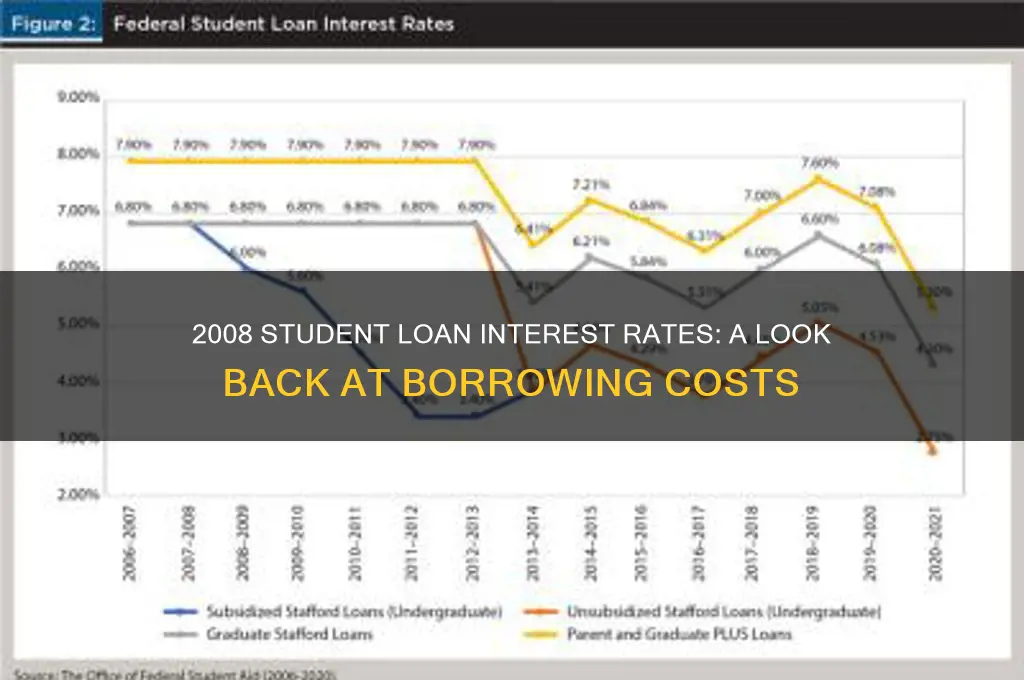

In 2008, student loan interest rates were a significant concern for borrowers in the United States, reflecting broader economic conditions and policy decisions. Federal student loan rates, which are set by Congress, varied depending on the type of loan and the borrower's educational level. For instance, subsidized Stafford loans for undergraduate students had a fixed rate of 6.0% for the 2007-2008 academic year, while unsubsidized Stafford loans carried the same rate. Graduate students faced higher rates, with unsubsidized Stafford loans at 6.8%. Private student loans, on the other hand, often had variable rates tied to market indices like the Prime Rate, which fluctuated throughout the year due to the Federal Reserve's actions in response to the financial crisis. The economic downturn in 2008 also led to increased scrutiny of student loan debt, as rising unemployment and financial instability made repayment more challenging for many borrowers.

| Characteristics | Values |

|---|---|

| Undergraduate Subsidized Stafford Loans (July 1, 2007 - June 30, 2008) | 6.80% |

| Undergraduate Unsubsidized Stafford Loans (July 1, 2007 - June 30, 2008) | 6.80% |

| Graduate Unsubsidized Stafford Loans (July 1, 2007 - June 30, 2008) | 6.80% |

| PLUS Loans for Parents and Graduate Students (July 1, 2007 - June 30, 2008) | 8.50% |

| Consolidation Loans (Variable Rate, weighted average of underlying loans) | Varied, typically between 6.80% - 8.50% |

| Note: | Interest rates for federal student loans in 2008 were fixed for the life of the loan, as per the terms of the loans originated during that period. |

Explore related products

What You'll Learn

![]()

Historical interest rates for federal student loans in 2008

In 2008, the interest rates for federal student loans in the United States were influenced by the Higher Education Act of 1965, as amended, and subsequent legislation. The rates varied depending on the type of loan and the year of disbursement. For undergraduate students, the most common federal loan was the Federal Stafford Loan, which had both subsidized and unsubsidized options. The subsidized Stafford Loans, where the government pays the interest while the student is in school, had a fixed interest rate of 6.0% for loans first disbursed between July 1, 2006, and June 30, 2008. This rate was part of a phased reduction plan outlined in the College Cost Reduction and Access Act of 2007, which aimed to lower rates over several years.

