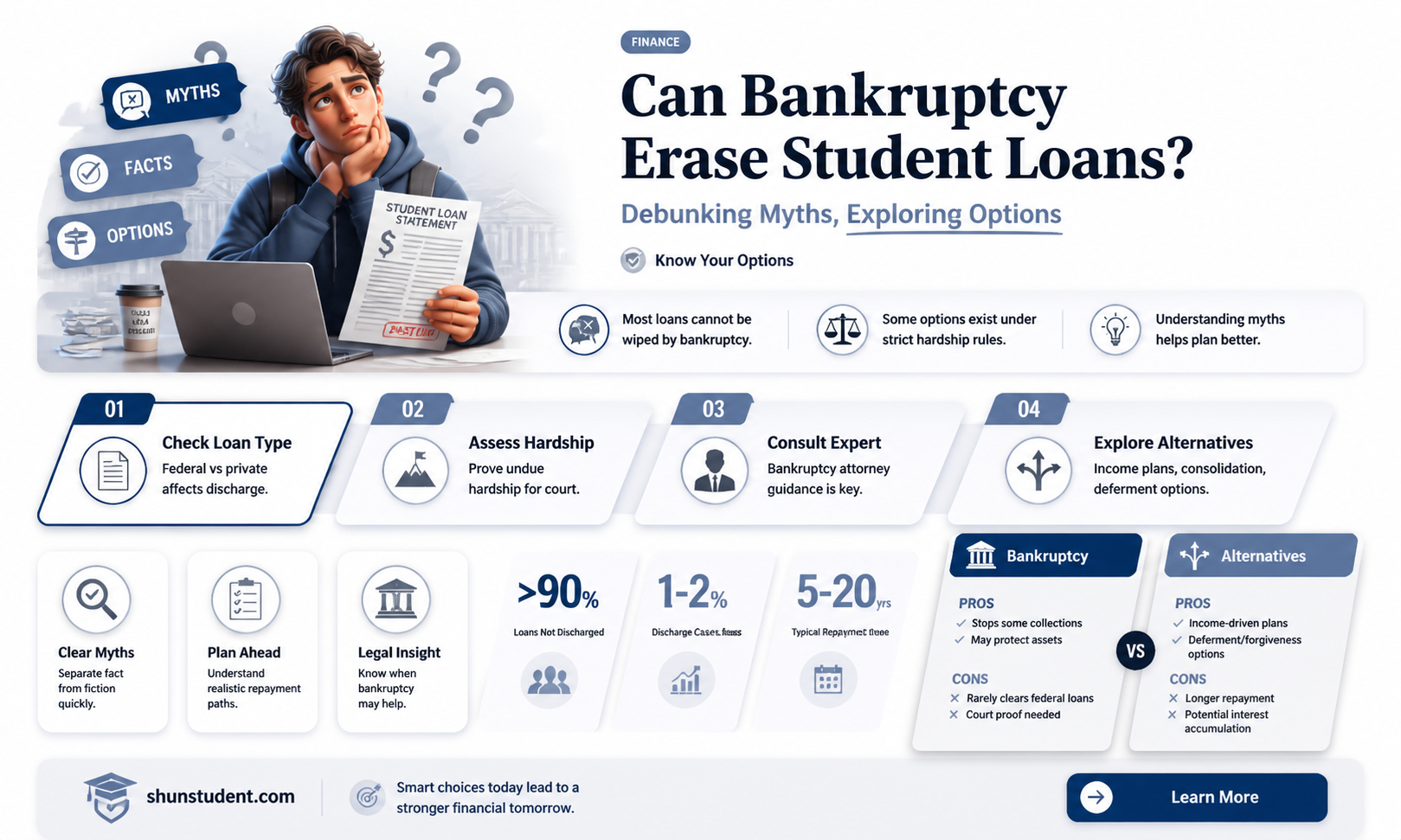

Student loan debt is a significant burden for many individuals, and the question of whether these loans can be discharged through bankruptcy is a common concern. While it is notoriously difficult to have student loans forgiven through bankruptcy, it is not entirely impossible. Under current U.S. law, borrowers must prove undue hardship through a separate legal process known as an adversary proceeding, which requires demonstrating that repaying the loans would cause an insurmountable financial burden. This standard is stringent and rarely met, but recent legal developments and policy changes have sparked discussions about potential reforms to make student loan discharge in bankruptcy more accessible. As a result, understanding the current landscape and exploring possible avenues for relief remains crucial for those overwhelmed by student debt.

