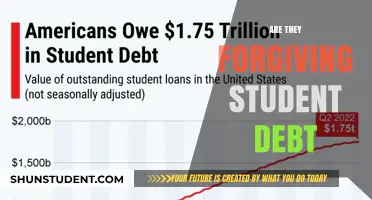

The topic of student loan forgiveness has become a pressing issue for millions of borrowers in the United States, as the burden of educational debt continues to weigh heavily on individuals and the economy. With the average student loan debt surpassing $30,000 per borrower, many are left wondering if relief is on the horizon. Discussions surrounding widespread student loan forgiveness have gained momentum, fueled by advocacy groups, policymakers, and the Biden administration's campaign promises. While targeted forgiveness programs have already provided relief to specific groups, such as public service workers and those defrauded by for-profit institutions, the question remains: will there be broader, more comprehensive student loan forgiveness for all borrowers? As debates continue over the feasibility, cost, and fairness of such a measure, borrowers anxiously await clarity on whether their financial futures will be alleviated by this potential policy change.

| Characteristics | Values |

|---|---|

| Current Status | As of October 2023, widespread student loan forgiveness remains uncertain. Biden's previous forgiveness plan was blocked by the Supreme Court in June 2023. |

| Supreme Court Ruling | Struck down Biden's plan to forgive up to $20,000 in federal student loans per borrower, citing lack of congressional authorization. |

| Existing Forgiveness Programs | Programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment (IDR) plans still exist but have specific eligibility requirements. |

| Biden Administration Efforts | Exploring alternative pathways for targeted relief, such as fixing IDR plans and expanding eligibility for existing programs. |

| Legislative Efforts | No major bipartisan student loan forgiveness legislation has passed Congress. |

| Loan Payments Resumed | Federal student loan payments resumed in October 2023 after a three-year pandemic-related pause. |

| Interest Rates | Interest began accruing again on federal student loans in September 2023. |

| Public Opinion | Divided, with some supporting broad forgiveness and others opposing it due to concerns about fairness and cost. |

| Economic Impact | Forgiveness could stimulate the economy by increasing disposable income but raises concerns about inflation and taxpayer burden. |

| Future Outlook | Uncertain, dependent on legislative action, legal challenges, and administrative measures by the Biden administration. |

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for forgiveness based on income, loan type, and repayment plan

- Amount of Forgiveness: Partial or full forgiveness What determines the forgiven amount

- Timeline for Implementation: When will forgiveness be applied Immediate or phased rollout

- Tax Implications: Will forgiven loans be taxed as income State vs. federal rules

- Political and Legal Challenges: Potential lawsuits or legislative hurdles affecting forgiveness programs

![]()

Eligibility Criteria: Who qualifies for forgiveness based on income, loan type, and repayment plan?

The path to student loan forgiveness is paved with eligibility criteria that can feel like a labyrinth. Understanding who qualifies based on income, loan type, and repayment plan is crucial for navigating this complex process. Let's break it down.

Income-Driven Repayment Plans: The Gateway to Forgiveness

For many borrowers, income-driven repayment (IDR) plans are the key to unlocking loan forgiveness. These plans cap your monthly payments at a percentage of your discretionary income, typically 10-20%. After a set period, usually 20-25 years, any remaining balance is forgiven. To qualify, you must demonstrate financial need through your income and family size. For instance, a single borrower earning $40,000 annually might qualify for significantly lower payments under an IDR plan compared to the standard 10-year repayment schedule.

Loan Type Matters: Not All Loans Are Created Equal

Not all student loans are eligible for forgiveness programs. Federal Direct Loans, including Direct Subsidized, Unsubsidized, PLUS, and Consolidation Loans, are generally eligible for IDR plans and Public Service Loan Forgiveness (PSLF). Private student loans, on the other hand, are typically excluded from these programs. If you have a mix of federal and private loans, focus on prioritizing repayment strategies for your federal loans to maximize your forgiveness potential.

Public Service Loan Forgiveness: A Faster Track for Public Servants

PSLF offers a faster route to forgiveness for borrowers working full-time in qualifying public service jobs. After making 120 qualifying payments (10 years) under an IDR plan while employed in public service, the remaining balance is forgiven tax-free. This program is particularly beneficial for borrowers with high debt burdens who are committed to careers in government, education, healthcare, or other eligible sectors.

Navigating the Maze: Practical Tips

- Research and Understand Your Options: Carefully review the eligibility criteria for each forgiveness program. The Federal Student Aid website (studentaid.gov) is a valuable resource.

- Choose the Right Repayment Plan: Select an IDR plan that aligns with your income and financial goals.

- Certify Your Income Annually: Regularly recertify your income to ensure your monthly payments remain affordable and you stay on track for forgiveness.

- Track Your Payments: Keep meticulous records of your loan payments and employment history, especially if pursuing PSLF.

