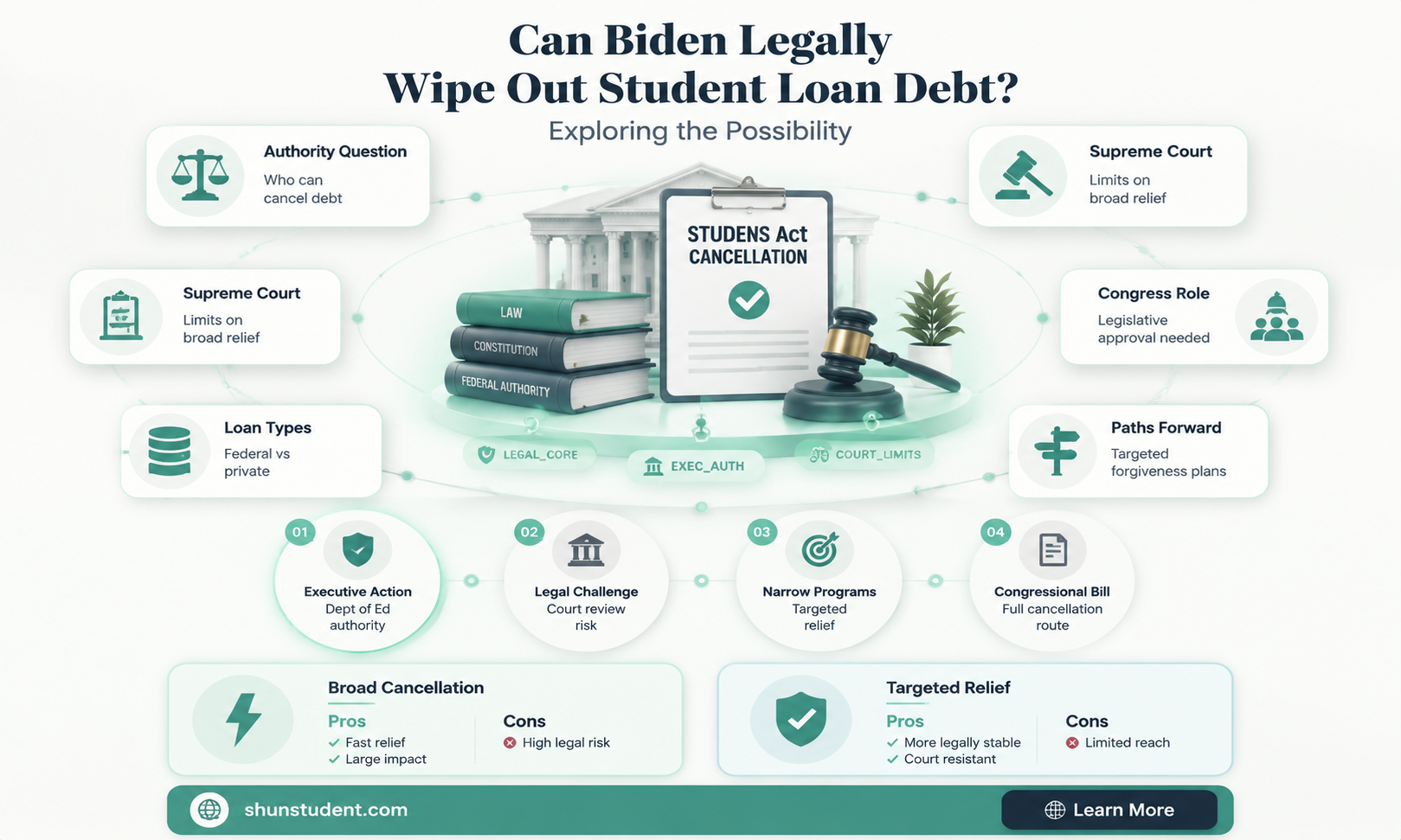

The question of whether President Biden can legally forgive student loan debt has sparked intense debate and scrutiny, as millions of Americans grapple with the burden of skyrocketing educational costs. Biden’s campaign promise to cancel at least $10,000 in student debt per borrower, and up to $50,000 for certain groups, has faced legal and political challenges, with critics arguing it exceeds executive authority and requires congressional approval. Proponents, however, point to the Higher Education Act’s provisions allowing the Secretary of Education to modify or waive federal student loans in times of national emergency, such as the COVID-19 pandemic. The Supreme Court’s 2023 ruling striking down Biden’s initial debt relief plan further complicated matters, leaving borrowers and policymakers awaiting clarity on the administration’s next steps and the constitutional limits of executive power in addressing this pressing issue.

| Characteristics | Values |

|---|---|

| Legal Authority | Biden's authority to forgive student loan debt is debated. The Higher Education Act of 1965 is cited as a potential source of authority, but its scope is unclear. |

| Executive Action | Biden has used executive action to forgive limited amounts of student debt, such as for defrauded students and those with disabilities. |

| Broad Forgiveness | As of October 2023, Biden's attempt at broad student loan forgiveness (up to $20,000 per borrower) was blocked by the Supreme Court in June 2023 in the case Biden v. Nebraska. |

| Supreme Court Ruling | The Supreme Court ruled 6-3 that Biden's broad forgiveness plan exceeded executive authority under the HEROES Act. |

| HEROES Act | The HEROES Act allows the Secretary of Education to modify student loan terms during national emergencies, but the Court found broad forgiveness went beyond this scope. |

| Congressional Action | Broad student loan forgiveness would likely require congressional legislation, which has not been passed as of October 2023. |

| Current Efforts | Biden's administration is exploring alternative paths, such as income-driven repayment (IDR) reforms and targeted forgiveness for specific groups. |

| IDR Account Adjustment | In April 2022, the Department of Education announced an IDR account adjustment to address past payment counting errors, providing millions with progress toward forgiveness. |

| Public Service Loan Forgiveness (PSLF) | Reforms to PSLF have been implemented, making it easier for eligible borrowers to qualify for forgiveness. |

