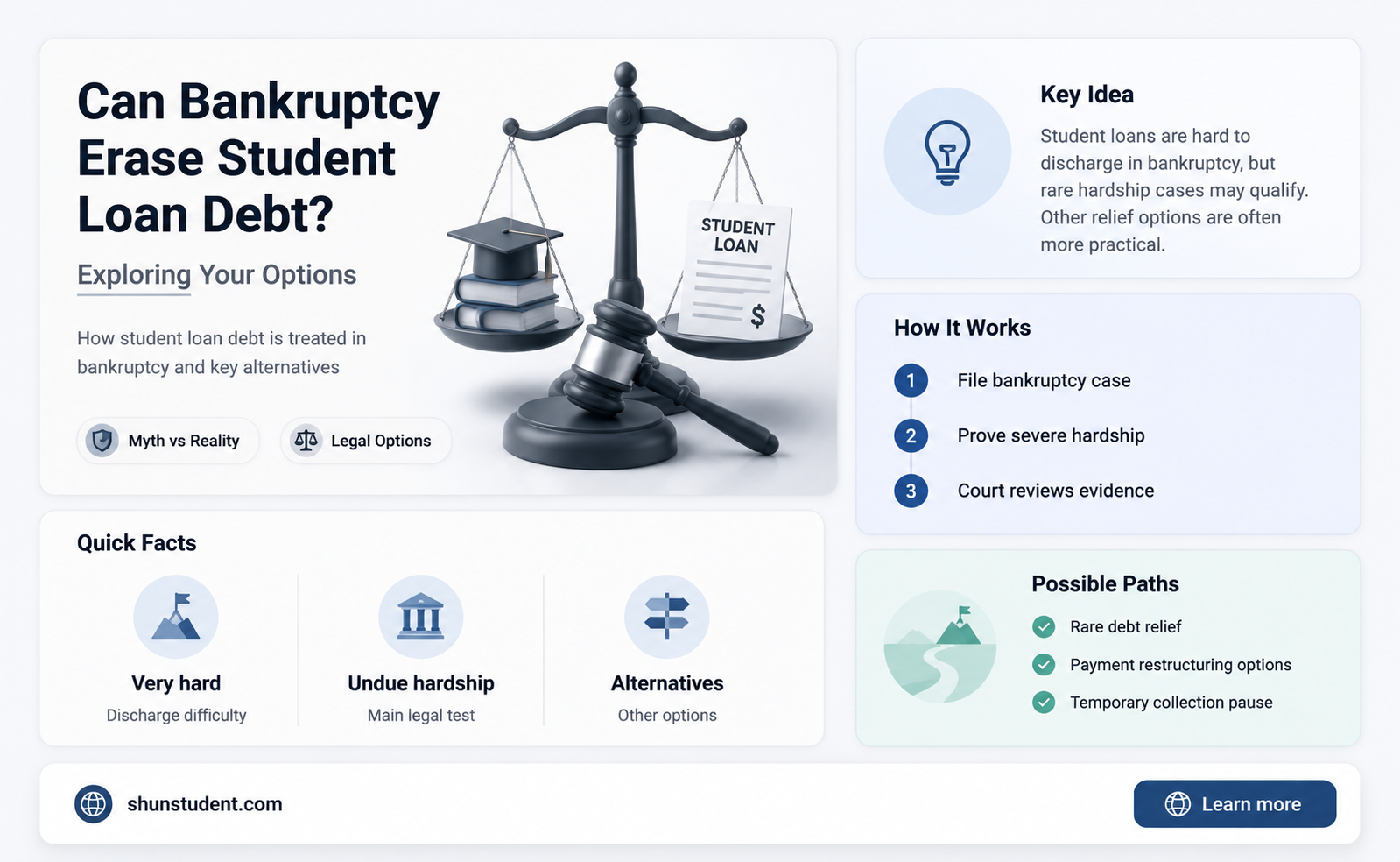

The question of whether bankruptcy can forgive student loans is a critical and complex issue for many individuals burdened by educational debt. While bankruptcy is designed to provide a fresh financial start, student loans are notoriously difficult to discharge due to stringent legal requirements. Under current U.S. bankruptcy law, borrowers must prove undue hardship through a separate legal process known as an adversary proceeding, which involves demonstrating that repaying the loans would cause insurmountable financial distress. This high bar means only a small fraction of cases succeed in discharging student debt. However, recent legal and policy discussions have highlighted potential reforms, such as the Fresh Start Through Bankruptcy Act, which aim to make it easier for borrowers to seek relief. As student loan debt continues to soar, understanding the intersection of bankruptcy and educational loans remains essential for those seeking financial freedom.

