours per week. Lastly, borrowers must make 120 qualifying payments under an income-driven repayment plan while employed full-time by a qualifying employer. Payments made during periods of economic hardship deferment or forbearance do not count toward the 120 total.

Qualifying Employers: Where to Work

Identifying a qualifying employer is crucial for PSLF eligibility. Government agencies at all levels automatically qualify, but nonprofit organizations require closer scrutiny. A 501(c)(3) nonprofit is typically eligible, but other nonprofits must provide specific public services, such as emergency management, public education, or military service. Private organizations may qualify if they are not-for-profit and provide certain public services, but they must meet specific criteria outlined by the U.S. Department of Education. Borrowers can use the PSLF Help Tool to determine their employer’s eligibility and ensure they are on the right track.

Certification Process: Staying on Track

The PSLF certification process is a proactive step borrowers must take to ensure their payments and employment qualify. Borrowers should submit an Employment Certification Form (ECF) annually or whenever they change employers. This form confirms their employment status and payment eligibility, helping them avoid surprises later. The ECF also allows the loan servicer to track progress toward the 120 required payments. While not mandatory, submitting the ECF regularly is highly recommended to catch any issues early, such as payments not counting due to incorrect repayment plan enrollment.

Forgiveness After 120 Payments: The Payoff

After making 120 qualifying payments, borrowers can apply for PSLF by submitting the PSLF Application for Forgiveness. If approved, the remaining loan balance is forgiven tax-free. This is a significant benefit, as other forgiveness programs may treat the forgiven amount as taxable income. To maximize the benefit, borrowers should ensure all payments are made on time and under an income-driven repayment plan, which can lower monthly payments based on income and family size. For example, a borrower earning $40,000 annually with $100,000 in loans might pay as little as $150 per month under the Revised Pay As You Earn (REPAYE) plan, making PSLF more attainable.

Practical Tips for Success

To navigate PSLF successfully, borrowers should stay organized and informed. Keep detailed records of payments, employment, and submitted forms. Regularly update contact information with the loan servicer to avoid missing important notifications. Consider setting up automatic payments to ensure timely payments each month. Finally, stay informed about program changes by subscribing to updates from the Department of Education or following reputable student loan resources. With careful planning and adherence to the requirements, PSLF can be a life-changing opportunity for those dedicated to public service.

Understanding Student Loan Forgiveness: Age Limits and Eligibility Criteria

You may want to see also

Explore related products

![]()

Income-Driven Repayment Forgiveness: Plan options, payment calculations, forgiveness timelines, and tax implications

Income-Driven Repayment (IDR) plans are a lifeline for borrowers struggling to manage federal student loan debt, offering lower monthly payments tied to income and family size. Four primary plans exist: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each plan caps monthly payments at a percentage of discretionary income, ranging from 10% to 20%, depending on the plan and borrower circumstances. For instance, REPAYE sets payments at 10% of discretionary income for all borrowers, while IBR adjusts this rate based on when the loan was first disbursed. Understanding these differences is critical, as the right plan can significantly reduce financial strain and accelerate progress toward forgiveness.

Payment calculations under IDR plans follow a specific formula: adjusted gross income (AGI) minus 150% of the poverty guideline for your family size and state. For example, a single borrower in California earning $40,000 annually would have discretionary income calculated as $40,000 – $20,040 (150% of the poverty guideline), resulting in $19,960. Under REPAYE, their monthly payment would be $166.33 (10% of $19,960 divided by 12). However, if their income drops or family size increases, payments adjust accordingly, ensuring affordability. Borrowers must recertify income and family size annually to maintain eligibility, a step often overlooked but essential to avoid payment spikes.

Forgiveness timelines under IDR plans vary, typically ranging from 20 to 25 years, depending on the plan and borrower profile. For instance, PAYE and REPAYE offer forgiveness after 20 years for undergraduate loans, while IBR extends this to 25 years for newer borrowers. ICR, the oldest plan, forgives remaining balances after 25 years for all borrowers. Importantly, any forgiven amount may be taxed as income, a potential financial pitfall. For example, a borrower with $50,000 forgiven after 20 years could face a tax bill of $12,500 in the 25% bracket, though current law exempts forgiven amounts through 2025 under the American Rescue Plan.

Tax implications of IDR forgiveness are a double-edged sword. While forgiveness provides relief from debt, it can trigger a substantial tax liability unless legislative exemptions are extended. Borrowers should plan ahead by setting aside funds or exploring options like Public Service Loan Forgiveness (PSLF), which offers tax-free forgiveness after 10 years of qualifying payments. Additionally, switching to a lower-tax-bracket year for forgiveness (e.g., during a career break) can minimize the impact. Consulting a tax professional is advisable to navigate these complexities and optimize financial outcomes.

In summary, Income-Driven Repayment Forgiveness offers a structured path to debt relief but requires careful navigation. Borrowers must select the right plan, stay diligent with annual recertification, and prepare for potential tax consequences. By understanding plan options, payment calculations, forgiveness timelines, and tax implications, borrowers can transform a daunting debt burden into a manageable financial journey.

Can Refinanced Student Loans Be Forgiven After Death? Key Facts

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness: Eligibility, teaching requirements, award amounts, and application process for educators

Teachers burdened by student loan debt may find relief through the Teacher Loan Forgiveness program, a federal initiative designed to incentivize and support educators in low-income schools. This program offers a unique opportunity for eligible teachers to have a portion of their federal student loans forgiven, providing financial breathing room and acknowledging the critical role educators play in society.