Remember, student loan forgiveness is not automatic. By understanding the eligibility criteria and taking proactive steps, you can increase your chances of achieving financial freedom from student debt.

Can Defaulted Student Loans Be Forgiven? Exploring Your Options

You may want to see also

Explore related products

![]()

Amount of Forgiveness: Partial or full forgiveness? What determines the forgiven amount?

The debate over student loan forgiveness often hinges on whether borrowers will receive partial or full relief. While full forgiveness captures headlines, partial forgiveness is more common in existing programs. For instance, the Public Service Loan Forgiveness (PSLF) program forgives the remaining balance after 120 qualifying payments, but only for those in eligible public service jobs. Similarly, income-driven repayment (IDR) plans forgive remaining debt after 20–25 years of payments, but the forgiven amount is taxed as income. These examples illustrate that the extent of forgiveness is rarely universal and often tied to specific conditions.

Determining the forgiven amount involves a complex interplay of factors, including the borrower’s income, loan type, and repayment plan. For example, IDR plans cap monthly payments at a percentage of discretionary income, typically 10–20%, depending on the plan. After the repayment period, the remaining balance is forgiven, but the total forgiven amount depends on how much was paid over time. Borrowers with lower incomes and higher debt balances are more likely to receive substantial forgiveness, while those with higher incomes may see minimal relief. This variability underscores the need for borrowers to understand their specific circumstances.

Proponents of full forgiveness argue it provides immediate economic relief and addresses systemic inequities in education funding. However, critics counter that it could disproportionately benefit higher-earning graduates and strain federal budgets. Partial forgiveness, on the other hand, is often seen as a more targeted approach, balancing relief with fiscal responsibility. For instance, President Biden’s 2022 plan forgave up to $20,000 for Pell Grant recipients and $10,000 for others, demonstrating how policy can differentiate forgiveness based on need. Such tiered approaches aim to maximize impact while minimizing cost.

To navigate these possibilities, borrowers should take proactive steps. First, assess eligibility for existing programs like PSLF or IDR plans. Second, monitor legislative updates, as policy changes can expand or limit forgiveness opportunities. Third, consider consulting a financial advisor to weigh the long-term implications of forgiveness, such as tax liabilities. By staying informed and strategic, borrowers can position themselves to benefit from whatever forgiveness measures emerge. Ultimately, the amount forgiven will depend on a combination of policy design, individual circumstances, and political will.

Student Loan Consolidation: Can It Lead to Debt Forgiveness?

You may want to see also

Explore related products

![]()

Timeline for Implementation: When will forgiveness be applied? Immediate or phased rollout?

The timeline for implementing student loan forgiveness is a critical factor in determining its impact on borrowers. An immediate rollout would provide instant relief, but it poses significant logistical challenges. Processing millions of accounts simultaneously could overwhelm servicers, leading to errors and delays in disbursement. For instance, the Public Service Loan Forgiveness (PSLF) program faced years of administrative hurdles, with only a fraction of applicants initially approved. An immediate approach, while appealing, risks repeating these mistakes on a larger scale.

A phased rollout, on the other hand, offers a more controlled approach. By categorizing borrowers based on factors like loan type, income level, or years in repayment, the government could prioritize those most in need. For example, borrowers with incomes below a certain threshold or those in default could be forgiven first. This method reduces administrative strain and ensures a smoother process. However, it may delay relief for some borrowers, potentially dampening the program’s immediate economic impact.

From a persuasive standpoint, a hybrid model could strike a balance. Immediate forgiveness for smaller loan balances (e.g., under $10,000) could provide quick wins, while larger balances are phased in over time. This approach would deliver tangible benefits to a significant portion of borrowers while managing the workload for servicers. For instance, forgiving $10,000 per borrower immediately could eliminate debt for nearly 15 million people, according to federal data, while the remaining balances are addressed in subsequent phases.

Comparatively, the timeline also depends on legislative and political factors. If forgiveness is tied to executive action, implementation could be swift but subject to legal challenges. Conversely, congressional approval might ensure stability but could introduce delays due to partisan gridlock. Borrowers should monitor policy updates and prepare documentation in advance, such as income verification or loan history, to expedite their case when the program rolls out.

In conclusion, the timeline for student loan forgiveness hinges on a trade-off between speed and efficiency. While an immediate rollout offers instant relief, a phased or hybrid approach may be more practical. Borrowers should stay informed and proactive, as the chosen timeline will directly affect when and how they experience financial relief.

Can My Student Loans Be Forgiven? A Comprehensive Guide to Relief

You may want to see also

Explore related products

$9.99 $12.99

![]()

Tax Implications: Will forgiven loans be taxed as income? State vs. federal rules

Forgiven student loans can trigger a tax bill, but the rules aren't one-size-fits-all. Federally, the American Rescue Plan Act of 2021 temporarily excludes forgiven student loans from taxable income through 2025. This means if your loans are forgiven under federal programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans during this period, you won’t owe federal taxes on the forgiven amount. However, this exclusion expires in 2026, so future forgiveness could be taxable unless Congress extends the provision.