| Characteristics | Values |

|---|---|

| General Rule | Student loans are typically not dischargeable in bankruptcy. |

| Undue Hardship Exception | Loans may be discharged if the borrower proves "undue hardship" under the Brunner Test (used in most circuits). |

| Brunner Test Criteria | 1. Unable to maintain minimal standard of living. 2. Circumstances unlikely to change. 3. Good faith effort to repay. |

| Chapter 7 Bankruptcy | Rarely discharges student loans unless undue hardship is proven. |

| Chapter 13 Bankruptcy | Does not discharge loans but allows repayment through a 3-5 year plan. |

| Private vs. Federal Loans | Both types may qualify for discharge under undue hardship. |

| Recent Legal Changes (as of 2023) | No major federal changes; some states have limited relief programs. |

| Administrative Discharge Options | Separate from bankruptcy (e.g., Total and Permanent Disability Discharge). |

| Success Rate in Bankruptcy | Less than 1% of debtors attempt; ~40% succeed in proving undue hardship. |

| Legal Representation | Strongly recommended due to complexity of proving undue hardship. |

| Impact on Credit Score | Bankruptcy negatively impacts credit; discharged loans may improve finances long-term. |

Explore related products

What You'll Learn

![]()

Eligibility criteria for student loan discharge in bankruptcy

Bankruptcy offers a potential lifeline for those drowning in debt, but student loans are notoriously difficult to discharge. Unlike credit card debt or medical bills, student loans enjoy special protections under U.S. bankruptcy law. However, it's not impossible to have them forgiven through bankruptcy. The key lies in meeting the stringent eligibility criteria outlined in the Bankruptcy Code.

Understanding these criteria is crucial for anyone considering this path.

The primary hurdle is the "undue hardship" standard, a legal test established by the Brunner case. This three-pronged test requires debtors to prove: 1) They cannot maintain a minimal standard of living if forced to repay the loans, 2) Their financial situation is likely to persist for a significant portion of the repayment period, and 3) They have made good faith efforts to repay the loans. This standard is intentionally high, reflecting the policy goal of protecting taxpayer-funded education investments.

While the Brunner test is the most common framework, some courts have adopted alternative standards, such as the "totality of circumstances" test, which considers factors like age, health, earning potential, and loan balance.

Meeting the undue hardship standard often requires extensive documentation and legal representation. Debtors must provide detailed financial records, medical evidence (if applicable), and a compelling narrative demonstrating their inability to repay. It's a complex and emotionally taxing process, often requiring expert testimony and legal arguments tailored to the specific court's interpretation of the standard.

Success rates for student loan discharge through bankruptcy are low, but not nonexistent. A 2019 study found that approximately 40% of debtors who actively sought discharge were successful. This highlights the importance of careful planning, thorough documentation, and experienced legal counsel.

It's crucial to remember that bankruptcy should be a last resort. Exploring other options like income-driven repayment plans, loan forgiveness programs, or loan consolidation should be prioritized before pursuing bankruptcy. However, for those facing insurmountable student loan debt and meeting the stringent eligibility criteria, bankruptcy can offer a path towards financial freedom.

Will MOHELA Student Loans Be Forgiven? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Undue hardship requirements for loan forgiveness

Bankruptcy offers a potential escape from overwhelming debt, but student loans are notoriously difficult to discharge. The key to unlocking this rare relief lies in proving "undue hardship," a stringent legal standard that demands more than just financial strain.

Borrowers seeking student loan discharge through bankruptcy must navigate the complex terrain of the Brunner Test, a three-pronged evaluation used by most courts. This test requires demonstrating:

- Insability to Maintain a Minimal Standard of Living: This goes beyond temporary belt-tightening. It means proving that paying student loans would force you and your dependents into a life of poverty, unable to afford basic necessities like food, shelter, clothing, and healthcare.

- Persistence of Circumstances: This isn't a temporary setback. You must show that your financial hardship is likely to continue for a significant portion of the loan repayment period. This could be due to chronic illness, disability, lack of employable skills, or a depressed job market in your field.

- Good Faith Effort to Repay: Courts scrutinize your repayment history. Demonstrating a consistent effort to make payments, even if minimal, strengthens your case. Exploring alternative repayment plans and seeking loan consolidation or deferment also shows good faith.

