Understanding the simple interest rate on a student loan is crucial for borrowers to manage their finances effectively. Simple interest is calculated as a percentage of the principal amount borrowed, without compounding, making it a straightforward way to determine the cost of borrowing. For student loans, this rate directly impacts the total amount to be repaid over the loan term. Knowing the simple interest rate helps borrowers estimate monthly payments, plan for repayment strategies, and compare loan options to make informed financial decisions. It is often influenced by factors such as credit history, loan term, and market conditions, making it essential to review the terms carefully before committing to a loan.

| Characteristics | Values |

|---|---|

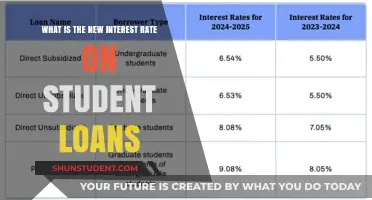

| Type of Interest | Simple Interest |

| Current Rate (Undergraduate) | 5.5% (for loans first disbursed on or after July 1, 2023) |

| Current Rate (Graduate) | 7.05% (for loans first disbursed on or after July 1, 2023) |

| Current Rate (PLUS Loans) | 8.05% (for loans first disbursed on or after July 1, 2023) |

| Calculation Method | Principal × Rate × Time (in years) |

| Fixed vs. Variable | Fixed (rates are set annually and remain constant for the loan term) |

| Loan Types | Direct Subsidized, Direct Unsubsidized, Direct PLUS Loans |

| Repayment Period | Typically 10 years (standard plan), but varies based on repayment plan |

| Interest Capitalization | Occurs at the end of grace/deferment periods (not applicable to simple interest loans) |

| Source of Data | U.S. Department of Education (Federal Student Aid) |

| Last Updated | July 1, 2023 |

Explore related products

What You'll Learn

![]()

Understanding Simple Interest Calculation

Simple interest is a straightforward method of calculating the interest charged on a loan, including student loans. It is calculated based on the principal amount (the initial amount borrowed), the interest rate, and the time period of the loan. Understanding how simple interest works is crucial for borrowers, as it directly impacts the total amount to be repaid. Unlike compound interest, which calculates interest on both the principal and accumulated interest, simple interest is only applied to the original principal amount. This makes it easier to understand and predict the cost of borrowing.

To calculate simple interest on a student loan, you use the formula: Simple Interest = Principal × Rate × Time. Here, the principal is the amount borrowed, the rate is the annual interest rate (expressed as a decimal), and time is the duration of the loan in years. For example, if a student borrows $10,000 at a simple interest rate of 5% for 4 years, the calculation would be: Simple Interest = $10,000 × 0.05 × 4 = $2,000. This means the borrower would pay $2,000 in interest over the 4-year period, in addition to repaying the $10,000 principal.

When researching "what is the simple interest rate on the student loan," it’s important to note that interest rates can vary widely depending on the type of loan (federal or private), the borrower’s credit history, and market conditions. Federal student loans often have fixed interest rates set by the government, while private loans may offer variable rates that fluctuate over time. Knowing the exact interest rate is essential for using the simple interest formula accurately and planning repayment effectively.

Finally, while simple interest is easier to calculate than compound interest, it’s still important to be aware of how it accumulates over time. Even a seemingly low interest rate can result in significant interest payments over a long loan term. Borrowers should also check if their student loan requires interest payments while in school or during grace periods, as this can affect the total amount owed. By mastering the concept of simple interest calculation, students and their families can make informed decisions about borrowing and repayment, ensuring they manage their student loans wisely.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Factors Affecting Student Loan Interest Rates

The interest rate on a student loan is a critical factor that determines the overall cost of borrowing. Unlike complex interest calculations, simple interest on a student loan is calculated solely on the principal amount, making it easier to understand. However, several factors influence the simple interest rate applied to student loans, and understanding these can help borrowers make informed decisions. One of the primary factors is the type of loan—federal or private. Federal student loans typically offer fixed interest rates set by the government, which are often lower than private loans. Private loans, on the other hand, have rates determined by lenders based on market conditions and the borrower’s creditworthiness.

Another significant factor affecting student loan interest rates is the borrower’s credit history and credit score. For private loans, lenders assess the borrower’s creditworthiness to determine the risk of lending. A higher credit score generally results in a lower interest rate, as it indicates a lower risk of default. Conversely, borrowers with poor or limited credit history may face higher interest rates. Federal student loans, however, do not typically require a credit check, making them more accessible but with standardized rates based on federal regulations rather than individual credit profiles.