For unsubsidized Stafford Loans, where the borrower is responsible for all interest, the rate was also 6.0% for the same period. However, it is important to note that unsubsidized loans were available to both undergraduate and graduate students, whereas subsidized loans were limited to undergraduates with demonstrated financial need. Graduate and professional students had access to the Federal PLUS Loan program, which allowed parents and graduate students to borrow directly from the federal government. In 2008, the interest rate for Federal PLUS Loans was 7.9%, a fixed rate that applied to loans disbursed before July 1, 2006, and after June 30, 2008.

The interest rates for federal student loans in 2008 were also impacted by the economic climate. The financial crisis that began in 2007 led to significant economic uncertainty, prompting the Federal Reserve to lower interest rates to stimulate the economy. However, federal student loan rates were not directly tied to the Federal Reserve’s actions and remained fixed for the academic year. This stability provided borrowers with predictable repayment terms, though it also meant that rates did not decrease in response to the broader economic downturn.

Another important aspect of federal student loans in 2008 was the introduction of the Income-Based Repayment (IBR) plan, which capped monthly loan payments at a percentage of the borrower’s discretionary income. While this did not directly affect interest rates, it provided borrowers with more flexible repayment options, particularly as interest accrued over time. Understanding these historical rates is crucial for borrowers and policymakers alike, as it highlights the evolution of student loan programs and the financial burden faced by students during that period.

In summary, 2008 marked a transitional year for federal student loan interest rates, with subsidized and unsubsidized Stafford Loans at 6.0% and Federal PLUS Loans at 7.9%. These rates reflected legislative efforts to reduce borrowing costs for students while maintaining fixed terms to ensure predictability. The economic challenges of the time underscored the importance of accessible and affordable student financing, setting the stage for future reforms in the student loan system.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Private student loan interest rates in 2008

In 2008, private student loan interest rates were significantly influenced by the broader economic climate, particularly the financial crisis that began to unfold in the latter part of the year. Unlike federal student loans, which have fixed interest rates set by the government, private student loan rates are determined by market conditions and the borrower’s creditworthiness. During this period, the prime rate—a key benchmark for many private loans—fluctuated due to the Federal Reserve’s efforts to stabilize the economy. As a result, private student loan interest rates in 2008 varied widely, typically ranging from 7% to 12% or higher, depending on the lender and the borrower’s financial profile.

One of the defining characteristics of private student loans in 2008 was their reliance on variable interest rates. Many lenders offered loans with rates tied to the prime rate or LIBOR (London Interbank Offered Rate), meaning that as these benchmarks changed, so did the borrower’s interest rate. For students and families borrowing during this time, this introduced an element of uncertainty, as the financial crisis led to unpredictable shifts in interest rates. Borrowers with strong credit histories or cosigners often secured lower rates, while those with limited or poor credit faced higher costs, sometimes exceeding 15%.

The economic downturn in 2008 also impacted the availability of private student loans. As financial institutions tightened lending standards, many lenders became more selective about who they approved for loans. This made it harder for students with average or below-average credit to qualify, even if they were willing to accept higher interest rates. Additionally, some lenders exited the private student loan market altogether, reducing competition and potentially driving rates higher for those who could still access these loans.

Another important factor in 2008 was the lack of borrower protections for private student loans compared to federal loans. Private loans typically did not offer income-driven repayment plans, deferment options, or loan forgiveness programs. This meant that borrowers had to carefully consider their ability to repay the loans, especially with variable rates that could increase over time. Financial advisors often cautioned students to exhaust federal loan options before turning to private loans due to these risks and the generally higher costs associated with private borrowing.

In summary, private student loan interest rates in 2008 were marked by variability, higher costs, and increased scrutiny from lenders. The financial crisis created an environment of uncertainty, with rates fluctuating based on market conditions and individual creditworthiness. Borrowers faced challenges in securing loans, particularly those with less-than-ideal credit histories, and had to navigate the risks of variable rates without the safety nets provided by federal loans. Understanding these dynamics is crucial for anyone examining the historical context of student loan interest rates during this pivotal year.

Understanding Student Loan Interest Rates: What Spread Should You Expect?

You may want to see also

Explore related products

![[Theory of Interest (Int'l Ed)] [By: Kellison, Stephen] [April, 2008]](https://m.media-amazon.com/images/I/41XwTbm-90L._AC_UY218_.jpg)

![]()

Impact of 2008 financial crisis on student loan rates

The 2008 financial crisis had a profound impact on the economy, and one of the areas significantly affected was student loan interest rates. Prior to the crisis, student loan rates were relatively stable, with federal Stafford loans for undergraduates carrying a fixed interest rate of 6.8% in the 2007-2008 academic year. However, as the financial crisis unfolded, the federal government took measures to stimulate the economy and provide relief to borrowers. In May 2008, the Ensuring Continued Access to Student Loans Act was passed, which temporarily increased the federal subsidy for student loans and lowered interest rates for new loans.