| Characteristics | Values |

|---|---|

| Eligibility for Discharge | Extremely rare; requires proving "undue hardship" under the Brunner Test. |

| Brunner Test Criteria | 1. Cannot maintain minimal living standard if forced to repay. |

| 2. Circumstances unlikely to change. | |

| 3. Made good faith effort to repay. | |

| Types of Student Loans Covered | Both federal and private student loans. |

| Court Process | Requires filing an adversary proceeding in bankruptcy court. |

| Success Rate | Less than 0.1% of bankruptcy filers attempt; even fewer succeed. |

| Impact on Credit Score | Bankruptcy filing severely damages credit score for 7–10 years. |

| Alternatives to Bankruptcy | Income-Driven Repayment Plans, Loan Forgiveness Programs, etc. |

| Recent Legal Changes | No significant changes; "Fresh Start Through Bankruptcy Act" (proposed but not law). |

| Attorney Requirement | Highly recommended due to complexity of the process. |

| Time Frame | Lengthy process, often taking months to years for resolution. |

| Tax Implications | Discharged debt may be considered taxable income (consult a tax advisor). |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Loan Discharge

Declaring bankruptcy does not automatically erase student loans, but specific eligibility criteria can lead to loan discharge under rare circumstances. The process hinges on proving "undue hardship," a stringent legal standard that varies by jurisdiction. In the U.S., for instance, the Brunner Test is commonly used, requiring borrowers to demonstrate three conditions: inability to maintain a minimal standard of living, persistence of this condition, and good-faith efforts to repay the loans. This bar is exceptionally high, with only about 0.1% of bankruptcy filers successfully discharging student loans.

To initiate this process, borrowers must file an adversary proceeding within their bankruptcy case, a separate lawsuit specifically targeting the student loans. This step requires legal representation and incurs additional court fees, typically ranging from $500 to $3,000. Documentation is critical; borrowers must provide evidence of income, expenses, medical conditions, and repayment history to support their claim of undue hardship. For example, a 45-year-old borrower with permanent disability, monthly income of $1,500, and $50,000 in student loans might have a stronger case than a 30-year-old with temporary unemployment and no medical issues.

Comparatively, other countries have more lenient policies. In Canada, student loans can be discharged if the borrower has been out of school for seven years (or five years with proof of financial hardship). In the UK, student loans are written off after 30 years, regardless of repayment status. These examples highlight the U.S. system’s rigidity and underscore the importance of understanding local laws. Borrowers should consult a bankruptcy attorney specializing in student loans to assess their eligibility and navigate the complex legal landscape.

A persuasive argument for reform emerges when examining the human cost of unmanageable student debt. For instance, a single parent earning $30,000 annually with $100,000 in loans faces a monthly payment of $1,000 under standard repayment plans, leaving just $1,700 for rent, food, and other essentials. Such scenarios illustrate why the current eligibility criteria for discharge are often criticized as inhumane. Advocacy groups propose alternatives, such as lowering the undue hardship threshold or creating income-driven repayment plans with forgiveness after 10–15 years, as seen in programs like Public Service Loan Forgiveness (PSLF).

In conclusion, while declaring bankruptcy can theoretically discharge student loans, the eligibility criteria are narrowly defined and difficult to meet. Borrowers must prove undue hardship through a costly and time-consuming legal process, with success rates near zero. Practical steps include gathering comprehensive financial and medical documentation, seeking specialized legal counsel, and exploring alternative relief programs. Understanding these criteria empowers borrowers to make informed decisions and advocate for systemic changes that address the broader student debt crisis.

Do I Qualify for Student Debt Forgiveness? A Clear Guide

You may want to see also

Explore related products

![]()

Chapter 7 vs. Chapter 13 Bankruptcy

Declaring bankruptcy doesn’t automatically erase student loans, but the type of bankruptcy you file—Chapter 7 or Chapter 13—can significantly impact your strategy for managing this debt. While both chapters require proving "undue hardship" through an adversary proceeding to discharge student loans, their structures and timelines differ, offering distinct paths for financial relief.

Chapter 7: The Liquidation Option

Chapter 7 bankruptcy, often called liquidation bankruptcy, is a swift process designed to discharge unsecured debts within 3-6 months. It involves selling non-exempt assets to pay creditors, though many filers retain most possessions due to state and federal exemptions. For student loans, Chapter 7’s primary advantage is its speed; if you qualify for undue hardship, the discharge process can begin immediately. However, the hurdle is high: courts use the Brunner Test to assess whether repaying loans would prevent you from maintaining a minimal standard of living, if your circumstances are likely to persist, and if you’ve made good-faith efforts to repay. Most filers fail this test, but Chapter 7’s quick resolution allows you to focus on the adversary proceeding without long-term repayment obligations.

