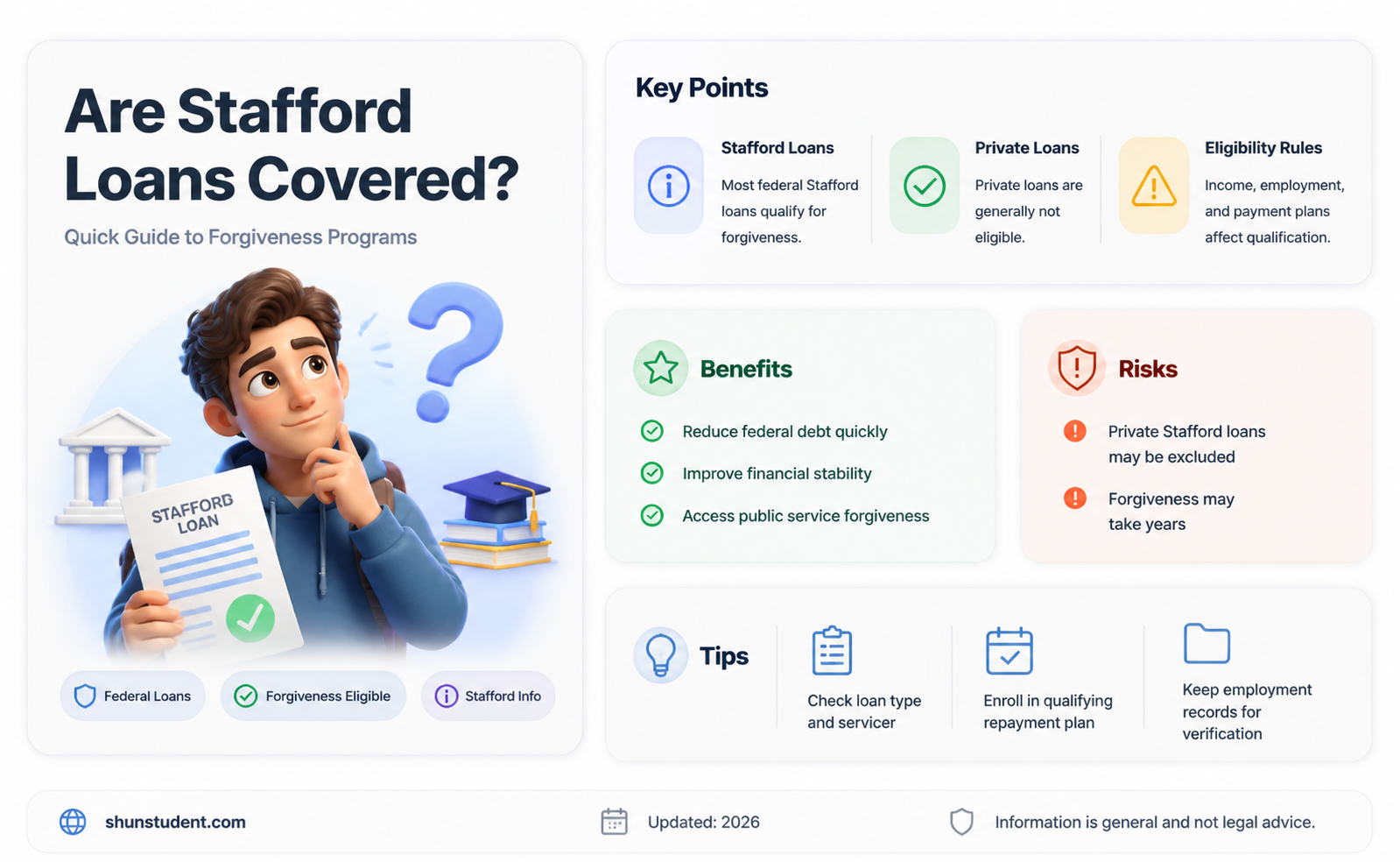

The question of whether Stafford loans are covered under student loan forgiveness programs is a critical concern for many borrowers navigating the complexities of student debt relief. Stafford loans, which include both subsidized and unsubsubsidized Direct Loans, are among the most common federal student loans issued to undergraduate and graduate students. As the federal government continues to roll out various forgiveness initiatives, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, understanding the eligibility of Stafford loans is essential. Generally, Stafford loans are eligible for these programs, provided borrowers meet specific criteria, such as making qualifying payments under an approved repayment plan or working in public service. However, the nuances of each forgiveness program and the requirements for Stafford loan holders can vary, making it crucial for borrowers to carefully review the terms and conditions to ensure they qualify for potential debt relief.

| Characteristics | Values |

|---|---|

| Loan Type Eligibility | Stafford Loans (both Subsidized and Unsubsidized) are eligible for forgiveness under certain programs. |

| Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness. |

| PSLF Eligibility | Stafford Loans qualify if consolidated into a Direct Consolidation Loan and meet PSLF requirements. |

| Teacher Loan Forgiveness | Up to $17,500 in Stafford Loan forgiveness for eligible teachers in low-income schools. |

| IDR Forgiveness | Stafford Loans can be forgiven after 20-25 years of qualifying payments under IDR plans. |

| Consolidation Requirement | Stafford Loans must be consolidated into a Direct Loan to qualify for PSLF. |

| Interest Subsidy | Subsidized Stafford Loans may have interest paid by the government during certain periods. |

| Borrower Defense to Repayment | Stafford Loans may be eligible for discharge if the school misled the borrower. |

| Total and Permanent Disability Discharge | Stafford Loans can be discharged if the borrower has a permanent disability. |

| Death Discharge | Stafford Loans are discharged upon the borrower's death. |

| Current Policy (as of 2023) | Stafford Loans remain eligible for forgiveness under existing federal programs. |

Explore related products

What You'll Learn