Meeting all three prongs is a high bar, and success rates are low. However, understanding these requirements is crucial for borrowers exploring bankruptcy as a last resort. Consulting with an experienced bankruptcy attorney who specializes in student loan discharge is essential for navigating this complex process and maximizing your chances of success.

Can Parent Student Loans Be Forgiven? Exploring Options for Relief

You may want to see also

Explore related products

![]()

Chapter 7 vs. Chapter 13 bankruptcy options

Bankruptcy offers a glimmer of hope for those drowning in debt, but for student loan borrowers, it’s often a double-edged sword. While both Chapter 7 and Chapter 13 bankruptcies aim to provide relief, their approaches and outcomes differ significantly, particularly when it comes to student loans. Understanding these differences is crucial for anyone considering bankruptcy as a solution to overwhelming educational debt.

Chapter 7: The Liquidation Option

Chapter 7 bankruptcy, often referred to as "liquidation bankruptcy," is designed to discharge unsecured debts quickly, typically within 3-6 months. However, student loans are rarely forgiven under Chapter 7 unless the borrower can prove "undue hardship" through a separate legal process known as an adversary proceeding. This standard is notoriously difficult to meet, requiring evidence that repaying the loans would cause extreme financial distress, with no likelihood of improvement. For instance, a 55-year-old borrower with $100,000 in student loans, earning minimum wage, and suffering from a chronic illness might have a stronger case. Yet, even in such scenarios, success is not guaranteed. Chapter 7’s primary benefit lies in eliminating other unsecured debts, such as credit card balances, which can free up income to tackle student loans. However, it’s a high-stakes gamble for student loan forgiveness, with less than 1% of cases resulting in full or partial discharge.

Chapter 13: The Repayment Plan

Chapter 13 bankruptcy, or "reorganization bankruptcy," takes a different approach by restructuring debts into a 3- to 5-year repayment plan. While student loans are not discharged, they can be temporarily paused during the repayment period, providing immediate relief from collection efforts. For example, a 35-year-old teacher with $80,000 in student loans and $20,000 in credit card debt could use Chapter 13 to prioritize the credit card debt while freezing student loan payments. At the end of the plan, the remaining student loan balance would still be due, but the borrower might be in a better financial position to manage it. Additionally, Chapter 13 allows borrowers to challenge student loans under the undue hardship standard, though the success rate remains low. This option is particularly useful for those with steady income who need breathing room to reorganize their finances.

Key Differences and Practical Tips

The choice between Chapter 7 and Chapter 13 hinges on your financial situation and goals. Chapter 7 is faster and more straightforward but offers little direct relief for student loans. Chapter 13 provides a structured repayment plan and temporary student loan relief but requires consistent income and a long-term commitment. Practical tips include:

- Consult an attorney specializing in bankruptcy and student loans to assess your eligibility for undue hardship.

- Evaluate your income and assets—Chapter 7 has strict income limits, while Chapter 13 requires sufficient income to fund the repayment plan.

- Consider alternatives like income-driven repayment plans or loan consolidation before pursuing bankruptcy.

The Takeaway

While neither Chapter 7 nor Chapter 13 guarantees student loan forgiveness, they offer distinct strategies for managing debt. Chapter 7 is a quick fix for unsecured debts but rarely touches student loans, while Chapter 13 provides temporary relief and a structured approach to overall debt management. For student loan borrowers, bankruptcy is a last resort, but understanding these options can help navigate the complexities of financial recovery.

Nursing Home Workers: Unlocking Student Loan Forgiveness Opportunities

You may want to see also

Explore related products

![]()

Legal process for filing adversary proceedings

Bankruptcy offers a potential lifeline for those drowning in debt, but student loans are notoriously difficult to discharge. The legal process for filing adversary proceedings within a bankruptcy case is a critical, yet complex, avenue for seeking relief from these obligations. This process requires a debtor to prove that repaying the student loans would cause an "undue hardship," a stringent standard set by the Bankruptcy Code.

The first step in initiating an adversary proceeding is filing a complaint with the bankruptcy court. This document must outline the debtor's financial situation, the nature of the student loans, and the reasons why repayment constitutes an undue hardship. It's crucial to provide detailed evidence, such as medical records, employment history, and budget statements, to support the claim. For instance, a 45-year-old debtor with a chronic illness, limited income, and no prospect of increased earnings might have a stronger case compared to a recent graduate with a high-earning potential.

