Private student loans are a common financing option for students seeking to cover educational expenses beyond what federal loans, grants, or scholarships provide. One of the most critical aspects of these loans is the interest rate, which significantly impacts the overall cost of borrowing. Unlike federal student loans, which have fixed interest rates set by the government, private student loan interest rates vary widely based on factors such as the borrower’s credit history, income, and cosigner involvement. Typically, private student loan interest rates can be either fixed or variable, with fixed rates remaining constant throughout the loan term and variable rates fluctuating based on market conditions. Borrowers with strong credit profiles or reliable cosigners often secure lower interest rates, while those with limited credit history may face higher rates, increasing the total repayment amount. Understanding these interest rate dynamics is essential for students to make informed decisions and manage their loan obligations effectively.

Explore related products

What You'll Learn

- Interest Rate Types: Fixed vs. variable rates and their impact on repayment

- Repayment Terms: Standard, graduated, or income-driven plans for private loans

- Fees and Penalties: Origination fees, late fees, and prepayment penalties

- Credit Requirements: How credit scores affect eligibility and interest rates

- Cosigner Benefits: Lower rates and improved approval chances with a cosigner

![]()

Interest Rate Types: Fixed vs. variable rates and their impact on repayment

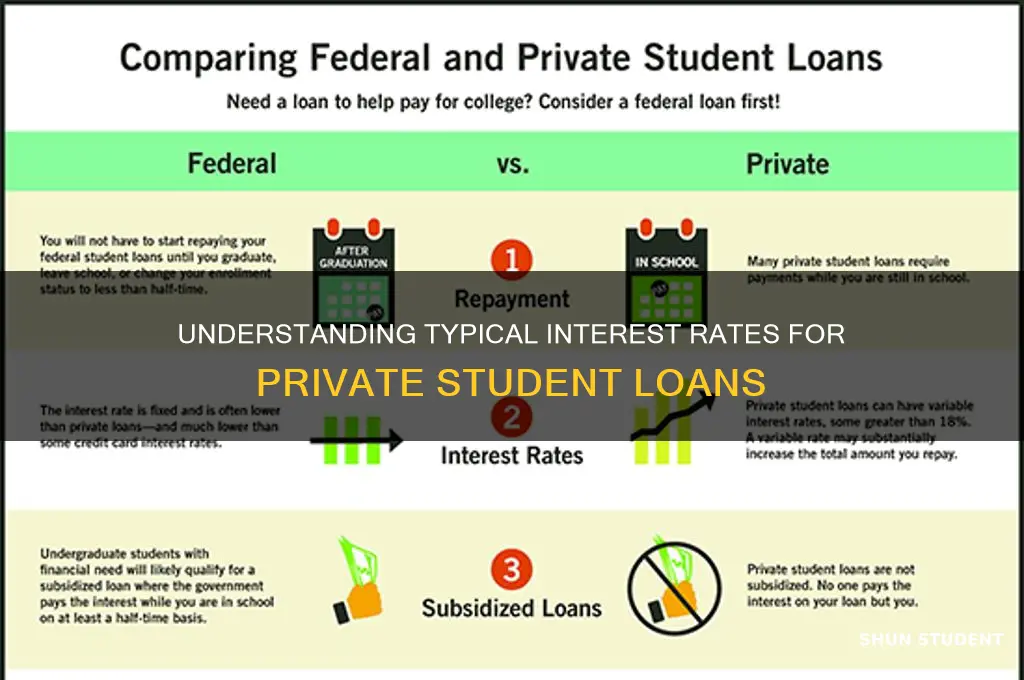

When considering private student loans, understanding the difference between fixed and variable interest rates is crucial, as it directly impacts your repayment plan and overall cost. Fixed interest rates remain constant throughout the life of the loan, meaning the rate you agree to at the time of borrowing will not change, regardless of market fluctuations. This predictability is advantageous for borrowers who prefer stable, unchanging monthly payments. For instance, if you take out a private student loan with a fixed rate of 6%, that rate will stay the same until the loan is fully repaid. This makes budgeting easier, as you know exactly how much you’ll owe each month and over the loan’s term.