- Eligibility Criteria: Stafford loan types (Direct, FFEL) and forgiveness program requirements

- Public Service Loan Forgiveness (PSLF): Stafford loans under PSLF rules and conditions

- Income-Driven Repayment Plans: Forgiveness options for Stafford loans after 20-25 years of payments

- Teacher Loan Forgiveness: Stafford loan forgiveness for eligible teachers in low-income schools

- Biden’s Forgiveness Plan: Stafford loans covered under the 2022 federal student loan forgiveness initiative

![]()

Eligibility Criteria: Stafford loan types (Direct, FFEL) and forgiveness program requirements

Stafford Loans, a cornerstone of federal student aid, come in two primary flavors: Direct Stafford Loans and Federal Family Education Loan (FFEL) Program loans. Understanding which type you hold is the first step in determining your eligibility for student loan forgiveness programs. Direct Stafford Loans are issued directly by the U.S. Department of Education, while FFEL loans are funded by private lenders but guaranteed by the federal government. This distinction is critical because not all forgiveness programs treat these loan types equally.

For Direct Stafford Loans, borrowers are in a more favorable position when it comes to forgiveness. Programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans such as Income-Based Repayment (IBR) and Pay As You Earn (PAYE) are accessible to Direct Loan holders. To qualify for PSLF, for instance, borrowers must make 120 qualifying payments while working full-time for a qualifying employer, typically a government or nonprofit organization. IDR plans, on the other hand, offer forgiveness after 20 or 25 years of payments, depending on the plan and when the loans were taken out.

FFEL Loans present a more complex scenario. These loans are not eligible for PSLF unless they are consolidated into a Direct Consolidation Loan. Consolidation is a strategic move for FFEL borrowers seeking forgiveness, as it opens the door to PSLF and IDR plans. However, consolidating resets the payment count for PSLF, meaning borrowers must start anew with their 120 qualifying payments. Additionally, FFEL borrowers must ensure their loans are in a repayment status that qualifies for forgiveness, as certain statuses, like deferment or forbearance, may not count toward the required payment total.

