The COVID-19 pandemic has brought unprecedented challenges to the global economy, particularly affecting students and graduates burdened by student loans. In response, governments and financial institutions have implemented various relief measures, including the possibility of student loan forgiveness. The question of whether student loans are being forgiven due to the coronavirus has sparked widespread debate and interest, as many borrowers face financial hardships exacerbated by the pandemic. While some countries and programs have offered temporary payment pauses, interest waivers, or limited forgiveness, comprehensive and permanent solutions remain uncertain. This topic highlights the intersection of education policy, economic recovery, and social equity, as stakeholders advocate for sustainable relief to alleviate the growing student debt crisis.

| Characteristics | Values |

|---|---|

| Current Status | No widespread student loan forgiveness due to COVID-19 as of October 2023. |

| CARES Act Provisions (Expired) | Payment pause, 0% interest, and stopped collections (ended Dec 31, 2022). |

| Targeted Relief | Limited forgiveness for specific groups (e.g., public service workers, defrauded students). |

| Biden Administration Efforts | $132 billion in targeted cancellations (e.g., Public Service Loan Forgiveness, income-driven repayment adjustments). |

| Legal Challenges | Supreme Court struck down Biden’s broad $400 billion forgiveness plan in June 2023. |

| Ongoing Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) adjustments. |

| Fresh Start Initiative | Helps defaulted borrowers re-enter repayment with benefits (e.g., credit repair). |

| SAVE Plan | New income-driven repayment plan with lower payments and faster forgiveness for smaller balances. |

| State-Level Initiatives | Some states offer limited relief or repayment assistance programs. |

| Future Outlook | No new broad forgiveness plans announced; focus on targeted relief and repayment reforms. |

Explore related products

What You'll Learn

![]()

CARES Act Loan Forbearance

The CARES Act, signed into law in March 2020, provided immediate relief for federal student loan borrowers by automatically placing their loans into forbearance. This meant that from March 13, 2020, through September 30, 2022, borrowers were not required to make payments, and interest rates were set to 0%. This measure was a direct response to the economic hardship caused by the coronavirus pandemic, offering a financial lifeline to millions. For those struggling with unemployment or reduced income, this forbearance period allowed them to allocate funds to more pressing needs like rent, groceries, or medical bills without the added stress of student loan payments.

Analyzing the impact, the CARES Act forbearance not only paused payments but also froze collections on defaulted loans, preventing wage garnishments and tax refund interceptions. This dual benefit was particularly significant for borrowers in default, as it provided a rare opportunity to regroup financially. Additionally, the forbearance period counted toward loan forgiveness programs like Public Service Loan Forgiveness (PSLF), meaning eligible borrowers continued to accrue credit toward forgiveness without making payments. This aspect was a strategic win for long-term debt management, especially for those in public service careers.

For borrowers, navigating the forbearance required minimal action, as it was applied automatically to eligible federal loans. However, private student loans were not covered, leaving those borrowers to seek relief through separate agreements with their lenders. To maximize the benefits, borrowers were advised to use the paused payments to pay down high-interest debt or build an emergency fund. Those pursuing PSLF were encouraged to ensure their employment and loan types qualified, as the forbearance period could accelerate their path to forgiveness.

A critical takeaway is that while the CARES Act forbearance provided temporary relief, it was not a permanent solution to student debt. Borrowers needed to prepare for the resumption of payments, which eventually occurred in October 2023 after multiple extensions. Strategies such as enrolling in income-driven repayment plans or exploring refinancing options became essential as the forbearance ended. The lesson from this policy is that while emergency measures can offer breathing room, long-term financial planning remains crucial for managing student loan debt effectively.

Unlock Public Service Loan Forgiveness: Your Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) Updates

The Public Service Loan Forgiveness (PSLF) program has seen significant updates in response to the coronavirus pandemic, offering new opportunities for borrowers to achieve loan forgiveness. One critical change is the Limited PSLF Waiver, which temporarily expanded eligibility by allowing previously ineligible payments to count toward the required 120 qualifying payments. This waiver, which expired on October 31, 2022, provided a lifeline for borrowers with Federal Family Education Loans (FFEL) or Perkins Loans by permitting them to consolidate into Direct Loans and retroactively apply past payments. For example, a teacher with 10 years of service under an FFEL loan could consolidate, have those years count, and immediately qualify for forgiveness.

Analyzing the impact, the waiver addressed long-standing criticisms of PSLF’s complexity and stringent requirements. Borrowers who had made payments while in the wrong loan type or repayment plan suddenly found themselves on track for forgiveness. However, the process wasn’t without challenges. Many borrowers reported difficulties navigating the consolidation process and ensuring their payments were correctly counted. The U.S. Department of Education responded by streamlining applications and providing clearer guidance, but the urgency of the October 2022 deadline left some scrambling to act in time.