| Political Opposition | Republicans and some Democrats oppose broad forgiveness, citing concerns about cost, fairness, and executive overreach. |

| Cost Estimate | Broad forgiveness (up to $20,000) was estimated to cost $400 billion over 30 years, according to the Congressional Budget Office. |

| Borrower Eligibility | If broad forgiveness were implemented, eligibility would likely be based on income thresholds (e.g., $125,000 for individuals, $250,000 for couples). |

| Loan Types Covered | Previous proposals included federal student loans held by the Department of Education, excluding private loans. |

| Current Status | As of October 2023, broad student loan forgiveness remains blocked, but targeted relief efforts continue. |

Explore related products

What You'll Learn

- Legal authority under HEROES Act for executive action on student loan forgiveness

- Potential economic impact of canceling student debt on inflation and growth

- Political implications and public opinion on Biden’s debt forgiveness plan

- Challenges from lawsuits and opposition to the forgiveness policy in court

- Long-term effects on higher education costs and borrowing behavior post-forgiveness

![]()

Legal authority under HEROES Act for executive action on student loan forgiveness

The Higher Education Relief Opportunities for Students (HEROES) Act of 2003 grants the Secretary of Education broad authority to modify student loan terms during national emergencies. This law, originally designed to assist military personnel, has become a focal point in the debate over executive action on student loan forgiveness. By invoking the HEROES Act, the Biden administration could potentially waive interest, pause payments, or even discharge certain federal student loans without congressional approval. However, the extent of this authority remains a subject of legal and political contention.

To understand the HEROES Act’s applicability, consider its core purpose: to provide relief during times of crisis. The COVID-19 pandemic, declared a national emergency in March 2020, falls squarely within this framework. Since then, the Department of Education has used the Act to pause federal student loan payments and suspend interest accrual, benefiting millions of borrowers. These actions demonstrate the Act’s flexibility but also raise questions about whether forgiveness—a more permanent measure—is within its scope. Critics argue that forgiveness goes beyond the Act’s intent, while proponents contend it aligns with its spirit of providing meaningful relief.

