Unsubsidized student loans are a common financing option for students pursuing higher education, but understanding the interest associated with them is crucial for effective financial planning. Unlike subsidized loans, where the government covers the interest while the borrower is in school, unsubsidized loans accrue interest from the moment the funds are disbursed. This means borrowers are responsible for the accumulating interest during their studies, deferment periods, or grace periods, which can significantly increase the total repayment amount over time. The interest rate on unsubsidized loans is typically fixed and determined by federal guidelines, though it can vary depending on the year the loan was taken out. Failing to address this accruing interest can lead to capitalization, where unpaid interest is added to the loan principal, further escalating the debt burden. As such, borrowers must carefully consider the long-term implications of unsubsidized loans and explore strategies to manage or minimize the interest costs.

Explore related products

What You'll Learn

- Interest Accrual During School: Unsubsidized loans accrue interest while you're still in school

- Capitalization of Interest: Unpaid interest can capitalize, increasing your loan balance

- Repayment Interest Rates: Fixed or variable rates apply during repayment periods

- Deferment Interest Rules: Interest still accrues during deferment periods unless subsidized

- Forbearance Interest Costs: Interest continues to accrue during forbearance, increasing total debt

![]()

Interest Accrual During School: Unsubsidized loans accrue interest while you're still in school

Unsubsidized student loans are a common financing option for students, but they come with a critical feature that borrowers must understand: interest accrual during school. Unlike subsidized loans, where the government covers the interest while the borrower is enrolled at least half-time, unsubsidized loans begin accruing interest immediately after disbursement. This means that even while you’re focusing on your studies, the loan balance is growing due to accumulating interest. For example, if you borrow $5,000 with a 4.99% interest rate, interest will start adding to the principal balance from day one, increasing the total amount you’ll need to repay after graduation.

The interest accrual during school can have long-term financial implications if not managed properly. Since payments are not required while you’re in school, the unpaid interest is typically capitalized, meaning it is added to the principal balance. This results in compound interest, where you end up paying interest on the interest. For instance, if $500 in interest accrues during your academic year and you don’t pay it, that amount is added to your loan balance, and future interest calculations will include this higher principal. Over time, this can significantly increase the total cost of your loan.

To minimize the impact of interest accrual, borrowers have the option to make interest payments while still in school. Although not mandatory, paying the interest as it accrues prevents capitalization and keeps the loan balance from growing. For example, on a $10,000 unsubsidized loan at 4.99%, the monthly interest payment would be approximately $41.50. By paying this amount each month, you can avoid adding hundreds or even thousands of dollars to your loan balance by the time you graduate.

