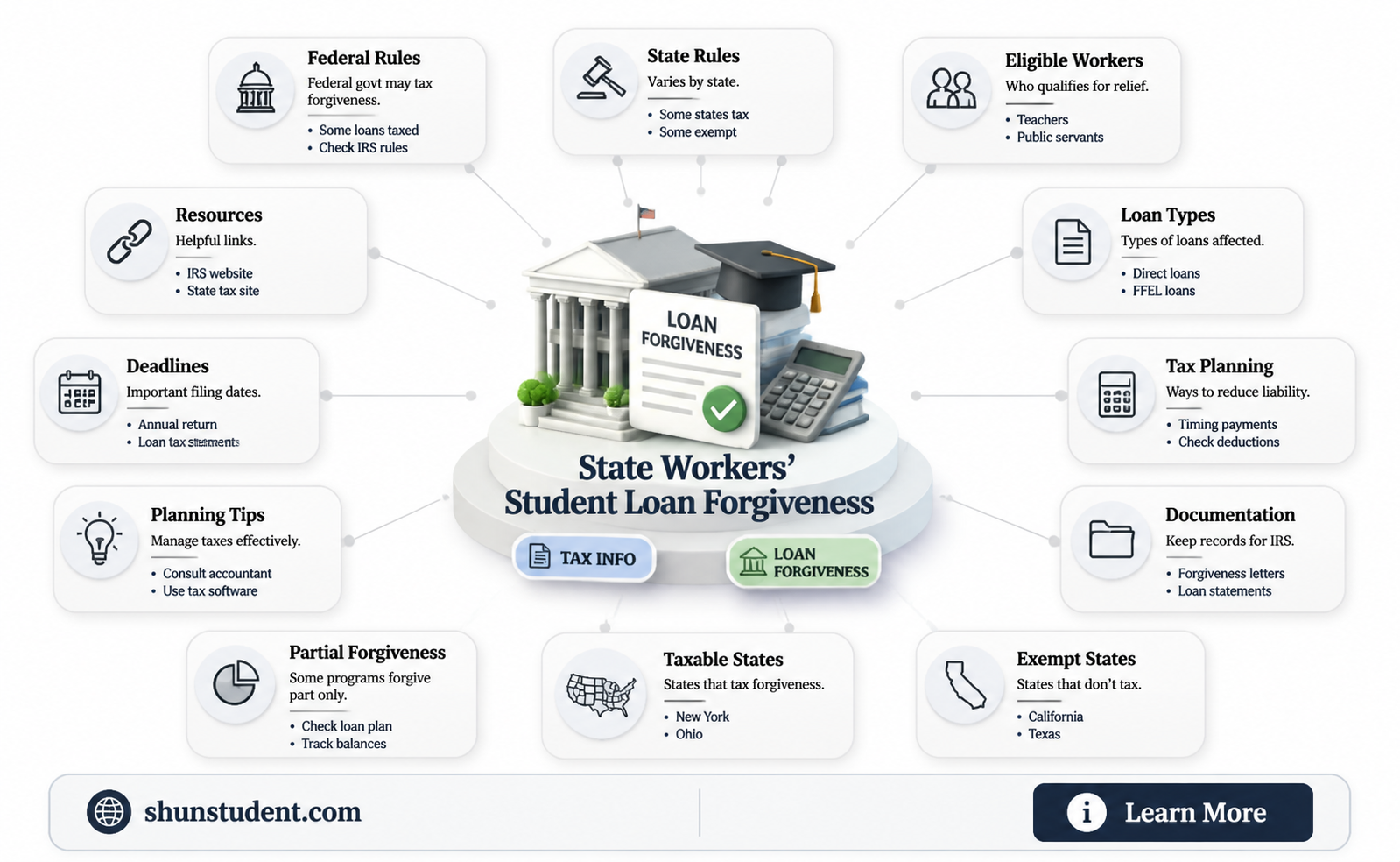

The topic of whether state workers are taxed for student loan forgiveness has gained significant attention as federal and state governments implement various debt relief programs. While the federal government’s Public Service Loan Forgiveness (PSLF) program generally excludes forgiven amounts from taxable income, state-level taxation varies widely. Some states align with federal tax treatment, exempting forgiven student loans from state income tax, while others may consider it taxable income, creating an unexpected financial burden for public servants. This disparity highlights the need for state workers to understand their specific state’s tax laws and underscores the broader debate over the fairness of taxing debt relief for those in public service roles.