Chapter 13: The Repayment Plan

Chapter 13 bankruptcy, a reorganization plan, spans 3-5 years and requires repaying debts through a court-approved plan. While student loans aren’t discharged during this period, they’re treated as non-priority unsecured debts, meaning they receive minimal repayment. The key benefit is the ability to pause collections and lower monthly payments during the plan. If you file an adversary proceeding for undue hardship, Chapter 13 buys time to build a stronger case. Additionally, any remaining student loan balance after completing the plan may be discharged if the court rules in your favor, though this is rare.

Strategic Differences: Timing and Flexibility

Choosing between Chapter 7 and Chapter 13 depends on your financial goals and ability to prove undue hardship. Chapter 7 is ideal if you’re confident in your case and seek immediate relief from other debts, freeing resources to focus on the adversary proceeding. Chapter 13 suits those needing breathing room to stabilize finances while pursuing hardship discharge. For example, a disabled borrower with no income might opt for Chapter 7, while a part-time worker with fluctuating income could benefit from Chapter 13’s structured repayment plan.

Practical Tips for Both Paths

Regardless of the chapter, consult a bankruptcy attorney specializing in student loan discharge. Document all attempts to repay loans, medical conditions, and financial hardships to strengthen your undue hardship case. In Chapter 13, prioritize completing the repayment plan to maximize the chance of discharge. For Chapter 7, act quickly to file the adversary proceeding before your case closes. Remember, bankruptcy won’t guarantee student loan forgiveness, but it can provide a framework to challenge this debt while addressing other financial burdens.

Avoid Scams: Safely Report Student Loan Forgiveness Fraud Today

You may want to see also

Explore related products

![]()

Undue Hardship Requirements

Declaring bankruptcy doesn’t automatically erase student loans. Borrowers must prove "undue hardship" through a separate legal process known as an adversary proceeding. This stringent standard, established by the *Brunner test* in most jurisdictions, requires demonstrating three conditions: inability to maintain a minimal standard of living, persistence of this condition, and good-faith efforts to repay the loans. Meeting these criteria is notoriously difficult, with approval rates historically below 1%.

Consider the case of *Educational Credit Management Corp. v. Frushour* (2005), where a borrower with severe health issues and limited income still failed to meet the undue hardship standard. The court ruled that her condition, while challenging, did not guarantee lifelong inability to work. Such cases highlight the narrow interpretation of "undue hardship," often requiring extreme circumstances like permanent disability or terminal illness. For instance, a 60-year-old borrower with chronic health issues and no retirement savings might have a stronger case than a 30-year-old with temporary unemployment.

To navigate this process, borrowers should gather comprehensive documentation: medical records, income statements, and repayment history. Consulting a bankruptcy attorney specializing in student loans is critical, as they can assess the viability of an undue hardship claim. For example, a borrower earning $20,000 annually with $100,000 in loans and no prospect of higher income might qualify, but only if they can prove sustained efforts to repay, such as enrolling in income-driven repayment plans.

Critics argue the undue hardship standard is too rigid, trapping borrowers in lifelong debt. Proponents counter that it prevents abuse of bankruptcy protections. Regardless, recent trends suggest slight shifts: some courts are applying the *Totality of Circumstances* test, which considers factors beyond the Brunner criteria. For instance, in *In re Roth* (2020), a Massachusetts court discharged $221,000 in student loans for a borrower with mental health issues and minimal income, signaling potential flexibility in certain districts.

Practical tip: If pursuing an undue hardship claim, focus on demonstrating long-term incapacity, not short-term struggles. For example, a 55-year-old with arthritis and $150,000 in loans might emphasize their inability to retrain for a higher-paying job due to age and health. Pair this with evidence of consistent repayment attempts, such as rejected requests for loan consolidation or forbearance. While success isn’t guaranteed, a well-documented, attorney-guided approach maximizes the odds of discharge.

FHA and Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Private vs. Federal Loan Treatment

Declaring bankruptcy does not automatically erase student loans, but the treatment differs sharply between private and federal loans. Federal student loans are notoriously difficult to discharge in bankruptcy, requiring borrowers to prove "undue hardship" through a separate legal process known as an adversary proceeding. This standard, established by the *Brunner test*, demands evidence of extreme financial distress, a lack of improvement in circumstances, and good-faith efforts to repay the debt. Success rates are low, often leaving borrowers with limited relief. Private student loans, however, may be more amenable to discharge, as they are not shielded by federal protections. While still challenging, private lenders cannot impose the same stringent hardship requirements, making bankruptcy a potentially viable, though not guaranteed, option for eliminating this debt.