State tax treatment complicates matters further. While federal law excludes forgiven loans from taxable income for now, some states don’t conform to this rule. For example, states like California and New York align with federal exclusions, but others, such as Massachusetts and Virginia, may still tax forgiven amounts as income. Borrowers must check their state’s tax laws to avoid unexpected liabilities. For instance, if you live in a non-conforming state and $50,000 of your loans are forgiven, you could owe state taxes on that amount even if federal taxes are waived.

Practical tip: If you’re pursuing loan forgiveness, consult a tax professional to understand both federal and state implications. For example, if you’re nearing PSLF eligibility, factor in potential state taxes when planning your finances. Additionally, keep detailed records of forgiven amounts and tax filings to ensure compliance with both federal and state requirements.

The interplay between federal and state rules underscores the need for careful planning. While federal exclusions provide temporary relief, state taxes can still erode the financial benefit of loan forgiveness. Borrowers in states with non-conforming tax laws may need to set aside funds to cover state tax obligations. For instance, if your forgiven amount is $30,000 and your state tax rate is 5%, you’d owe $1,500 in state taxes—a significant expense if unprepared.

In conclusion, while federal tax exclusions for forgiven student loans offer temporary relief, state tax rules can offset these savings. Borrowers must navigate this dual system carefully, consulting state laws and seeking professional advice to avoid surprises. As the federal exclusion expires in 2026, staying informed about legislative changes will be crucial for long-term financial planning.

Are Current Students Eligible for Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Political and Legal Challenges: Potential lawsuits or legislative hurdles affecting forgiveness programs

The path to widespread student loan forgiveness is fraught with political and legal landmines. One immediate hurdle lies in the separation of powers. The executive branch, particularly the Department of Education, has limited authority to unilaterally forgive debt without congressional approval. While the HEROES Act and the Higher Education Act provide some leeway for targeted relief, large-scale forgiveness would likely require legislative action. This reality sets the stage for partisan gridlock, as Republicans have historically opposed broad forgiveness initiatives, arguing they unfairly burden taxpayers and reward irresponsible borrowing.

Consider the legal challenges already mounted against existing forgiveness programs. In 2022, the Supreme Court heard arguments in *Biden v. Nebraska*, a case challenging the administration’s attempt to cancel up to $20,000 in student debt per borrower. The plaintiffs, six Republican-led states, argued the administration overstepped its authority and violated the Administrative Procedure Act. This case underscores the vulnerability of forgiveness programs to legal scrutiny, particularly when they rely on executive action rather than congressional legislation. If the Court rules against the administration, it could set a precedent limiting future forgiveness efforts.

Even if legislative action were to pass, the specifics of the program would face additional hurdles. For instance, means-testing—limiting forgiveness to borrowers below a certain income threshold—could trigger lawsuits alleging unequal treatment under the law. Similarly, excluding certain types of loans (e.g., private loans) or institutions (e.g., for-profit colleges) could invite challenges based on arbitrariness or discrimination. Crafting a legally defensible program would require meticulous attention to detail, balancing equity with constitutional and statutory constraints.

Advocates for forgiveness must also contend with the political optics. Critics argue that broad forgiveness disproportionately benefits higher-income earners, who hold a disproportionate share of student debt. To counter this narrative, proponents could propose targeted relief for low-income borrowers or those in public service, but such measures risk alienating broader support. Striking the right balance between inclusivity and political feasibility is a delicate task, one that will shape the program’s chances of survival in both the legislative and judicial arenas.

In practical terms, borrowers should stay informed but cautious. While advocacy efforts continue, the legal and political landscape remains uncertain. Those eligible for existing programs like Public Service Loan Forgiveness or income-driven repayment plans should take immediate steps to enroll, as these programs are less likely to face legal challenges. For broader forgiveness, patience and persistence will be key. Engaging with policymakers, participating in public comment periods, and supporting organizations pushing for reform can amplify the collective voice demanding relief.

Postdoc Student Loan Forgiveness: Exploring Options for Debt Relief

You may want to see also

Frequently asked questions

As of now, widespread student loan forgiveness remains uncertain and depends on government policies, legal challenges, and legislative actions.

Eligibility would depend on the specific forgiveness program, but it often targets federal loan borrowers with income-driven repayment plans, public service workers, or those meeting income thresholds.

There is no definitive timeline, as it depends on ongoing legal battles, congressional decisions, and executive actions. Updates are typically announced by the Department of Education.

The amount forgiven would vary based on the program. Past proposals have suggested $10,000 to $20,000 per borrower, but this is subject to change based on final legislation or policies.