As a result of this legislation, student loan interest rates began to decrease. For the 2008-2009 academic year, the interest rate for federal Stafford loans for undergraduates was lowered to 6.0%. This reduction was aimed at making student loans more affordable for borrowers during a time of economic uncertainty. The crisis also led to a shift towards more federal lending, as private student loan providers became more risk-averse and tightened their lending criteria. This increased demand for federal student loans put pressure on the government to keep interest rates low and maintain access to affordable financing for students.

The impact of the 2008 financial crisis on student loan rates was also felt in the private loan market. As credit markets froze and lenders became more cautious, private student loan interest rates increased significantly. Many private lenders stopped offering student loans altogether, leaving students with fewer options for financing their education. Those who were able to secure private loans often faced higher interest rates, fees, and stricter repayment terms. This situation highlighted the importance of federal student loans, which continued to offer relatively low, fixed interest rates and more flexible repayment options.

In response to the crisis, the federal government implemented further measures to support student borrowers. The American Opportunity Tax Credit, introduced in 2009, provided tax credits for tuition and related expenses, effectively reducing the cost of college for many families. Additionally, the Income-Based Repayment (IBR) plan was expanded, allowing more borrowers to cap their monthly loan payments at a percentage of their discretionary income. These initiatives, combined with the lower interest rates, helped to mitigate the impact of the financial crisis on student loan borrowers and ensured that access to higher education remained a viable option for many.

The long-term effects of the 2008 financial crisis on student loan rates are still evident today. The crisis accelerated a trend towards increased federal involvement in student lending, with the government becoming the primary source of student loans. This shift has had implications for interest rate policy, as federal student loan rates are now set by Congress and tied to the 10-year Treasury note. While this has provided stability and predictability for borrowers, it has also led to debates about the appropriate level of interest rates and the role of the government in student lending. As the economy continues to evolve, the impact of the 2008 financial crisis on student loan rates serves as a reminder of the complex interplay between economic conditions, government policy, and access to education financing.

In conclusion, the 2008 financial crisis had a significant and lasting impact on student loan interest rates. The crisis led to temporary reductions in federal student loan rates, increased federal lending, and highlighted the importance of affordable financing for students. While the crisis also resulted in higher private loan rates and reduced access to private financing, government initiatives helped to mitigate these effects and support student borrowers. As the student loan landscape continues to evolve, understanding the impact of the 2008 financial crisis on interest rates remains crucial for borrowers, policymakers, and educators alike.

Federal Student Loan Interest Rates in 2002: A Historical Overview

You may want to see also

Explore related products

![]()

Fixed vs. variable interest rates in 2008

In 2008, the landscape of student loan interest rates was characterized by a mix of fixed and variable rate options, each with distinct advantages and drawbacks. Fixed interest rates remained constant over the life of the loan, providing borrowers with predictability and stability in their monthly payments. This was particularly appealing during a time of economic uncertainty, as the U.S. was entering the Great Recession. For federal student loans, the fixed interest rate for subsidized Stafford loans was set at 6.0% for undergraduate students, while unsubsidized Stafford loans carried the same rate. Graduate and professional students faced higher fixed rates, with subsidized Stafford loans at 6.8% and unsubsidized loans also at 6.8%. These fixed rates offered peace of mind, as borrowers knew exactly how much they would pay over the loan term, regardless of market fluctuations.

On the other hand, variable interest rates in 2008 were tied to financial indices, such as the London Interbank Offered Rate (LIBOR), and fluctuated based on market conditions. Private student loans often featured variable rates, which could start lower than fixed rates but carried the risk of increasing over time. For instance, some private lenders offered variable rates as low as 3.25% initially, but these rates could rise significantly if market interest rates climbed. This made variable rates a double-edged sword: while they could save borrowers money in a low-interest-rate environment, they also exposed them to potential payment shocks if rates increased. In 2008, as the Federal Reserve began cutting rates to stimulate the economy, variable rates initially appeared attractive, but borrowers had to weigh the risk of future increases.

The choice between fixed and variable rates in 2008 depended largely on a borrower's risk tolerance and financial outlook. Fixed rates were ideal for those who prioritized stability and wanted to avoid surprises in their repayment plans. This was especially true for students who expected to take several years to repay their loans, as it protected them from potential rate hikes. Conversely, variable rates appealed to borrowers who were comfortable with uncertainty and believed they could manage higher payments if rates rose. Some borrowers also opted for variable rates with the intention of paying off their loans quickly, before any significant rate increases could occur.