To navigate this landscape, borrowers must understand the procedural differences. Federal loans require filing an adversary proceeding within the bankruptcy case, a costly and time-consuming step that involves presenting extensive financial documentation and testimony. Private loans, by contrast, are treated like other unsecured debts in bankruptcy, meaning they can be discharged without the same burden of proof. However, private lenders may contest the discharge, arguing that their loans meet federal loan criteria or that the borrower’s financial situation does not warrant relief. Borrowers should consult an attorney experienced in student loan bankruptcy cases to assess their chances and prepare a strong case.

A critical takeaway is that federal loan forgiveness through bankruptcy is rare, while private loan discharge is more feasible but still uncertain. For federal loans, alternatives like income-driven repayment plans, public service loan forgiveness, or disability discharge may offer more practical paths to relief. Private loans, however, lack such federal programs, making bankruptcy a more attractive, albeit risky, strategy. Borrowers should weigh the long-term impact of bankruptcy on their credit score and financial future against the potential benefits of debt elimination.

Practical tips include gathering comprehensive financial records, including income, expenses, and repayment history, to support a hardship claim. For private loans, borrowers should scrutinize loan agreements for any clauses that might affect dischargeability, such as language mimicking federal loan protections. Additionally, exploring settlement options with private lenders before filing for bankruptcy can sometimes yield negotiated reductions or waivers. Ultimately, the private vs. federal loan distinction is pivotal in determining whether bankruptcy offers a realistic path to student loan forgiveness.

Nonprofit Student Loan Forgiveness: Eligibility and Application Guide

You may want to see also

Explore related products

![]()

Impact on Credit Score

Declaring bankruptcy to discharge student loans is notoriously difficult, but even if successful, the process leaves a lasting mark on your credit score. A bankruptcy filing typically stays on your credit report for 7 to 10 years, acting as a red flag to future lenders. This negative entry can slash your credit score by 160 to 220 points, depending on your initial creditworthiness. For context, a score drop of this magnitude can push someone from "good" credit territory (670-739) into "fair" or even "poor" ranges, severely limiting access to credit cards, loans, and favorable interest rates.

The impact isn’t just immediate; it’s a long-term financial handicap. Lenders view bankruptcy as a high-risk indicator, often translating to higher interest rates or outright denials for mortgages, auto loans, and personal loans. For instance, a borrower with a pre-bankruptcy score of 720 might see their mortgage APR jump from 4.5% to 6.5% post-bankruptcy, adding tens of thousands of dollars in interest over the life of a 30-year loan. Even securing a credit card may require a secured option with a hefty deposit, and unsecured cards often come with exorbitant fees and low limits.

However, the damage isn’t permanent. Strategic credit rebuilding can mitigate the effects over time. Start by obtaining a secured credit card with a limit of $200 to $500, ensuring timely payments to establish a positive payment history. Simultaneously, become an authorized user on a trusted individual’s credit card to inherit their positive credit behavior. Keep credit utilization below 30%—ideally under 10%—and avoid opening multiple accounts at once, as hard inquiries further dent your score. Within 2 to 3 years of consistent effort, you can see a gradual score improvement, though full recovery may take the full 7 to 10 years until the bankruptcy drops off your report.

It’s also crucial to monitor your credit report for inaccuracies, as errors can exacerbate the damage. Dispute any discrepancies with the credit bureaus immediately. Additionally, consider working with a credit counselor or financial advisor to create a tailored recovery plan. While bankruptcy may offer relief from overwhelming student debt, the credit score consequences demand proactive management to reclaim financial stability.

Do Government Employees Qualify for Student Loan Forgiveness?

You may want to see also

Frequently asked questions

No, student loans are not automatically forgiven when you declare bankruptcy. They are typically considered non-dischargeable debts, meaning they remain your responsibility unless you can prove undue hardship through an adversary proceeding in bankruptcy court.

Yes, but it’s rare and requires meeting the "undue hardship" standard. You must file a separate lawsuit within your bankruptcy case and prove that repaying the loans would cause you and your dependents insurmountable financial difficulty, with no likelihood of improvement.

Both federal and private student loans can potentially be discharged in bankruptcy, but the process is the same for both. You must still meet the undue hardship criteria, which is a high bar to clear and requires substantial evidence of financial distress.