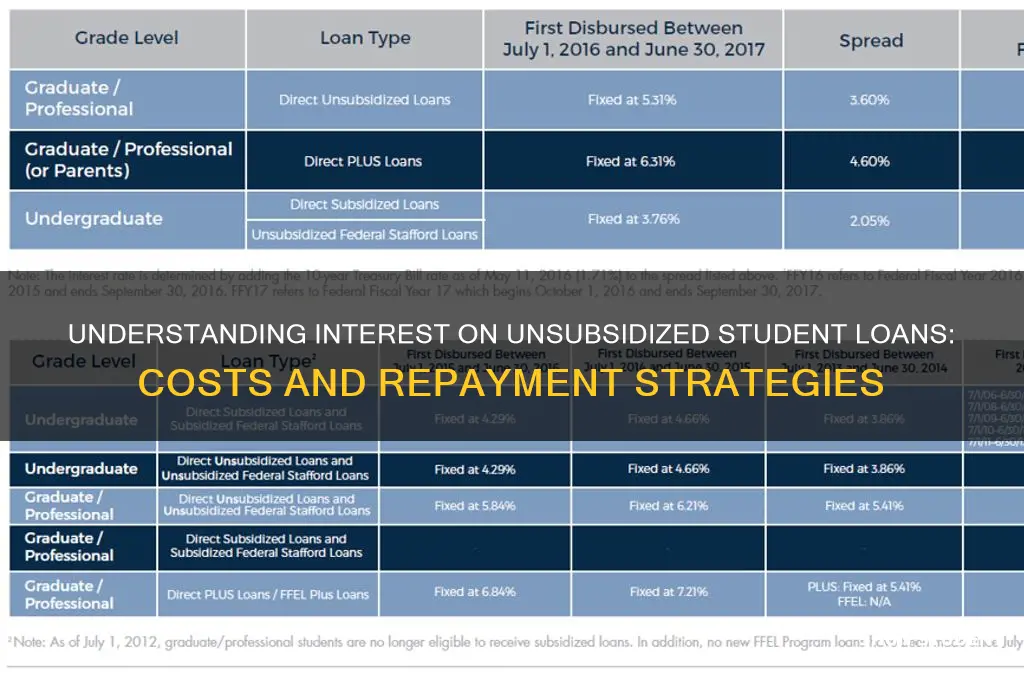

It’s important to understand how interest rates are determined for unsubsidized loans. These rates are set by the federal government and are typically fixed for the life of the loan. As of recent data, undergraduate unsubsidized loans have an interest rate of around 4.99%, while graduate loans are higher, at approximately 6.54%. Knowing your specific rate is crucial for estimating how much interest will accrue during your time in school and planning your repayment strategy accordingly.

Finally, borrowers should be proactive in tracking their loan balances and understanding the long-term consequences of interest accrual. Tools like the National Student Loan Data System (NSLDS) allow you to monitor your loans and see how much interest is accruing. Additionally, speaking with your school’s financial aid office can provide insights into managing your loans effectively. By staying informed and taking steps to manage interest during school, you can reduce the financial burden of unsubsidized loans and set yourself up for more manageable repayment after graduation.

Tax-Deductible Student Loan Interest: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Capitalization of Interest: Unpaid interest can capitalize, increasing your loan balance

Capitalization of interest is a critical concept for borrowers with unsubsidized student loans to understand, as it directly impacts the total amount they will owe over the life of the loan. Unlike subsidized loans, where the government covers the interest while the borrower is in school or during grace periods, unsubsidized loans accrue interest from the moment the funds are disbursed. If this interest is not paid as it accrues, it can capitalize, meaning it is added to the principal balance of the loan. This process significantly increases the total amount borrowed, as future interest is then calculated on this larger balance. For example, if a borrower has a $10,000 unsubsidized loan with 5% annual interest and does not pay the $500 in interest that accrues during the first year, that $500 is added to the principal, making the new balance $10,500. The borrower then pays interest on $10,500 instead of the original $10,000, leading to higher overall costs.

Capitalization of interest typically occurs at specific points during the life of an unsubsidized student loan. The first instance is at the end of the grace period, which is usually six months after graduation, leaving school, or dropping below half-time enrollment. During this grace period, interest continues to accrue, and if it remains unpaid, it capitalizes when the repayment period begins. Another common time for capitalization is when a borrower leaves a deferment or forbearance period, during which interest may have accrued without payment. Additionally, for certain income-driven repayment plans, capitalization can occur annually if the borrower’s monthly payment is not sufficient to cover the accruing interest. Understanding these triggers is essential for borrowers to manage their loans effectively and minimize the impact of capitalization.

To avoid or minimize the capitalization of interest, borrowers have several strategies at their disposal. The most straightforward approach is to pay the accruing interest while in school, during grace periods, or during deferment or forbearance. Even small payments can prevent the balance from growing. For example, paying $25 per month on a $10,000 loan with 5% interest can save hundreds of dollars in capitalized interest over time. Another strategy is to make interest payments while on an income-driven repayment plan to ensure that the balance does not increase. Borrowers can also consider making lump-sum payments toward the interest before capitalization occurs, such as before the end of a grace period or deferment. Proactive management of interest can significantly reduce the long-term cost of the loan.

It’s important for borrowers to be aware of how capitalization affects their loan repayment options and overall financial health. When interest capitalizes, it not only increases the principal balance but also extends the time it takes to pay off the loan, as more interest accrues on the higher balance. This can make monthly payments higher under standard repayment plans or increase the total amount paid over the life of the loan. For borrowers on income-driven plans, capitalization can lead to a situation where the monthly payments do not cover the accruing interest, causing the balance to grow even while making payments. This phenomenon, known as "negative amortization," can be particularly problematic for borrowers with limited incomes.