On the other hand, variable interest rates fluctuate based on market conditions, typically tied to an index like the London Interbank Offered Rate (LIBOR) or the Prime Rate. Initially, variable rates may start lower than fixed rates, making them an attractive option for borrowers. However, this rate can increase over time if the underlying index rises, potentially leading to higher monthly payments and a greater total repayment amount. For example, a variable rate starting at 4% could climb to 7% or higher if market rates increase, significantly impacting your repayment strategy.

The choice between fixed and variable rates depends on your financial situation, risk tolerance, and market outlook. Fixed rates are ideal for borrowers who prioritize consistency and want to avoid surprises in their repayment plan. They are particularly beneficial in low-interest-rate environments, as locking in a low fixed rate can save money over the long term. Conversely, variable rates may appeal to borrowers who expect to pay off their loans quickly or believe interest rates will remain stable or decline during their repayment period.

The impact of these rate types on repayment is substantial. With a fixed rate, your total interest paid is predictable, allowing you to plan for the future. Variable rates, however, introduce uncertainty, as changes in the market can alter your monthly payments and the total cost of the loan. For instance, a borrower with a $30,000 loan at a fixed 5% rate will pay less in interest over 10 years than someone whose variable rate starts at 4% but increases to 7% midway through the repayment term.

In summary, when evaluating private student loan options, carefully consider whether a fixed or variable interest rate aligns with your financial goals and risk tolerance. Fixed rates offer stability and predictability, making them a safer choice for long-term planning. Variable rates, while initially lower, carry the risk of increasing costs, which could strain your budget if market conditions change. Understanding these differences ensures you make an informed decision that minimizes the financial burden of student loan repayment.

Understanding Typical Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Terms: Standard, graduated, or income-driven plans for private loans

When considering private student loans, understanding the repayment terms is crucial, as these terms significantly impact the overall cost and management of your debt. Private lenders typically offer several repayment plans, each with distinct structures to accommodate different financial situations. The three most common repayment plans are standard, graduated, and income-driven, and they each come with their own set of advantages and considerations.

Standard Repayment Plan

The standard repayment plan is the most straightforward option. Under this plan, borrowers make fixed monthly payments over a set period, usually 10 years, though some lenders may offer shorter or longer terms. The primary benefit of this plan is that it minimizes the total interest paid over the life of the loan, as consistent payments reduce the principal balance more quickly. However, the fixed payments can be higher compared to other plans, which may be challenging for borrowers with limited income immediately after graduation. This plan is ideal for those who have a stable income and want to pay off their loans as quickly as possible.

Graduated Repayment Plan

A graduated repayment plan is designed to start with lower monthly payments that increase over time, typically every two years. This structure aligns with the assumption that borrowers’ incomes will grow as they advance in their careers. The initial lower payments can provide financial relief during the early years of repayment, but the increasing payments mean that borrowers will pay more interest over the life of the loan compared to a standard plan. This option is suitable for borrowers who expect their income to rise steadily but need flexibility in the short term.

Income-Driven Repayment Plan

Income-driven repayment plans are less common with private lenders but are sometimes offered as an option. These plans base monthly payments on a percentage of the borrower’s discretionary income, often recalculated annually. This can result in lower monthly payments for those with lower incomes, making it easier to manage debt. However, because payments may not cover the accruing interest, the total amount repaid can be significantly higher over time. Income-driven plans are best for borrowers with irregular or low incomes who need flexibility and affordability in their repayment schedule.

Choosing the Right Plan

Selecting the appropriate repayment plan depends on your financial situation, career outlook, and long-term goals. Standard plans are ideal for those seeking to minimize interest and pay off debt quickly, while graduated plans cater to borrowers expecting income growth. Income-driven plans offer the most flexibility but may result in higher overall costs. It’s essential to evaluate your current and projected financial circumstances carefully before committing to a repayment plan. Additionally, some private lenders may allow borrowers to switch plans if their financial situation changes, though this is not guaranteed and should be confirmed with the lender.

Impact on Interest Rates

While repayment terms themselves do not directly determine the interest rate on a private student loan, the choice of plan can affect the total interest paid. For instance, longer repayment periods or plans with lower initial payments often result in more interest accruing over time. Borrowers should consider both the interest rate and the repayment term when calculating the total cost of their loan. Typical interest rates for private student loans range from 3% to 12% or more, depending on creditworthiness, loan type, and market conditions. Understanding how repayment terms interact with these rates is key to making an informed decision.