A key legal challenge lies in interpreting the Act’s language. Section 2(a)(1) allows the Secretary to “waive or modify any statutory or regulatory provision applicable to the student financial assistance programs” to ensure affected borrowers are not worse off financially. While this provision is expansive, it is not unlimited. For example, forgiving loans for all borrowers, regardless of pandemic impact, could be seen as overreach. A more targeted approach—such as forgiving loans for low-income borrowers or those in public service—might align better with the Act’s emergency relief framework.

Practical implementation also requires careful consideration. If the Biden administration were to pursue forgiveness under the HEROES Act, it would need to define eligibility criteria, determine the amount of forgiveness, and address potential tax implications for borrowers. For instance, forgiven debt is typically treated as taxable income, though the American Rescue Plan of 2021 excluded student loan forgiveness from taxation through 2025. Clear communication and coordination with the IRS would be essential to avoid unintended financial burdens on borrowers.

In conclusion, the HEROES Act provides a plausible legal pathway for executive action on student loan forgiveness, but its application is not without constraints. A successful strategy would require a nuanced interpretation of the Act’s authority, targeted implementation, and careful attention to potential legal and administrative challenges. While the Act offers a tool for relief, its effectiveness ultimately depends on how it is wielded.

Public Service Loan Forgiveness: Does It Apply to Private Student Loans?

You may want to see also

Explore related products

![]()

Potential economic impact of canceling student debt on inflation and growth

The cancellation of student debt has been a contentious issue, with proponents arguing it could stimulate economic growth and opponents warning of inflationary pressures. To understand its potential impact, consider the scale: forgiving $10,000 per borrower could cost approximately $377 billion, while $50,000 per borrower could reach $1.4 trillion. Such a massive injection of funds into the economy would not go unnoticed, but its effects depend on how borrowers respond. If debt cancellation frees up disposable income, consumers might increase spending, boosting sectors like retail, housing, and services. However, this increased demand could also drive prices higher, particularly in an economy already grappling with inflation.

Analyzing the mechanics, debt cancellation could act as a form of fiscal stimulus, similar to tax cuts or direct payments. For instance, a borrower with $300 in monthly loan payments might redirect that money toward goods, services, or savings. If millions of borrowers behave similarly, aggregate demand could rise, potentially accelerating GDP growth. However, this scenario assumes borrowers spend rather than save or pay down other debts. Historical data suggests younger borrowers are more likely to spend, while older borrowers may prioritize savings or debt reduction. Policymakers must weigh these behavioral differences when predicting macroeconomic outcomes.

A comparative perspective reveals mixed lessons from similar policies. Australia’s Higher Education Loan Program (HELP), which does not require repayment until income thresholds are met, has not caused significant inflation but has supported education access. Conversely, broad stimulus measures during the COVID-19 pandemic contributed to inflationary spikes in the U.S. and elsewhere. The key difference lies in targeting: student debt cancellation benefits a specific demographic, whereas pandemic stimulus was universal. Targeted relief might avoid overheating the economy if borrowers’ spending is modest and gradual.

To mitigate inflationary risks, policymakers could implement safeguards. One approach is phasing in debt cancellation over several years, spreading out the economic impact. Another is pairing cancellation with measures to increase the supply of goods and services, such as investments in affordable housing or education infrastructure. Additionally, the Federal Reserve could adjust monetary policy to counteract inflationary pressures, though this risks dampening growth. Striking the right balance requires careful calibration, not just of the policy itself but of complementary measures.

Ultimately, the economic impact of canceling student debt hinges on its design and context. A well-structured plan could spur growth by freeing up income for productive uses, such as entrepreneurship or homeownership. However, without safeguards, it risks exacerbating inflation, particularly in sectors where demand outstrips supply. Policymakers must navigate these trade-offs, recognizing that while debt cancellation offers a powerful tool for economic stimulus, its success depends on precision and prudence.