Finally, borrowers should carefully review their loan agreements and communicate with their loan servicers to fully understand when and how interest capitalization will occur. Loan servicers are required to notify borrowers before capitalization happens, providing an opportunity to make payments and avoid the increase in the loan balance. Additionally, borrowers can explore options such as loan consolidation, which may reset the capitalization process but could also affect interest rates and repayment terms. By staying informed and taking proactive steps, borrowers can better manage the impact of capitalized interest on their unsubsidized student loans and work toward more manageable repayment outcomes.

Understanding Tax Reform's Impact on Student Loan Interest Deductions

You may want to see also

Explore related products

![]()

Repayment Interest Rates: Fixed or variable rates apply during repayment periods

When it comes to unsubsidized student loans, understanding the repayment interest rates is crucial for borrowers. Repayment interest rates can be either fixed or variable, and this distinction significantly impacts the total cost of the loan over time. Fixed interest rates remain constant throughout the life of the loan, providing predictability in monthly payments. For instance, if an unsubsidized federal student loan has a fixed rate of 5.5%, this rate will not change, regardless of fluctuations in the broader economic environment. This stability makes budgeting easier for borrowers, as they know exactly how much interest will accrue each month.

On the other hand, variable interest rates on unsubsidized student loans can fluctuate based on market conditions. These rates are typically tied to a benchmark index, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. When the benchmark rate increases, the interest rate on the loan rises, leading to higher monthly payments. Conversely, if the benchmark rate decreases, the loan’s interest rate may drop, potentially lowering the borrower’s monthly obligations. While variable rates can sometimes start lower than fixed rates, they introduce uncertainty, making long-term financial planning more challenging.

For unsubsidized federal student loans, the U.S. Department of Education sets fixed interest rates annually, which are determined by federal law. These rates are based on the 10-year Treasury note yield plus a margin, and they remain the same for the life of the loan. For example, as of recent data, undergraduate unsubsidized Direct Loans have a fixed rate of around 5.5%, while graduate loans may have a slightly higher rate. This fixed structure ensures that borrowers are not exposed to market volatility, providing a layer of financial security.

Private unsubsidized student loans, however, often offer both fixed and variable rate options. Borrowers must carefully consider their financial situation and risk tolerance when choosing between the two. Fixed rates from private lenders may be higher initially but provide long-term stability. Variable rates might start lower, but they carry the risk of increasing over time, potentially making the loan more expensive in the long run. It’s essential to compare offers from multiple lenders and evaluate how each option aligns with your repayment strategy.

Lastly, understanding the repayment interest rates on unsubsidized student loans is key to managing debt effectively. Fixed rates offer simplicity and predictability, making them a safer choice for many borrowers. Variable rates, while potentially more affordable initially, come with inherent risks tied to market changes. Borrowers should assess their financial goals, expected income trajectory, and comfort with risk before deciding. Additionally, exploring repayment plans, such as income-driven options, can help mitigate the impact of interest rates on monthly payments, ensuring a more manageable loan repayment journey.

Understanding Student Loan Interest: What Counts and Why It Matters

You may want to see also

Explore related products

![]()

Deferment Interest Rules: Interest still accrues during deferment periods unless subsidized

When considering the interest on unsubsidized student loans, it's crucial to understand the deferment interest rules, particularly how interest accrues during these periods. Deferment allows borrowers to temporarily pause their loan payments under specific conditions, such as returning to school, experiencing economic hardship, or serving in the military. However, for unsubsidized loans, interest continues to accrue during deferment, which can significantly impact the total cost of the loan over time. This is in contrast to subsidized loans, where the government covers the interest during deferment periods.

The accrual of interest during deferment on unsubsidized loans means that the unpaid interest is added to the principal balance of the loan. This process, known as capitalization, increases the total amount borrowed, and subsequently, the overall cost of the loan. For example, if a borrower has a $20,000 unsubsidized loan with a 5% interest rate and enters a 12-month deferment period, approximately $1,000 in interest will accrue. If this interest is not paid during the deferment, it will be capitalized, increasing the loan balance to $21,000. When repayment resumes, the borrower will then be charged interest on this new, higher balance.

To mitigate the effects of interest capitalization, borrowers have the option to make interest payments during the deferment period, even if they are not required to make full loan payments. By paying the interest as it accrues, borrowers can prevent the increase in their loan balance and reduce the total cost of the loan. This proactive approach can save hundreds or even thousands of dollars over the life of the loan. It’s important for borrowers to carefully consider their financial situation and explore this option if feasible.