A critical takeaway is that eligibility for forgiveness programs hinges on both the type of Stafford Loan and the borrower’s repayment strategy. Direct Loan holders have more straightforward access to forgiveness programs, while FFEL borrowers must take proactive steps, such as consolidation, to qualify. Borrowers should carefully review their loan types and repayment plans, consulting resources like the Federal Student Aid website or a loan servicer for personalized guidance. By understanding these nuances, Stafford Loan holders can navigate the path to forgiveness with greater clarity and confidence.

Grad Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Stafford loans under PSLF rules and conditions

Stafford Loans, both Subsidized and Unsubsidized, are eligible for Public Service Loan Forgiveness (PSLF), a federal program designed to alleviate student debt for borrowers committed to public service careers. This program offers a pathway to debt relief after 120 qualifying payments, but navigating its rules and conditions requires precision. Understanding the specifics of how Stafford Loans fit into PSLF is crucial for maximizing this opportunity.

To qualify for PSLF with Stafford Loans, borrowers must first consolidate their loans into a Direct Consolidation Loan, as only Direct Loans are eligible for the program. This step is non-negotiable, even if you already have Stafford Loans, which are technically part of the Federal Family Education Loan (FFEL) program. Consolidation ensures your loans are under the Direct Loan umbrella, making them PSLF-eligible. After consolidation, borrowers must make 120 qualifying payments while working full-time for a qualifying employer, such as a government organization or a 501(c)(3) nonprofit. These payments must be made under an income-driven repayment plan to ensure they are counted toward PSLF.

One critical aspect of PSLF is the definition of a "qualifying payment." Payments must be made on time, in full, and under a qualifying repayment plan. Partial payments or those made during periods of deferment or forbearance do not count. Borrowers should also submit the Employment Certification Form (ECF) annually or when changing employers to ensure their employment qualifies and to track their progress toward forgiveness. This proactive approach minimizes the risk of disqualification due to administrative errors.

A common pitfall for Stafford Loan borrowers is assuming their payments automatically qualify for PSLF. Many borrowers discover too late that their payments were not made under an income-driven plan or that their employer did not meet PSLF criteria. To avoid this, borrowers should regularly consult the Federal Student Aid website and work closely with their loan servicer to ensure compliance. Additionally, staying informed about updates to PSLF rules, such as the Limited PSLF Waiver (which expired in October 2022), can provide opportunities to retroactively qualify payments that were previously ineligible.

In conclusion, Stafford Loans can be a ticket to debt relief through PSLF, but success hinges on meticulous adherence to the program’s rules. Consolidation, qualifying employment, income-driven repayment, and diligent documentation are the cornerstones of this strategy. By taking these steps, borrowers can transform their public service commitment into a powerful tool for financial freedom.

Devry Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: Forgiveness options for Stafford loans after 20-25 years of payments

Stafford loans, both subsidized and unsubsidized, are eligible for forgiveness under Income-Driven Repayment (IDR) plans after 20 to 25 years of qualifying payments. This pathway is particularly beneficial for borrowers with federal student loans who may struggle to repay their debt under standard repayment plans. The key to unlocking this forgiveness lies in choosing the right IDR plan and understanding the nuances of each option.

Step 1: Choose an Income-Driven Repayment Plan

There are four main IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each plan calculates monthly payments differently, typically capping them at 10-20% of your discretionary income. For Stafford loan borrowers, REPAYE and IBR are often the most advantageous due to their lower payment caps and shorter forgiveness timelines (20-25 years). For example, if you’re a single borrower earning $40,000 annually, your monthly payment under REPAYE might be as low as $100, compared to $400 under a standard 10-year plan.

Caution: Tax Implications of Loan Forgiveness

While IDR plans offer a lifeline for Stafford loan borrowers, the forgiven amount after 20-25 years is typically treated as taxable income. This means you could face a significant tax bill in the year of forgiveness. For instance, if $30,000 of your Stafford loan is forgiven, you may owe taxes on that amount at your current tax rate. To mitigate this, consider setting aside a portion of your savings annually in a "forgiveness tax fund" or explore options like Public Service Loan Forgiveness (PSLF), which offers tax-free forgiveness after 10 years of qualifying payments.