| Characteristics | Values |

|---|---|

| Federal Tax Treatment | Student loan forgiveness is generally considered taxable income by the IRS, unless specifically excluded by law (e.g., Public Service Loan Forgiveness under the American Rescue Plan Act of 2021). |

| State Tax Treatment | Varies by state; some states follow federal tax rules, while others may exempt student loan forgiveness from state income tax. |

| Public Service Loan Forgiveness (PSLF) | Tax-free at the federal level for loans forgiven through PSLF, as of the American Rescue Plan Act (2021). State treatment depends on local laws. |

| State-Specific Exemptions | Some states (e.g., California, New York) have explicitly exempted student loan forgiveness from state income tax, while others have not. |

| Temporary vs. Permanent Relief | Temporary federal tax exclusions (e.g., CARES Act) may not apply to state taxes, depending on state conformity to federal law. |

| State Worker Eligibility | State workers may qualify for PSLF or other forgiveness programs, but state tax implications depend on local legislation. |

| Recent Legislation | Check state-specific laws, as some states have recently updated their tax codes to address student loan forgiveness (e.g., Illinois in 2023). |

| Consultation Advice | State workers should consult state tax authorities or a tax professional to determine their specific tax liability for student loan forgiveness. |

Explore related products

$10.1 $16.99

What You'll Learn

![]()

Federal vs. State Tax Rules

The tax treatment of student loan forgiveness for state workers hinges on a critical distinction: federal versus state tax rules. While the federal government generally excludes forgiven student loans from taxable income under the American Rescue Plan Act of 2021 (through 2025), states operate under their own tax codes, creating a patchwork of outcomes. This disparity means a state worker in Mississippi, which conforms to federal tax rules, might owe nothing, while a counterpart in Massachusetts could face a state tax bill on the forgiven amount.

Consider the mechanics of state conformity. Some states, like Arizona and Minnesota, have partially conformed to federal exclusion rules but with specific conditions or limitations. Others, such as California and New York, maintain their own tax treatment, often taxing forgiven loans as income unless explicitly exempted by state legislation. For instance, California excludes forgiven student loans under certain federal programs but requires taxpayers to file additional forms to claim the exclusion. This complexity underscores the need for state workers to consult state-specific guidance or a tax professional.

A persuasive argument emerges when examining the equity implications of this federal-state divide. State workers in non-conforming states effectively face a "forgiveness penalty," paying state taxes on debt relief intended to alleviate financial burden. Advocacy groups argue that states should align with federal exclusions to ensure consistent relief, particularly for public servants in income-driven repayment plans or those pursuing Public Service Loan Forgiveness (PSLF). For example, in 2023, Illinois passed legislation to exclude forgiven student loans from state taxable income, reflecting a growing trend toward alignment.

Practically, state workers must take proactive steps to navigate this landscape. First, verify your state’s tax treatment of student loan forgiveness by checking the state revenue department’s website or consulting IRS Publication 970. Second, retain documentation of the forgiven amount and any federal exclusions claimed. Third, if your state taxes forgiven loans, explore state-specific deductions or credits that might offset the liability. For instance, some states offer credits for public service employment, which could partially mitigate the tax impact.

In conclusion, the federal-state tax rule disparity for student loan forgiveness demands attention to detail and strategic planning. While federal exclusions provide broad relief, state-level variations can significantly alter the financial outcome for state workers. By understanding these nuances and taking targeted actions, individuals can minimize unexpected tax liabilities and maximize the benefits of loan forgiveness programs.

Unlocking Student Loan Forgiveness: Weekly Work Hours Explained

You may want to see also

Explore related products

![]()

Taxable Income Thresholds

Student loan forgiveness can significantly reduce financial burdens, but it often comes with tax implications that vary by state and individual circumstances. One critical factor in determining whether forgiven loans are taxable is the concept of taxable income thresholds. These thresholds dictate when and how much of the forgiven amount is considered taxable income, influencing the overall financial impact of loan forgiveness programs.