Qualifying for Student Loan Forgiveness: Is It Really That Easy?

You may want to see also

Explore related products

![]()

Political implications and public opinion on Biden’s debt forgiveness plan

President Biden's student loan forgiveness plan has become a lightning rod in American politics, polarizing public opinion and reshaping electoral strategies. At its core, the plan aims to cancel up to $20,000 in federal student debt for eligible borrowers, a move framed as both economic relief and social justice. However, its political implications are far-reaching, influencing voter perceptions, party dynamics, and the balance of power in Congress. For Democrats, the plan is a bold stroke to energize younger and progressive voters, who often feel burdened by educational debt. Yet, it risks alienating moderate and independent voters who view it as fiscally irresponsible or unfair to those who paid their loans in full. Republicans, meanwhile, have seized on the issue as an example of government overreach, using it to rally their base and challenge the plan in court, framing it as an unconstitutional abuse of executive power.

Public opinion on the plan is deeply divided, reflecting broader societal fault lines. Polls show that while a majority of Democrats support debt forgiveness, Republicans overwhelmingly oppose it, with independents split. Age is a critical factor: younger Americans, disproportionately affected by student debt, tend to favor the plan, while older generations, many of whom paid off their loans without assistance, are more skeptical. Racial disparities also play a role, as Black and Latino borrowers, who carry higher average debt burdens, are more likely to support forgiveness. However, the plan’s popularity wanes when framed as a taxpayer-funded bailout, highlighting the challenge of messaging in a politically charged environment. Practical concerns, such as the plan’s impact on inflation or its long-term effects on higher education costs, further complicate public perception.

The legal battles surrounding the plan underscore its political volatility. After the Supreme Court struck down Biden’s initial forgiveness program in 2023, the administration pivoted to narrower relief efforts, such as income-driven repayment plans and targeted cancellations for specific groups. These adjustments reflect a strategic effort to salvage the policy’s goals while navigating legal and political constraints. However, each revision reignites debates over executive authority and the role of government in addressing systemic issues like student debt. For Biden, the stakes are high: failure to deliver on his promise could disillusion key constituencies, while success could cement his legacy as a champion of economic equity.

To navigate this complex landscape, policymakers must balance idealism with pragmatism. Advocates for forgiveness argue that it would stimulate the economy by freeing up disposable income for millions of Americans, while critics warn of moral hazard and long-term fiscal risks. A middle-ground approach, such as means-tested forgiveness or expanded repayment options, could mitigate these concerns while providing tangible relief. For voters, understanding the nuances of the plan—its scope, eligibility criteria, and funding mechanisms—is essential to forming an informed opinion. As the debate continues, one thing is clear: Biden’s debt forgiveness plan is not just a policy initiative but a political gamble with far-reaching consequences for his presidency and the nation’s future.

Student Loan Forgiveness Bill Blocked: What Does This Mean?

You may want to see also

Explore related products

$14.95 $14.95

![]()

Challenges from lawsuits and opposition to the forgiveness policy in court

The Biden administration's student loan forgiveness plan faced immediate legal challenges, with multiple lawsuits filed shortly after its announcement. These lawsuits argue that the administration overstepped its authority under the Higher Education Act and violated the Administrative Procedure Act by bypassing Congress. The legal battles have created uncertainty for millions of borrowers awaiting relief, as courts weigh the constitutional and statutory limits of executive power.

One of the most significant challenges came from Republican-led states, which claimed the forgiveness plan infringed on their sovereign immunity and caused financial harm to state entities managing student loans. In *Nebraska v. Biden*, a federal judge blocked the program, ruling that the states had standing to sue and that the administration lacked the authority to implement such broad forgiveness. This decision highlighted the tension between federal and state powers, as well as the political polarization surrounding the issue.

Another critical lawsuit, *Biden v. Missouri*, reached the Supreme Court, where the administration defended its use of the HEROES Act as legal justification for the forgiveness. The Court’s conservative majority scrutinized the plan’s scope, questioning whether it exceeded the act’s intent to provide targeted relief during national emergencies. The outcome of this case will likely set a precedent for the limits of executive action in education policy, with broader implications for administrative law.