Another factor influencing the decision was the economic climate of 2008. As the financial crisis unfolded, fixed rates became increasingly attractive, as they shielded borrowers from the volatility of the market. Variable rates, while initially lower, became riskier as the Federal Reserve's actions to lower interest rates were seen as a response to a weakening economy. Borrowers had to consider not only the current rate environment but also the potential for prolonged economic instability. This made fixed rates a safer bet for many, despite their higher starting point compared to some variable rate options.

In summary, the fixed vs. variable interest rate debate in 2008 was shaped by economic uncertainty and individual financial strategies. Fixed rates offered stability and predictability, making them a popular choice for federal student loans and risk-averse borrowers. Variable rates, while potentially more affordable initially, carried the risk of increasing payments and were more common in private loans. Borrowers had to carefully assess their financial situations, risk tolerance, and the broader economic outlook to make an informed decision. Understanding these differences was crucial for managing student loan debt effectively during a tumultuous financial period.

Understanding Subsidized Government Student Loans: Interest Rates Explained

You may want to see also

Explore related products

![]()

Subsidized vs. unsubsidized loan interest rates in 2008

In 2008, student loan interest rates were a critical factor for borrowers, with significant differences between subsidized and unsubsidized loans. Subsidized loans, available to undergraduate students with demonstrated financial need, offered a key advantage: the federal government paid the interest on these loans while the borrower was in school, during the grace period after graduation, and in periods of approved deferment. This feature made subsidized loans a more affordable option for eligible students. The interest rate for subsidized Stafford loans in the 2008-2009 academic year was 6.0% for undergraduate students, a rate that was fixed for the life of the loan. This rate was part of a phased reduction plan outlined in the College Cost Reduction and Access Act of 2007, which aimed to lower rates over time.

In contrast, unsubsidized loans were available to both undergraduate and graduate students regardless of financial need, but borrowers were responsible for paying all interest that accrued on the loan. For unsubsidized Stafford loans in 2008, the interest rate was also 6.0% for undergraduate students, matching the subsidized rate. However, the primary difference lay in the interest accrual: since borrowers did not receive government assistance, any unpaid interest would capitalize, increasing the total loan balance over time. This made unsubsidized loans potentially more costly in the long run, especially if borrowers deferred payments.

For graduate and professional students, the interest rates for unsubsidized Stafford loans in 2008 were higher than those for undergraduates. Graduate students faced a rate of 6.8%, which was already in effect before the phased reductions began. This disparity highlighted the importance of understanding the terms of each loan type, as graduate students often relied more heavily on unsubsidized loans due to limited eligibility for subsidized options.

Another important distinction in 2008 was the role of private student loans, which often had variable interest rates that could exceed those of federal loans. While federal subsidized and unsubsidized loans offered fixed rates, private loans were tied to market conditions and the borrower’s creditworthiness. This made federal loans, despite their 6.0% rate, a more stable and predictable option for many students. Borrowers were encouraged to exhaust federal loan options before considering private loans due to the added protections and benefits of federal programs.

In summary, 2008 student loan interest rates reflected a clear divide between subsidized and unsubsidized federal loans. Subsidized loans at 6.0% for undergraduates offered a financial cushion by eliminating interest payments during key periods, while unsubsidized loans, also at 6.0% for undergraduates, required borrowers to manage accruing interest. Graduate students faced higher unsubsidized rates at 6.8%, emphasizing the need for careful planning. Understanding these differences was essential for borrowers to make informed decisions and minimize long-term debt.

Where to Find Your Student Loan Interest Statement: A Quick Guide

You may want to see also

Frequently asked questions

In 2008, the average student loan interest rate for federal Stafford loans was around 6.8% for subsidized loans and 6.8% for unsubsidized loans for undergraduate students. Graduate students faced rates of 6.8% for unsubsidized loans.

Yes, in 2008, the Higher Education Act of 2008 introduced changes to federal student loan interest rates, gradually reducing them over time. For example, subsidized Stafford loan rates began a phased reduction from 6.8% to 3.4% by 2011.

Private student loan interest rates in 2008 varied widely, typically ranging from 7% to 12% or higher, depending on the borrower's creditworthiness and market conditions.

In 2008, federal student loans had fixed interest rates, while private student loans often offered both fixed and variable rate options, with variable rates tied to market indices like LIBOR or Prime.

The 2008 financial crisis led to tighter credit markets, making it harder for some borrowers to qualify for private student loans. However, federal student loan interest rates remained stable, as they are set by Congress and not directly influenced by market fluctuations.