Understanding the deferment interest rules is essential for effective loan management. Borrowers should be aware of the type of loans they have—whether subsidized or unsubsidized—and how interest accrual during deferment will affect their repayment obligations. Lenders and loan servicers are required to provide clear information about these rules, but borrowers should also take the initiative to educate themselves. Resources such as the Federal Student Aid website offer detailed explanations and tools to help borrowers calculate potential interest accrual and plan accordingly.

Lastly, borrowers should explore all available options to manage their loans during deferment. In addition to making interest payments, they can consider other strategies, such as switching to an income-driven repayment plan once out of deferment, which can adjust monthly payments based on income and family size. Additionally, staying in communication with the loan servicer can provide access to valuable advice and potential assistance programs. By staying informed and proactive, borrowers can minimize the financial burden of unsubsidized student loans, even during deferment periods.

Understanding the Real Interest Rate on Student Loans: What You Need to Know

You may want to see also

Explore related products

![]()

Forbearance Interest Costs: Interest continues to accrue during forbearance, increasing total debt

Forbearance can be a temporary solution for borrowers struggling to make their student loan payments, but it comes with a significant financial trade-off: interest continues to accrue during the forbearance period. Unlike deferment, where interest may be subsidized for certain types of loans, forbearance does not halt the accumulation of interest on unsubsidized student loans. This means that even though payments are paused, the loan balance grows as interest compounds over time. For unsubsidized loans, which already accrue interest from the time of disbursement, forbearance exacerbates the problem by allowing this interest to pile onto the principal balance.

The mechanics of interest accrual during forbearance are straightforward but costly. For example, if a borrower has a $30,000 unsubsidized student loan with a 5% interest rate and enters a 12-month forbearance period, approximately $1,500 in interest will accrue during that time. This amount is then capitalized, meaning it is added to the principal balance of the loan. As a result, the borrower’s total debt increases, and future interest calculations are based on this higher balance. This cycle can lead to substantial long-term costs, as the borrower ends up paying interest on the capitalized interest, effectively paying "interest on interest."

Borrowers often underestimate the impact of forbearance interest costs, particularly when facing short-term financial hardships. While forbearance provides immediate relief by pausing payments, it does not address the underlying issue of growing debt. Over time, this can make it harder for borrowers to manage their loans, as the increased balance leads to higher monthly payments once the forbearance period ends. For those with unsubsidized loans, this is especially problematic, as these loans already carry a higher financial burden due to continuous interest accrual.

To mitigate forbearance interest costs, borrowers should explore alternative options before choosing forbearance. Income-driven repayment plans, for instance, can lower monthly payments based on income and family size, often resulting in more manageable terms without the added cost of capitalized interest. Additionally, borrowers with unsubsidized loans may consider making interest-only payments during periods of financial hardship to prevent capitalization. While this requires some cash flow, it is far less costly than allowing interest to compound unchecked.

In summary, forbearance interest costs can significantly increase the total debt of unsubsidized student loan borrowers. By allowing interest to accrue and capitalize, forbearance turns a temporary pause in payments into a long-term financial burden. Borrowers should carefully weigh the immediate relief of forbearance against the future costs and explore alternative strategies to manage their loans more effectively. Understanding these implications is crucial for making informed decisions and minimizing the overall impact of student loan debt.

Student Loans: Which Ones Start Accruing Interest Immediately?

You may want to see also

Frequently asked questions

The interest on unsubsidized student loans is the rate at which the loan balance accrues interest while the borrower is in school, during the grace period, and throughout the repayment period. Unlike subsidized loans, the government does not cover the interest on unsubsidized loans, so it begins to accrue immediately after the loan is disbursed.

The interest rate for unsubsidized student loans is determined by the federal government and is based on the 10-year Treasury note index, plus a fixed percentage. For undergraduate students, the rate is typically higher than that of subsidized loans. The interest rate is fixed for the life of the loan, meaning it will not change over time.

You are responsible for paying the interest on your unsubsidized student loans as soon as the loan is disbursed. If you choose not to pay the interest while in school, during the grace period, or during deferment or forbearance, the unpaid interest will be capitalized (added to the principal balance) when repayment begins, increasing the total amount you owe.