Understanding Student Loan Consolidation Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

$6.99

![]()

Fees and Penalties: Origination fees, late fees, and prepayment penalties

When considering private student loans, it's essential to understand the various fees and penalties that can significantly impact the overall cost of borrowing. One common fee is the origination fee, which is charged by some lenders to cover the administrative costs of processing the loan. This fee is typically a percentage of the loan amount, often ranging from 1% to 6%, and is usually deducted from the loan disbursement. For example, if you borrow $20,000 with a 5% origination fee, you’ll receive $19,000, but you’ll still be responsible for repaying the full $20,000 plus interest. Not all private lenders charge origination fees, so it’s crucial to compare options to avoid unnecessary costs.

Another critical aspect to consider is late fees, which are imposed when a borrower fails to make a payment by the due date. Late fees can vary widely among lenders but typically range from $25 to $50 per missed payment. Over time, these fees can add up, increasing the total cost of the loan. Additionally, late payments can negatively impact your credit score, making it harder to secure favorable terms on future loans. Setting up automatic payments or reminders can help you avoid late fees and maintain a positive credit history.

Prepayment penalties are another factor to watch out for, though they are less common today than in the past. A prepayment penalty is a fee charged if you pay off your loan ahead of schedule, either in part or in full. Lenders impose these penalties to recoup the interest they would have earned had the loan term continued as planned. While many modern private student loans do not include prepayment penalties, it’s essential to verify this before signing the loan agreement. Avoiding loans with prepayment penalties gives you the flexibility to pay off your debt faster without incurring extra costs.

It’s also important to note that these fees and penalties can vary significantly between lenders, making it crucial to read the fine print of any loan agreement. Some lenders may waive origination fees or offer incentives for on-time payments, while others may have stricter policies regarding late fees. Understanding these details upfront can help you choose a loan that aligns with your financial situation and repayment strategy.

Lastly, while the interest rate is a primary concern when evaluating private student loans, the fees and penalties discussed here can also have a substantial impact on the total cost of borrowing. Origination fees reduce the amount of money you actually receive, late fees can accumulate over time, and prepayment penalties may discourage you from paying off your loan early. By carefully reviewing these aspects and comparing multiple lenders, you can make an informed decision that minimizes unnecessary expenses and supports your long-term financial goals.

Diverse Passions: Exploring the Term for Students with Varied Interests

You may want to see also

Explore related products

![]()

Credit Requirements: How credit scores affect eligibility and interest rates

When considering private student loans, understanding how credit scores impact eligibility and interest rates is crucial. Private lenders use credit scores as a primary factor to assess a borrower’s financial responsibility and risk. A higher credit score generally indicates a history of reliable financial behavior, making lenders more confident in the borrower’s ability to repay the loan. Conversely, a lower credit score may signal higher risk, potentially leading to loan denial or less favorable terms. Most private student loan lenders require a minimum credit score, typically ranging from 600 to 670, though this can vary. Borrowers with scores above 700 are more likely to qualify for lower interest rates and better loan terms.

Credit scores not only determine eligibility but also directly influence the interest rates offered on private student loans. Lenders often use a tiered pricing model, where higher credit scores correspond to lower interest rates. For example, a borrower with an excellent credit score (800 or above) might secure an interest rate of 3% to 5%, while someone with a fair credit score (650–699) could face rates of 8% to 12% or higher. The difference in rates can significantly impact the total cost of the loan over its lifetime. Borrowers with poor credit (below 650) may struggle to qualify without a cosigner and, if approved, could face double-digit interest rates.

For students with limited or no credit history, qualifying for a private student loan can be challenging. Lenders often view lack of credit history as risky because there is no evidence of financial behavior. In such cases, having a cosigner with a strong credit profile can improve eligibility and secure lower interest rates. The cosigner’s credit score becomes a determining factor, as lenders will consider their financial stability alongside the primary borrower’s application. This arrangement reduces the lender’s risk and can open doors to more competitive loan terms.