Consider the federal tax treatment of student loan forgiveness, which typically treats forgiven amounts as taxable income unless they fall under specific exceptions, such as the Public Service Loan Forgiveness (PSLF) program. However, state tax laws differ widely. For instance, some states, like Pennsylvania and Indiana, align with federal guidelines, taxing forgiven loans as income. Others, like California and New York, offer exemptions or partial exclusions for certain forgiveness programs, particularly for state workers in public service roles. Understanding these state-specific thresholds is crucial for state workers to anticipate their tax liabilities accurately.

To navigate taxable income thresholds effectively, state workers should first identify their state’s tax treatment of loan forgiveness. For example, in states with no income tax, like Texas or Florida, forgiven loans may not be taxed at the state level, regardless of federal rules. In contrast, states with progressive income tax systems may apply higher tax rates to forgiven amounts that push individuals into higher income brackets. A practical tip is to consult a tax professional or use tax software to model the impact of forgiven loans on both federal and state tax returns.

Another key consideration is the timing of loan forgiveness. Some states may allow taxpayers to spread the forgiven amount over multiple years to avoid exceeding taxable income thresholds in a single year. For instance, if a state worker has $50,000 forgiven, spreading this amount over two years could keep their taxable income below a critical threshold, reducing their overall tax burden. This strategy requires careful planning and an understanding of both federal and state tax laws.

In conclusion, taxable income thresholds play a pivotal role in determining the tax implications of student loan forgiveness for state workers. By researching state-specific rules, modeling tax scenarios, and strategically timing forgiveness, individuals can minimize their tax liabilities and maximize the benefits of loan forgiveness programs. Proactive planning and informed decision-making are essential to navigating this complex landscape successfully.

Medical Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

State-Specific Forgiveness Policies

State-specific student loan forgiveness programs often come with unique tax implications, creating a patchwork of rules that borrowers must navigate carefully. For instance, California’s *Golden State Teacher Grant Program* offers up to $20,000 in loan forgiveness for educators serving in low-income schools, but unlike federal programs, this state benefit is not explicitly exempt from state income tax. Borrowers must consult California’s Franchise Tax Board to determine their liability, as state tax laws can differ significantly from federal guidelines.

In contrast, New York’s *Get on Your Feet Loan Forgiveness Program* provides tax-free relief for recent college graduates earning under $50,000 annually. This program underscores the importance of understanding state-specific legislation, as some states intentionally design their forgiveness programs to avoid additional financial burden on borrowers. However, eligibility criteria can be stringent—New York requires applicants to have graduated after December 2014 and to have lived in the state for at least one year post-graduation.

Borrowers in states like Texas and Florida may face fewer concerns due to their lack of state income tax, but this doesn’t eliminate all complexities. For example, Texas’s *Teach for Texas Loan Repayment Assistance Program* offers up to $2,000 annually for teachers in high-need districts, but recipients must still consider federal tax implications, as some state programs are taxable at the federal level. This highlights the need to cross-reference state and federal tax codes to avoid unexpected liabilities.

To maximize benefits, borrowers should take proactive steps: first, research their state’s forgiveness programs and associated tax rules; second, consult a tax professional to clarify potential obligations; and third, maintain detailed records of all loan forgiveness payments and related documentation. For example, Maryland’s *Janet L. Hoffman Loan Assistance Repayment Program* requires recipients to submit annual reports, which can double as evidence for tax purposes. By staying informed and organized, borrowers can leverage state-specific policies without falling into tax traps.

Student Loan Forgiveness: What Really Happened and Who Benefited?

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![]()

Public Service Loan Forgiveness (PSLF)

One critical aspect of PSLF that state workers must understand is the tax treatment of forgiven debt. Unlike some forms of loan forgiveness, PSLF is tax-free at the federal level, meaning borrowers are not required to report the forgiven amount as taxable income. This is a significant advantage, as it prevents borrowers from facing a large tax bill after receiving forgiveness. For example, if a state worker has $50,000 in student loans forgiven through PSLF, they save not only that principal amount but also the potential tax liability, which could be several thousand dollars depending on their tax bracket. This makes PSLF an even more attractive option for those in public service roles.