Borrowers caught in this legal limbo face practical challenges, such as delayed payments and confusion over loan servicers’ instructions. To navigate this uncertainty, borrowers should continue making payments if financially feasible, monitor updates from the Department of Education, and explore alternative relief options like income-driven repayment plans. While the lawsuits proceed, staying informed and proactive is essential to managing student debt effectively.

In conclusion, the legal opposition to Biden’s forgiveness policy underscores the complexities of implementing large-scale debt relief without congressional approval. The court rulings not only determine the fate of the program but also shape the future of executive authority in education. For borrowers, the ongoing battles serve as a reminder of the precarious nature of policy changes and the importance of staying prepared for shifting landscapes.

Can Student Loan Forgiveness Lead to a Refund? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Long-term effects on higher education costs and borrowing behavior post-forgiveness

Student loan forgiveness, if implemented, could inadvertently reshape the financial landscape of higher education, potentially driving up costs in the long term. Colleges and universities, sensing reduced financial burden on students, might increase tuition fees, knowing that federal intervention could soften the impact. This phenomenon, often referred to as the "moral hazard" of forgiveness, could perpetuate a cycle where institutions raise prices, and students borrow more, expecting future relief. For instance, if a private university currently charges $50,000 annually, it might incrementally hike fees to $60,000 or more, banking on the assumption that students will borrow without restraint, given the precedent of forgiveness.

To mitigate this risk, policymakers must pair forgiveness with structural reforms that cap tuition increases. States could reintroduce funding models that tie public university budgets to inflation or regional income levels, ensuring affordability. Simultaneously, federal oversight could mandate transparency in private institution pricing, requiring them to justify tuition hikes beyond a certain threshold. Without such safeguards, forgiveness could become a subsidy for institutions rather than a relief for borrowers, exacerbating the very problem it aims to solve.

Borrowing behavior post-forgiveness would likely reflect a mix of caution and complacency. On one hand, students might become more discerning about loan amounts, opting for federal loans with forgiveness potential over private ones. On the other, the memory of forgiveness could foster a "borrow now, worry later" mindset, particularly among younger demographics. A 2023 survey by the Pew Research Center found that 43% of Gen Z students believed future forgiveness was likely, influencing their willingness to accrue debt. This duality underscores the need for financial literacy programs that educate students on the long-term implications of borrowing, even in an era of potential forgiveness.

Finally, the psychological impact of forgiveness on borrowing cannot be overlooked. Forgiving debt sends a powerful signal about the value of education, but it also risks normalizing high debt levels as an inevitable part of the college experience. To counter this, institutions should incentivize cost-effective pathways, such as dual enrollment programs or competency-based degrees, which reduce reliance on traditional four-year models. By fostering a culture of affordability alongside forgiveness, the higher education system can avoid the pitfalls of unchecked borrowing while ensuring access to quality education.

Stop Annoying Student Loan Forgiveness Calls: Effective Strategies to Regain Peace

You may want to see also

Frequently asked questions

President Biden’s authority to forgive student loan debt through executive action is a matter of legal debate. While the Higher Education Act grants the Secretary of Education the power to modify or waive certain federal student loans, critics argue that large-scale debt forgiveness requires congressional approval. The Biden administration has cited legal justification, but the issue remains contested and has faced legal challenges.

The amount of student loan debt Biden can forgive and the eligibility criteria depend on the specific policy or executive action. Previous proposals have suggested forgiving up to $10,000 or $50,000 per borrower, often targeting those with federal student loans and income below a certain threshold. However, no broad forgiveness plan has been finalized or implemented as of now.

Forgiving student loan debt could stimulate the economy by freeing up disposable income for borrowers, potentially boosting spending and savings. However, critics argue it could increase the national debt and inflation. The impact would depend on the scale of forgiveness and how it is structured, with targeted relief likely having a more positive economic effect than broad, universal forgiveness.