For those who missed the waiver, all is not lost. The PSLF reforms introduced in 2021 continue to offer pathways to forgiveness. These include a more flexible definition of qualifying payments and a review process for denied applications. Borrowers in public service roles, such as nurses, firefighters, and nonprofit employees, can now have their employment certified proactively through the PSLF Help Tool. Additionally, the IDR Account Adjustment, launched in 2023, retroactively credits time spent in forbearance or certain repayment plans toward forgiveness, further easing the burden for long-term borrowers.

A comparative look at pre- and post-pandemic PSLF reveals a program transformed. Before COVID-19, PSLF had a notoriously low approval rate, with only 2.2% of applicants receiving forgiveness by 2021. Post-pandemic updates have increased approvals significantly, with over $14 billion in loans forgiven as of 2023. This shift underscores the importance of staying informed about policy changes. For instance, borrowers should regularly submit the PSLF form to ensure their payments are tracked accurately and take advantage of tools like the Payment Tracking System.

In conclusion, the PSLF updates tied to the coronavirus pandemic have opened doors for countless public servants. While the Limited PSLF Waiver has ended, ongoing reforms continue to simplify the path to forgiveness. Borrowers should act proactively by consolidating ineligible loans, certifying employment annually, and monitoring policy changes. With persistence and the right strategy, achieving PSLF is more attainable than ever.

Unlocking Pell Grant Forgiveness: A Guide for Struggling Students

You may want to see also

Explore related products

![]()

Biden Administration Forgiveness Plans

The Biden administration has taken significant steps to address the student loan crisis exacerbated by the coronavirus pandemic, offering targeted relief to millions of borrowers. One of the most notable initiatives is the Public Service Loan Forgiveness (PSLF) waiver, which temporarily expanded eligibility for loan forgiveness. This waiver, active until October 31, 2022, allowed borrowers to receive credit for past payments that were previously deemed ineligible, provided they worked in qualifying public service jobs. For example, a teacher with 10 years of service could have payments made under a graduated repayment plan counted toward forgiveness, even if they were initially excluded.

Another cornerstone of the Biden administration’s efforts is the targeted loan cancellation for specific groups. In April 2022, the Department of Education announced $6.8 billion in loan forgiveness for over 200,000 borrowers who were defrauded by for-profit colleges, such as Corinthian Colleges and ITT Tech. Additionally, borrowers with total and permanent disabilities received automatic loan discharges totaling $7.7 billion, benefiting over 400,000 individuals. These actions demonstrate a focus on rectifying systemic issues and providing relief to the most vulnerable borrowers.

While broad-based student loan forgiveness remains a topic of debate, the Biden administration has implemented income-driven repayment (IDR) reforms to reduce long-term financial burdens. These reforms include shortening the repayment period for undergraduate loans to 20 years (from 25) and capping monthly payments at 5% of discretionary income. For instance, a borrower earning $40,000 annually with $30,000 in debt could see their monthly payment drop from $300 to $150 under the revised plan. These changes aim to make repayment more manageable and prevent borrowers from defaulting.

Critics argue that these measures, while helpful, fall short of addressing the $1.7 trillion student debt crisis comprehensively. However, the administration’s pause on federal student loan payments, extended multiple times since March 2020, has provided immediate relief to 43 million borrowers. This pause, which includes a 0% interest rate, has saved the average borrower over $2,000 in payments. Practical tips for borrowers include using the payment pause to pay down higher-interest debt or build an emergency fund, as interest will not accrue during this period.

In conclusion, the Biden administration’s forgiveness plans are a patchwork of targeted initiatives rather than a one-size-fits-all solution. By focusing on public service workers, defrauded borrowers, and those with disabilities, the administration has prioritized equity and accountability. While broader forgiveness remains uncertain, borrowers can take advantage of IDR reforms and the payment pause to stabilize their financial situations. Staying informed about policy updates and exploring eligibility for existing programs is crucial for maximizing relief.

Massachusetts Tax Rules: Student Loan Forgiveness Explained

You may want to see also

Explore related products

![]()

Income-Driven Repayment (IDR) Changes

The CARES Act's pause on student loan payments and interest accrual has ended, but the Biden administration's recent changes to Income-Driven Repayment (IDR) plans offer a new lifeline for borrowers. These revisions aim to address longstanding issues with IDR plans, which were designed to make loan payments more manageable but often fell short due to complex rules and poor implementation.

Key Changes and Their Impact

One significant update is the recalibration of payment calculations. Previously, IDR plans capped monthly payments at 10-20% of discretionary income, but many borrowers faced unexpected increases due to fluctuating income or family size changes. Now, the new IDR plan, known as the SAVE Plan, reduces payments to 5% of discretionary income for undergraduate loans, offering immediate relief for lower-income borrowers. For example, a borrower earning $40,000 annually with a family of three could see monthly payments drop from $200 to $100, freeing up funds for other necessities.