To qualify for PSLF, state workers must navigate a series of specific steps. First, ensure your loans are federal Direct Loans, as only this type qualifies for the program. If you have Federal Family Education Loans (FFEL) or Perkins Loans, consolidate them into a Direct Consolidation Loan to become eligible. Second, work full-time for a qualifying employer—this includes federal, state, local, or tribal government agencies, as well as certain nonprofits. Third, make 120 qualifying payments under an income-driven repayment plan, which caps monthly payments based on income and family size. Keep detailed records of your employment and payments, as these will be required when submitting your forgiveness application.

Despite its benefits, PSLF is not without challenges. Common pitfalls include missing payments, working for a non-qualifying employer, or failing to certify employment annually. For instance, a state worker who switches jobs mid-career must ensure their new employer qualifies for PSLF and promptly submit an Employment Certification Form to avoid losing progress. Additionally, the program’s strict requirements mean that even minor errors can disqualify borrowers. To mitigate these risks, state workers should consult the Federal Student Aid website regularly, use the PSLF Help Tool to assess eligibility, and seek guidance from loan servicers or financial advisors.

In conclusion, PSLF offers state workers a powerful tool to eliminate student debt tax-free, but success requires careful planning and adherence to program rules. By understanding the eligibility criteria, maintaining accurate records, and staying proactive, state workers can maximize their chances of achieving loan forgiveness. For those committed to a career in public service, PSLF is not just a financial benefit—it’s a reward for their dedication to the greater good.

Can Retired Federal Employees Get Student Loan Forgiveness?

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Tax Implications by State Laws

State workers rejoicing over student loan forgiveness may face an unexpected tax bill, depending on where they live. While federal law generally excludes forgiven student loans from taxable income, state tax treatment varies widely. This patchwork of state laws creates a confusing landscape for borrowers, with some states mirroring federal exclusions and others treating forgiven debt as taxable income.

Understanding these state-level nuances is crucial for state employees to accurately plan for their financial future.

Consider the stark contrast between two states. In California, forgiven student loans are generally exempt from state income tax, aligning with federal policy. This means a California state worker receiving $50,000 in loan forgiveness wouldn't owe state taxes on that amount. Conversely, in Mississippi, forgiven student loans are considered taxable income. The same $50,000 forgiveness for a Mississippi state employee could result in a significant state tax liability, potentially reaching thousands of dollars depending on their tax bracket.

This example highlights the importance of checking your specific state's tax code to avoid unwelcome surprises during tax season.

Several factors influence how states approach taxing forgiven student loans. Some states automatically conform to federal tax laws, ensuring consistency. Others maintain their own tax codes, allowing for independent treatment of forgiven debt. Additionally, some states may offer partial exclusions or exemptions based on the type of loan forgiveness program or the borrower's income level. For instance, a state might exempt forgiven loans under a public service loan forgiveness program but tax forgiven loans from income-driven repayment plans.

Navigating this complex landscape requires proactive research. State workers should consult their state's department of revenue website or a tax professional to determine the specific tax implications of their student loan forgiveness. Understanding these state-specific rules empowers borrowers to make informed financial decisions and avoid unexpected tax burdens. Remember, while federal student loan forgiveness programs offer relief, state tax laws can significantly impact the net benefit received.

Does Student Loan Forgiveness Include Private Loans? Key Facts Explained

You may want to see also

Frequently asked questions

Yes, state workers may be eligible for student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), if they meet specific criteria, including working full-time for a qualifying employer and making 120 eligible payments.

Generally, student loan forgiveness through programs like PSLF is tax-free at the federal level. However, some states may tax forgiven amounts, so state workers should check their state’s tax laws.

While federal student loan forgiveness programs like PSLF are tax-free federally, state tax treatment varies. Some states align with federal rules, while others may consider forgiven loans as taxable income.

State workers should consult a tax professional or review their state’s tax laws to understand if forgiven student loans are taxable. They may also need to set aside funds to cover potential state tax liabilities.

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)