Practical Tips for Maximizing Forgiveness

To ensure you qualify for IDR forgiveness, stay vigilant about recertifying your income and family size annually—failure to do so can result in being switched to a standard repayment plan. Additionally, keep detailed records of all payments, as administrative errors are common. If you’re pursuing PSLF alongside an IDR plan, submit an Employment Certification Form annually to track your progress. Finally, consider refinancing private loans separately, as only federal Stafford loans qualify for IDR forgiveness.

Comparative Analysis: IDR vs. Standard Repayment

While standard repayment plans offer a clear end date (typically 10 years), IDR plans provide flexibility and long-term relief for Stafford loan borrowers. For example, a borrower with $50,000 in Stafford loans at 5% interest would pay $530 monthly under a standard plan, totaling $63,600 over 10 years. In contrast, an IDR plan might reduce payments to $200 monthly, with the remaining balance forgiven after 240-300 payments. While the total paid over 25 years ($60,000) is comparable, the lower monthly burden and forgiveness option make IDR plans a strategic choice for those with limited income.

Income-Driven Repayment plans offer Stafford loan borrowers a viable path to forgiveness, but success requires careful planning and adherence to program rules. By selecting the right plan, preparing for tax implications, and staying organized, borrowers can navigate the complexities of IDR and achieve financial relief after 20-25 years of payments. This approach not only reduces immediate financial strain but also provides a long-term solution to student debt.

Unraveling the Truth About Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness: Stafford loan forgiveness for eligible teachers in low-income schools

Teachers in low-income schools face unique challenges, but the Teacher Loan Forgiveness program offers a financial lifeline by forgiving up to $17,500 of Stafford loan debt. This program is specifically designed to incentivize educators to commit to high-need areas, where their impact can be most significant. To qualify, teachers must work full-time for five consecutive years in a designated low-income school, as determined by the federal government’s annual directory. The amount forgiven depends on the subject taught: educators in math, science, or special education may receive the full $17,500, while others can receive up to $5,000. This tiered structure highlights the program’s focus on addressing critical teacher shortages in specific fields.

Eligibility for Teacher Loan Forgiveness requires more than just teaching in a low-income school. Applicants must have Stafford loans (Direct Subsidized or Unsubsidized) and cannot have had an outstanding balance on these loans as of Oct. 1, 1998. Additionally, the five years of service must be continuous, though not necessarily at the same school. Teachers should also ensure their employment qualifies by checking the federal directory of low-income schools annually, as a school’s status can change. Documentation, such as employment verification and loan details, is critical when applying, so maintaining organized records is essential.

While Teacher Loan Forgiveness is a valuable opportunity, it’s not without limitations. For instance, private Stafford loans or FFEL loans not consolidated into the Direct Loan program are ineligible. Teachers pursuing this option should consolidate their loans if necessary, but beware: consolidating resets the five-year service clock. Additionally, forgiveness is considered taxable income, so recipients may owe federal taxes on the forgiven amount. Teachers should consult a tax professional to plan for this potential liability and explore other forgiveness programs, like Public Service Loan Forgiveness (PSLF), which may offer tax-free benefits after 10 years of service.

For teachers committed to low-income schools, combining Teacher Loan Forgiveness with other strategies can maximize debt relief. For example, educators can simultaneously work toward PSLF by making qualifying payments while teaching in a public or nonprofit school. This dual approach allows teachers to receive $5,000 or $17,500 in forgiveness after five years and continue toward full PSLF forgiveness after 10 years. To optimize this strategy, teachers should enroll in an income-driven repayment plan, which lowers monthly payments and ensures eligibility for both programs. Careful planning and coordination can turn these programs into powerful tools for financial freedom.