The economic environment also plays a crucial role in shaping student loan interest rates. For federal loans, rates are tied to the 10-year Treasury note auction and are adjusted annually based on market conditions. During periods of economic growth, interest rates may rise, while they may decrease during economic downturns. Private loan rates are similarly influenced by broader economic trends, including inflation and monetary policy decisions by central banks. Borrowers should monitor these macroeconomic factors to anticipate potential changes in their loan rates.

The repayment term of the loan is another factor that impacts the interest rate. Shorter repayment terms often come with lower interest rates because lenders assume less risk over a shorter period. Longer repayment terms, while providing lower monthly payments, typically result in higher total interest costs due to the extended borrowing period. Borrowers should carefully consider their financial situation and choose a repayment term that balances affordability with minimizing interest expenses.

Lastly, the type of interest rate—fixed or variable—affects the overall cost of the loan. Fixed interest rates remain constant throughout the life of the loan, providing predictability in monthly payments. Variable rates, however, fluctuate based on market conditions, which can lead to changes in monthly payments and total interest costs. While variable rates may start lower than fixed rates, they carry the risk of increasing over time, making them less stable for long-term planning. Understanding these factors allows borrowers to navigate the complexities of student loan interest rates and choose the most favorable terms for their financial circumstances.

Understanding the Student Loan Interest Phaseout: What You Need to Know

You may want to see also

Explore related products

![]()

Fixed vs. Variable Interest Rates

When considering student loans, one of the most critical decisions borrowers face is choosing between fixed and variable interest rates. This choice significantly impacts the total cost of the loan and the predictability of monthly payments. A simple interest rate on a student loan is calculated as a percentage of the principal amount, but whether that rate remains constant or fluctuates over time depends on the type of interest rate selected. Understanding the differences between fixed and variable rates is essential for making an informed financial decision.

Fixed interest rates remain constant throughout the life of the loan. This means the interest rate you agree to at the time of borrowing will not change, regardless of market conditions. For example, if you secure a student loan with a fixed interest rate of 5%, that rate will stay at 5% until the loan is fully repaid. The primary advantage of a fixed rate is predictability. Borrowers can plan their budgets more effectively since their monthly payments remain the same. This stability is particularly beneficial in a rising interest rate environment, as it protects borrowers from higher costs. However, fixed rates are often initially higher than variable rates, which can make them more expensive upfront.

On the other hand, variable interest rates can fluctuate over time, typically in response to changes in a benchmark rate, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. For instance, if you take out a student loan with a variable rate of 3% and the benchmark rate increases by 1%, your interest rate will rise to 4%. Variable rates are often lower than fixed rates initially, which can make them appealing to borrowers seeking lower upfront costs. However, this comes with the risk of increased payments if interest rates rise. Borrowers with variable rates must be prepared for the possibility of higher monthly payments, which can strain their finances if not managed carefully.

Choosing between fixed and variable rates depends on several factors, including your financial stability, risk tolerance, and expectations about future interest rate trends. If you prefer consistency and want to avoid the uncertainty of fluctuating payments, a fixed rate may be the better option. Conversely, if you are comfortable with potential changes in your monthly payments and believe interest rates will remain stable or decrease, a variable rate could save you money in the long run. It’s also important to consider the loan term; shorter repayment periods may make variable rates less risky, while longer terms increase exposure to rate changes.

In summary, the decision between fixed and variable interest rates on a student loan hinges on your financial goals and risk tolerance. Fixed rates offer stability and predictability, making them ideal for borrowers who prioritize consistent payments. Variable rates, while riskier, can provide initial savings and may be advantageous if interest rates remain low. Before committing to a loan, carefully evaluate your financial situation, research current market trends, and consider consulting a financial advisor to determine the best option for your needs. Understanding these differences ensures you make a choice that aligns with your long-term financial health.

Understanding the Current Student Loan Interest Rate Trends

You may want to see also

Explore related products

![]()

Impact of Repayment Terms on Interest

The simple interest rate on a student loan is a fixed percentage applied to the principal amount borrowed, determining the cost of borrowing over time. Unlike compound interest, simple interest does not accrue on previously accumulated interest, making it easier to calculate. However, the repayment terms of a student loan significantly influence the total interest paid, even with a simple interest structure. Longer repayment terms, for instance, result in more interest accruing over time, increasing the overall cost of the loan. Conversely, shorter repayment terms minimize interest costs but require higher monthly payments. Understanding this relationship is crucial for borrowers to make informed decisions about their student loan repayment strategies.

One of the most direct impacts of repayment terms on interest is the total duration of the loan. For example, a 10-year repayment term will accrue more interest than a 5-year term, even if the interest rate remains constant. This is because interest is calculated based on the outstanding principal balance over time. Borrowers who opt for extended repayment plans, such as 20 or 25 years, may find themselves paying significantly more in interest over the life of the loan compared to those who choose standard 10-year plans. While longer terms reduce monthly payments, they ultimately increase the financial burden due to the additional interest accrued.