It’s important for borrowers to check their credit scores before applying for a private student loan. Free credit reports are available annually from major credit bureaus, and many financial institutions offer credit monitoring tools. If a borrower’s credit score is lower than desired, steps can be taken to improve it, such as paying down existing debt, correcting errors on credit reports, and avoiding new credit inquiries. A higher credit score not only increases the likelihood of loan approval but also positions the borrower to negotiate better interest rates.

Lastly, borrowers should be aware that credit requirements can vary widely among private lenders. Some lenders specialize in working with borrowers who have fair or poor credit, though these loans often come with higher interest rates and fees. Shopping around and comparing offers from multiple lenders is essential to finding the best terms. Additionally, understanding the long-term financial implications of higher interest rates is critical, as even a slight difference in rates can result in thousands of dollars in additional costs over the life of the loan.

Understanding the Federal Student Loan Interest Paid Tax Form

You may want to see also

Explore related products

![]()

Cosigner Benefits: Lower rates and improved approval chances with a cosigner

When considering private student loans, one of the most significant factors borrowers face is the interest rate, which can vary widely depending on creditworthiness and other financial factors. Typical interest rates for private student loans range from 4% to 12% or higher, with variable rates often starting lower than fixed rates but carrying the risk of increasing over time. For borrowers with limited credit history or lower credit scores, securing a loan with favorable terms can be challenging. This is where a cosigner becomes invaluable, offering benefits such as lower interest rates and improved approval chances.

A cosigner, typically a parent, relative, or trusted individual with strong credit, agrees to share responsibility for the loan. Lenders view cosigners as a form of security, reducing their risk since they have another party to turn to if the primary borrower defaults. As a result, loans with cosigners often qualify for lower interest rates compared to those without. For example, a borrower with fair credit might face an interest rate of 8% to 10%, but with a cosigner, that rate could drop to 5% to 7%, saving thousands of dollars over the life of the loan. This reduction in interest rates not only makes monthly payments more manageable but also decreases the overall cost of borrowing.

In addition to lower rates, a cosigner significantly improves the chances of loan approval. Lenders assess both the borrower’s and cosigner’s credit histories, incomes, and debt-to-income ratios when evaluating the application. If the borrower has a thin credit file or a history of missed payments, a cosigner with a strong financial profile can tip the scales in their favor. This is particularly beneficial for students who are just starting to build credit or for international students who may not have a U.S. credit history. With a cosigner, lenders are more confident in the borrower’s ability to repay the loan, making approval more likely.

Another advantage of having a cosigner is the potential to access more competitive loan terms. Beyond interest rates, cosigners can help borrowers qualify for loans with longer repayment terms, lower fees, or additional benefits such as interest rate discounts for consistent on-time payments. These terms can provide greater flexibility and financial relief, especially for students pursuing degrees in fields with uncertain income prospects immediately after graduation. By leveraging a cosigner’s financial stability, borrowers can secure loans that align better with their long-term financial goals.

It’s important to note that while cosigning offers substantial benefits, it also comes with responsibilities for both parties. The cosigner is legally obligated to repay the loan if the borrower cannot, which could impact their credit score and financial health. Therefore, borrowers should prioritize timely payments to protect both their own and their cosigner’s credit. For cosigners, understanding the commitment and ensuring the borrower is capable of repayment is crucial. When managed responsibly, however, the benefits of lower interest rates and improved approval chances make cosigning a strategic option for securing private student loans with favorable terms.

Maximize Your Savings: Understanding the Student Loan Interest Tax Break

You may want to see also

Frequently asked questions

The typical interest rate for a private student loan ranges from 4% to 13%, depending on the lender, the borrower's creditworthiness, and whether the loan is fixed or variable.

Borrowers with excellent credit (typically a FICO score of 720 or higher) qualify for lower interest rates, while those with poor or limited credit history may face higher rates or need a cosigner.

Private student loans offer both fixed and variable interest rates. Fixed rates remain the same throughout the loan term, while variable rates may fluctuate based on market conditions.

Yes, adding a cosigner with strong credit can help you secure a lower interest rate, as it reduces the lender's risk.

Private student loan interest rates are often higher than federal student loan rates, which are typically fixed and set by the government. Federal loans also offer more flexible repayment options and borrower protections.