Finally, teachers should act proactively to take advantage of Teacher Loan Forgiveness. Start by confirming your school’s eligibility annually and tracking your years of service meticulously. Submit your application for forgiveness after completing the five-year requirement, using the official Teacher Loan Forgiveness Application form. Stay informed about changes to the program and explore additional resources, such as state-based loan repayment assistance programs, to supplement federal forgiveness. By leveraging these opportunities, educators can focus on their students without being burdened by overwhelming student debt.

North Carolina's Tax Rules on Student Loan Forgiveness Explained

You may want to see also

Explore related products

![]()

Biden’s Forgiveness Plan: Stafford loans covered under the 2022 federal student loan forgiveness initiative

Stafford loans, a cornerstone of federal student aid, were a central focus of President Biden’s 2022 student loan forgiveness initiative. This plan aimed to alleviate the financial burden on millions of borrowers, but its specifics required careful examination to understand who qualified and how much relief was available. For Stafford loan holders, the news was significant: both Direct Subsidized and Direct Unsubsidized Stafford loans were eligible for forgiveness under the program, provided borrowers met certain income criteria. This inclusion marked a critical step in addressing the growing student debt crisis, offering a lifeline to those struggling to repay their loans.

To qualify for forgiveness, borrowers with Stafford loans had to meet specific income thresholds: individuals earning less than $125,000 annually or married couples filing jointly with incomes under $250,000 were eligible. The relief was substantial, with up to $10,000 in forgiveness for eligible borrowers and an additional $10,000 for those who had received Pell Grants. This tiered approach ensured that the most financially vulnerable borrowers received greater assistance, addressing disparities in the student loan landscape. For Stafford loan holders, this meant a potential reduction or elimination of their debt, depending on their balance and income level.

The process for Stafford loan holders to access this relief was relatively straightforward. Borrowers were encouraged to apply through the Federal Student Aid website, though the Department of Education also planned to automatically discharge loans for those whose income data was already on file. This streamlined approach aimed to minimize administrative hurdles, ensuring that eligible borrowers could access forgiveness without unnecessary delays. However, it was crucial for Stafford loan holders to verify their eligibility and monitor updates, as legal challenges and policy changes could impact the program’s implementation.

Critics of the plan raised concerns about its long-term economic implications, arguing that widespread forgiveness could exacerbate inflation or create moral hazard. Proponents, however, emphasized its potential to stimulate economic growth by freeing borrowers from debt burdens, enabling them to invest in homes, start businesses, or save for the future. For Stafford loan holders, the initiative represented more than just financial relief—it was a chance to reset their economic trajectory. By understanding the specifics of the plan, borrowers could maximize their benefits and take proactive steps toward financial stability.

In practical terms, Stafford loan holders should take several steps to ensure they benefit from the forgiveness initiative. First, verify your loan type and eligibility by logging into your Federal Student Aid account. Second, update your contact information to receive important notifications from the Department of Education. Third, consider consolidating any Federal Family Education Loan (FFEL) Stafford loans into the Direct Loan program, as only Direct Stafford loans were automatically eligible for forgiveness. Finally, stay informed about deadlines and potential changes to the program, as legal challenges and policy updates could affect your eligibility. By taking these steps, Stafford loan holders can navigate the forgiveness process with confidence and clarity.

Biden's Potential Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Frequently asked questions

Yes, Stafford Loans, both Subsidized and Unsubsidized, are eligible for certain student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness.

Yes, Stafford Loans qualify for PSLF if the borrower works full-time for a qualifying public service employer and makes 120 eligible payments under an approved repayment plan.

Yes, Stafford Loans can be forgiven through income-driven repayment (IDR) plans after 20–25 years of qualifying payments, depending on the specific plan.

Yes, Stafford Loans are included in the one-time student loan forgiveness programs, such as the targeted relief initiatives, provided the borrower meets the eligibility criteria.

No, private Stafford Loans (if they exist) do not qualify for federal student loan forgiveness programs, as these programs only apply to federal student loans, including federal Stafford Loans.