Eligibility: Who Qualifies for This Opportunity?

To be eligible for Teacher Loan Forgiveness, educators must meet specific criteria. Firstly, you must have been employed full-time as a teacher for five complete and consecutive academic years in a low-income school or educational service agency. This requirement ensures that the program benefits those serving in areas with the greatest need. Additionally, the loans must have been obtained before the end of your fifth year of teaching. It's important to note that this program is applicable to Direct Subsidized and Unsubsidized Loans, as well as Subsidized and Unsubsidized Federal Stafford Loans.

Teaching Requirements: Defining the Role

The program's teaching requirements are straightforward. Eligible teachers must be highly qualified, as defined by the No Child Left Behind Act, and provide direct classroom teaching, or classroom-type teaching in a non-classroom setting. This includes special education teachers, as long as they meet the highly qualified teacher standards. The program recognizes the diverse roles educators play, ensuring that those in non-traditional teaching environments can also benefit.

Award Amounts: A Substantial Financial Boost

The Teacher Loan Forgiveness program offers substantial financial relief. Eligible teachers can receive up to $17,500 in loan forgiveness. However, the amount varies based on the subject taught. Secondary school teachers in mathematics or science, or special education teachers, can receive the full $17,500. Other eligible teachers can receive up to $5,000. This tiered system aims to address critical teacher shortages in specific subjects while still providing support to all qualifying educators.

Application Process: Navigating the Steps

Applying for Teacher Loan Forgiveness involves several steps. After completing the required five years of teaching, educators must submit an application to their loan servicer. This application includes an employment certification form, which must be completed by the chief administrative officer of the school or agency where you taught. It's crucial to keep detailed records of your employment and teaching assignments during the five-year period to facilitate a smooth application process.

The Teacher Loan Forgiveness program is a powerful tool for educators seeking financial relief. By understanding the eligibility criteria, teaching requirements, and application process, teachers can take advantage of this opportunity to reduce their student loan burden significantly. This program not only provides financial support but also serves as a testament to the value society places on the teaching profession.

Can Defaulted Student Loans Be Forgiven? Exploring Your Options

You may want to see also

Explore related products

![]()

Loan Discharge Options: Disability, school closure, borrower defense, and total permanent disability discharge criteria

Student loan borrowers facing insurmountable challenges may qualify for loan discharge, a process that eliminates debt obligations under specific circumstances. Unlike forgiveness programs, which often require years of service or payments, discharge options provide immediate relief for those who meet stringent criteria. Four primary pathways exist: disability, school closure, borrower defense, and total permanent disability discharge. Each requires meticulous documentation and adherence to federal guidelines, but they offer a lifeline to those in dire situations.

Disability Discharge demands proof of a physical or mental impairment that prevents substantial gainful activity, as certified by a physician. Borrowers must submit evidence to the U.S. Department of Education, which reviews applications against Social Security Administration (SSA) standards. For those receiving SSA benefits, the process is streamlined; others must provide medical documentation. A three-year monitoring period follows approval, during which earning above the poverty line could reinstate the loan. This option is critical for individuals whose health precludes employment, but it requires vigilance to maintain compliance.

School Closure Discharge applies when a borrower’s institution closes before completing their program or within 120 days of withdrawal. Applicants must prove enrollment status and that credits are non-transferable. For-profit school closures, such as those in the ITT Tech and Corinthian Colleges cases, have led to thousands of discharges. The process involves submitting a claim to the loan servicer, supported by enrollment records. This option underscores the importance of choosing accredited institutions and staying informed about school stability.

Borrower Defense to Repayment allows discharge if the school misled borrowers or violated state laws. Common claims include false job placement rates or accreditation status. Applicants must file a complaint with the Department of Education, detailing the school’s misconduct. Approved cases can result in full discharge and refund of payments made. High-profile examples include Corinthian Colleges and American Career Institute, where widespread fraud led to group discharges. This pathway empowers borrowers to hold institutions accountable, but it requires detailed evidence and persistence.

Total and Permanent Disability (TPD) Discharge is the most comprehensive option, available to borrowers with severe, permanent disabilities. Eligibility extends to veterans with service-related disabilities certified by the Department of Veterans Affairs. Unlike standard disability discharge, TPD has no monitoring period, offering permanent relief. Applicants must submit documentation via the TPD website or mail, with automatic consideration for SSA and VA beneficiaries. This option is a critical safety net, ensuring that those with lifelong disabilities are not burdened by unmanageable debt.

In summary, loan discharge options provide targeted relief for borrowers facing extreme hardship. Each pathway requires specific documentation and adherence to federal rules, but they offer a chance to escape debt when repayment is impossible. Understanding these criteria empowers borrowers to navigate their options effectively, turning a financial crisis into an opportunity for a fresh start.

Forgiving Student Loans: Pros, Cons, and Long-Term Impact Explained

You may want to see also

Frequently asked questions

No, there is no student loan forgiveness program exclusively for bank loans. Forgiveness programs typically apply to federal student loans, not private loans from banks.

Generally, private bank student loans do not qualify for federal forgiveness programs. However, some state or employer-based programs may offer assistance for private loans.

Yes, alternatives include refinancing for lower interest rates, income-based repayment plans (if available), or negotiating with the lender for settlement or reduced payments.

No, refinancing federal loans with a private bank typically makes them ineligible for federal forgiveness programs, as they convert to private loans.