Another critical factor is the frequency and amount of payments. Making extra payments or paying more than the minimum required can reduce the principal balance faster, thereby decreasing the total interest paid. For instance, bi-weekly payments instead of monthly payments can shorten the loan term and save on interest. Similarly, lump-sum payments toward the principal can have a substantial impact on reducing interest costs. Borrowers should explore prepayment options and ensure their loans do not include prepayment penalties to maximize these benefits.

Repayment plans with graduated or income-driven structures also affect interest accumulation. Graduated repayment plans start with lower payments that increase over time, often leading to more interest accrual in the early years. Income-driven plans tie monthly payments to the borrower’s income, which can result in lower payments but extended repayment periods, increasing total interest paid. Borrowers must weigh the immediate financial relief of these plans against the long-term cost of additional interest.

Lastly, the timing of payments plays a role in interest calculations. Simple interest is typically calculated daily based on the outstanding principal. Late payments or missed payments can extend the loan term, allowing more interest to accrue. Staying current on payments and understanding the amortization schedule can help borrowers minimize interest costs. Additionally, refinancing to a lower interest rate or shorter term can further reduce the impact of repayment terms on interest, provided the borrower qualifies for better terms.

In summary, the repayment terms of a student loan have a profound impact on the total interest paid, even with a simple interest rate. Borrowers should carefully consider the duration of the loan, payment frequency, repayment plan type, and payment timing to manage interest costs effectively. By strategically choosing and managing repayment terms, borrowers can significantly reduce the financial burden of their student loans.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

How to Lower Your Interest Rate

Lowering the interest rate on your student loan can significantly reduce the total amount you repay over time. While federal student loans often have fixed interest rates set by Congress, there are strategies to secure a lower rate, especially with private loans or through refinancing. Here’s how you can approach this effectively.

- Refinance Your Student Loans: One of the most direct ways to lower your interest rate is by refinancing your student loans. Refinancing involves taking out a new loan with a private lender to pay off your existing loans. If your credit score has improved since you first took out the loan, or if market interest rates have dropped, you may qualify for a lower rate. Shop around with multiple lenders to compare offers, as rates and terms can vary widely. Keep in mind that refinancing federal loans into private loans means losing access to federal benefits like income-driven repayment plans and loan forgiveness programs.

- Improve Your Credit Score: Lenders use your credit score to assess your risk as a borrower. A higher credit score often translates to a lower interest rate. To boost your score, focus on paying bills on time, reducing credit card balances, and avoiding new debt. If you’re refinancing, consider adding a creditworthy cosigner to your application. A cosigner with a strong credit history can help you secure a lower rate, though they’ll share responsibility for the loan.

- Take Advantage of Autopay Discounts: Many lenders offer a small interest rate reduction—typically 0.25%—if you enroll in automatic payments. This discount may seem minor, but it can save you hundreds or even thousands of dollars over the life of the loan. Autopay also ensures you never miss a payment, which protects your credit score and avoids late fees.

- Explore Loyalty or Rate Reduction Programs: Some lenders provide loyalty discounts or rate reductions after a certain number of on-time payments. For example, you might receive a 0.25% rate reduction after making 24 or 36 consecutive on-time payments. Review your loan agreement or contact your lender to see if such programs are available. Additionally, if you have multiple loans with the same lender, they may offer a rate reduction as an incentive to consolidate your business with them.

- Consider Federal Loan Repayment Options: While federal student loans typically have fixed rates, certain repayment plans can lower your monthly payments, indirectly easing the burden of interest. For instance, income-driven repayment plans cap your monthly payments at a percentage of your discretionary income and may offer loan forgiveness after 20–25 years. Though these plans don’t directly lower your interest rate, they can make your payments more manageable and reduce the overall cost if you qualify for forgiveness.

By combining these strategies, you can take proactive steps to lower your student loan interest rate and save money in the long run. Always weigh the pros and cons of each option, especially when considering refinancing federal loans, to ensure you’re making the best decision for your financial situation.

Understanding the Real Interest Rate on Student Loans: What You Need to Know

You may want to see also

Frequently asked questions

The simple interest rate on a student loan is the fixed percentage charged annually on the principal amount borrowed, calculated without compounding.

The simple interest rate is calculated using the formula: Simple Interest = (Principal × Rate × Time), where the rate is expressed as a decimal.

No, the simple interest rate on a student loan remains constant unless specified otherwise in the loan agreement.