Once the complaint is filed, the court will schedule a trial, typically within 60 to 90 days. During this period, both the debtor and the loan servicer can engage in discovery, exchanging relevant documents and information. This phase is vital for building a robust case. For example, if a debtor argues that their disability prevents them from maintaining a stable income, they should gather medical expert testimonies and employment records to substantiate this claim. The court may also allow for mediation, providing an opportunity to reach a settlement without a full trial.

The trial itself is a formal proceeding where both parties present their arguments and evidence. The debtor must demonstrate that they have made good faith efforts to repay the loans and that their financial situation is unlikely to improve. The Brunner Test, used in most jurisdictions, requires proving that (1) the debtor cannot maintain a minimal standard of living if forced to repay, (2) this situation is likely to persist, and (3) they have made good faith efforts to repay. A persuasive narrative, backed by concrete evidence, is key to success.

After the trial, the judge will issue a ruling, which can be appealed by either party. If the debtor prevails, the student loans may be partially or fully discharged. However, the process is arduous and success is not guaranteed. It's essential to consult with an experienced bankruptcy attorney who can navigate the intricacies of adversary proceedings and increase the chances of a favorable outcome. This legal battle is not for the faint-hearted, but for those facing insurmountable student debt, it may be the only path to financial freedom.

Disabilities That Qualify for Student Loan Forgiveness: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact of bankruptcy on credit and loan repayment

Bankruptcy’s impact on credit and loan repayment is a double-edged sword, particularly when student loans are involved. Filing for bankruptcy can provide immediate relief from overwhelming debt, but it comes with long-term consequences that reshape financial opportunities. For instance, a Chapter 7 bankruptcy remains on your credit report for 10 years, while Chapter 13 stays for 7 years. This significantly lowers your credit score, often by 160 to 220 points, making it harder to secure loans, credit cards, or even rent an apartment. Lenders view bankruptcy as a red flag, signaling high risk, which translates to higher interest rates or stricter terms if you do qualify for credit.

Student loans, however, are rarely discharged through bankruptcy. Under the *Brunner Test*, you must prove "undue hardship," a stringent standard requiring evidence of extreme financial distress, good-faith repayment efforts, and long-term inability to repay. Few cases meet this criteria, meaning most student loan debt survives bankruptcy. This creates a paradox: while bankruptcy may clear other debts, student loans persist, leaving you with a damaged credit profile and ongoing repayment obligations. For example, if you owe $50,000 in student loans and $20,000 in credit card debt, bankruptcy might eliminate the latter but leave you with the former, plus a credit score in the 500s.

Rebuilding credit post-bankruptcy requires strategic action. Start by obtaining a secured credit card with a deposit of $200 to $500, ensuring timely payments to demonstrate reliability. Pay all bills on time, keep credit utilization below 30%, and avoid new debt. Within 12 to 24 months, you may see your score rise into the 600s, gradually improving access to better loan terms. However, student loans remain a constant, and missed payments further damage your credit. Enrolling in income-driven repayment plans or applying for forbearance can provide temporary relief, but interest continues to accrue, increasing the total debt burden.

Comparatively, bankruptcy’s impact on loan repayment differs from other debt relief options. Debt settlement, for instance, may reduce total debt but harms credit less severely than bankruptcy. Student loan forgiveness programs, like Public Service Loan Forgiveness (PSLF), offer a path to debt elimination after 10 years of qualifying payments, but bankruptcy does not accelerate this process. In fact, bankruptcy can disqualify you from certain federal loan benefits, such as deferment or forbearance, during the repayment period.

Ultimately, bankruptcy’s role in credit and loan repayment is complex, especially with student loans. While it can provide a fresh start by eliminating unsecured debts, it does not guarantee student loan forgiveness and severely damages credit. Practical steps like secured credit cards, disciplined repayment, and exploring alternative relief programs are essential to mitigate long-term harm. Before filing, weigh the immediate relief against the enduring consequences, ensuring you’re prepared to navigate the financial aftermath.

Do Students Embrace Grade Forgiveness in College? Insights and Opinions

You may want to see also

Frequently asked questions

No, bankruptcy does not automatically forgive student loans. Student loans are generally considered non-dischargeable unless the borrower can prove "undue hardship" through an adversary proceeding in bankruptcy court.

The "undue hardship" test varies by jurisdiction but typically requires proving that repaying the loans would cause extreme financial difficulty, that the hardship is likely to persist, and that the borrower has made good-faith efforts to repay the loans.

As of now, there are no widespread changes to bankruptcy laws that automatically make student loans dischargeable. However, legislative proposals and court rulings occasionally emerge, so it’s important to consult a bankruptcy attorney for the most current information.