Addressing Administrative Failures

Another critical change involves fixing the "payment counting" system. Many borrowers in IDR plans were not receiving credit toward loan forgiveness due to administrative errors. The Department of Education is now conducting a one-time account adjustment, retroactively counting months spent in forbearance or certain repayment plans toward the 20-25 year forgiveness threshold. This means borrowers who have been in repayment for years may be closer to forgiveness than they realize—some could even qualify immediately.

Practical Steps for Borrowers

To maximize these benefits, borrowers should take proactive steps. First, enroll in the SAVE Plan by submitting an application through the Federal Student Aid website. Second, update income and family size information annually to ensure accurate payment calculations. Third, monitor loan servicer communications for updates on the account adjustment process. For those nearing forgiveness, consider requesting a payment count review to confirm eligibility.

Long-Term Implications

While these IDR changes provide substantial relief, they are not a substitute for broader loan forgiveness initiatives. Borrowers should view IDR as a bridge to financial stability, not a permanent solution. By reducing monthly payments and streamlining the path to forgiveness, these reforms empower borrowers to manage debt more effectively while advocating for systemic changes in student loan policy.

Student Loan Forgiveness and Taxes: What You Need to Report

You may want to see also

Explore related products

![]()

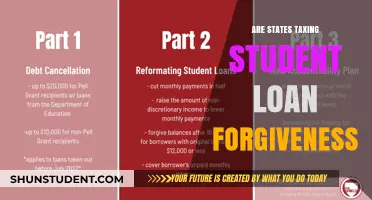

State-Level Loan Forgiveness Programs

In response to the economic strain caused by the coronavirus pandemic, several U.S. states have launched their own student loan forgiveness programs to complement federal efforts. These initiatives are tailored to address local workforce needs and economic priorities, often targeting essential sectors like healthcare, education, and public service. For instance, New York’s “Get on Your Feet” loan forgiveness program offers up to $17,500 in relief for recent graduates earning under $50,000 annually, provided they make timely payments for two years. Such programs demonstrate how states are stepping in to fill gaps left by broader federal policies.

Analyzing these state-level programs reveals a strategic focus on retaining talent in critical fields. California’s *California Loan Forgiveness Program* forgives up to $50,000 for healthcare professionals working in underserved areas, while Minnesota’s *Rural Dentist Loan Forgiveness Program* offers $25,000 annually for dentists practicing in rural communities. These targeted incentives not only alleviate individual debt burdens but also address regional shortages in essential services. Borrowers should research their state’s offerings carefully, as eligibility often hinges on profession, location, and commitment to public service.

Persuasively, state-level programs highlight the importance of localized solutions in addressing systemic issues like student debt. Unlike federal initiatives, which can be slow to adapt, state programs can respond swiftly to regional economic shifts. For example, during the pandemic, Massachusetts expanded its *MassLoan Forgiveness Program* to include additional professions, such as mental health counselors, in recognition of increased demand for their services. This flexibility underscores the value of state-driven policies in fostering economic resilience and workforce stability.

Comparatively, while federal loan forgiveness programs like Public Service Loan Forgiveness (PSLF) offer broad relief, state programs often provide more accessible pathways to forgiveness. For instance, Pennsylvania’s *PA Forward Loan Forgiveness Program* forgives up to $10,000 for graduates working in STEM fields, with no requirement for prior federal loan consolidation. Such programs reduce bureaucratic hurdles, making relief more attainable for borrowers. However, applicants must weigh state-specific requirements against federal options to determine the best fit for their circumstances.

Practically, borrowers should take proactive steps to maximize their chances of qualifying for state-level forgiveness. First, identify programs aligned with your profession and location using resources like the American Student Assistance (ASA) database. Second, maintain detailed records of employment and loan payments, as these are frequently required for applications. Finally, stay informed about program deadlines and updates, as funding and eligibility criteria can change annually. By leveraging these state-specific opportunities, borrowers can significantly reduce their debt burden while contributing to their communities.

Student Nurse Loans: Forgiveness Eligibility Explained for Aspiring Nurses

You may want to see also

Frequently asked questions

Yes, the CARES Act and subsequent extensions provided temporary relief, including paused payments, 0% interest, and stopped collections. However, broad forgiveness beyond these measures has not been implemented.

No, there is no universal forgiveness for all student loans. Only specific programs, like Public Service Loan Forgiveness (PSLF) or targeted relief for certain borrowers, have been expanded.

No, private student loans are not covered by federal coronavirus relief measures. Only federal student loans qualify for the temporary benefits.

The payment pause has been extended multiple times, with the most recent extension ending on August 31, 2022. Borrowers should check updates from the Department of Education for the latest information.

Not automatically. However, you may qualify for income-driven repayment plans with lower payments or explore options like unemployment deferment. Broad forgiveness based on job loss is not available.