Student loans can be a critical tool for financing education, but understanding how interest accrues is essential for managing repayment effectively. Not all student loans accumulate interest in the same way; it largely depends on the type of loan. Federal subsidized loans, for instance, do not accrue interest while the borrower is in school, during the grace period, or in deferment, as the government covers the interest costs. In contrast, federal unsubsidized loans and most private student loans begin accumulating interest immediately after disbursement, regardless of the borrower's enrollment status. This means that unsubsidized and private loans can significantly increase the total repayment amount over time if the interest is not paid while the borrower is still in school. Understanding these differences is crucial for borrowers to make informed decisions and avoid unnecessary financial burden.

Explore related products

What You'll Learn

- Federal Subsidized Loans: No interest while in school, grace period, or deferment

- Federal Unsubsidized Loans: Interest accrues immediately after disbursement, even during school

- Private Student Loans: Interest typically accrues from the date of disbursement

- Loan Repayment Plans: Interest continues to accrue during income-driven or extended repayment

- Loan Deferment/Forbearance: Interest may still accrue, depending on loan type

![]()

Federal Subsidized Loans: No interest while in school, grace period, or deferment

Federal Subsidized Loans are a unique and advantageous type of student loan offered by the U.S. Department of Education, specifically designed to help undergraduate students with demonstrated financial need. One of the most significant benefits of these loans is that they do not accumulate interest while the borrower is enrolled in school at least half-time, during the grace period after leaving school, or during any approved deferment period. This feature sets Federal Subsidized Loans apart from other types of student loans, such as unsubsidized loans, which begin accruing interest immediately after disbursement.

While the borrower is in school, the government covers the interest on the loan, preventing the balance from growing. This is a crucial benefit, as it allows students to focus on their studies without the added financial burden of increasing debt. The interest-free period continues during the grace period, which typically lasts for six months after the borrower graduates, leaves school, or drops below half-time enrollment. During this time, borrowers can prepare for repayment without worrying about interest accrual, providing a buffer to transition into the workforce or further education.

Another key advantage of Federal Subsidized Loans is the deferment option. If a borrower encounters financial hardship, returns to school, or meets other qualifying conditions, they can apply for deferment. During an approved deferment, the loan remains interest-free, and repayment is temporarily paused. This flexibility is particularly valuable for borrowers facing unemployment, economic hardship, or other challenges that make repayment difficult. It ensures that the loan balance does not increase during these periods, offering much-needed relief.

It’s important to note that not all students qualify for Federal Subsidized Loans, as eligibility is based on financial need determined by the Free Application for Federal Student Aid (FAFSA). However, for those who do qualify, these loans are a highly beneficial option due to their interest-free provisions. In contrast, Federal Unsubsidized Loans, which are available to all students regardless of financial need, do accumulate interest from the time of disbursement, making subsidized loans the more cost-effective choice for eligible borrowers.

In summary, Federal Subsidized Loans stand out as a borrower-friendly option because they do not accumulate interest while the borrower is in school, during the grace period, or during deferment. This feature significantly reduces the overall cost of borrowing and provides financial flexibility during critical periods. For students with demonstrated financial need, these loans are an excellent tool to fund their education without the added stress of growing interest. Understanding these benefits is essential when navigating the complexities of student loans and choosing the best financing options for higher education.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Federal Unsubsidized Loans: Interest accrues immediately after disbursement, even during school

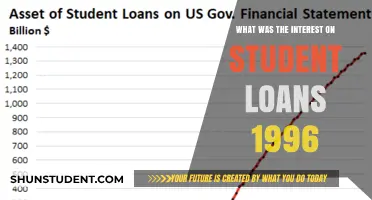

Federal Unsubsidized Loans are a type of student loan offered by the U.S. Department of Education that begins accumulating interest immediately after the loan is disbursed. Unlike subsidized loans, where the government covers the interest while the borrower is in school, unsubsidized loans require the borrower to take responsibility for the interest from day one. This means that even if you are still in school, enrolled at least half-time, or during grace periods after leaving school, interest will continue to accrue on the loan balance. Understanding this key difference is crucial for borrowers, as it directly impacts the total amount you’ll need to repay over the life of the loan.

The interest on Federal Unsubsidized Loans is calculated daily and compounds over time, meaning that unpaid interest is added to the principal balance. This process, known as capitalization, increases the total amount of the loan, and subsequently, the amount of interest that accrues. For students, this can lead to a significantly higher loan balance by the time they graduate if the interest is not paid as it accrues. While you have the option to pay the interest while in school, many borrowers choose not to, which can result in a larger financial burden post-graduation.

One of the challenges with Federal Unsubsidized Loans is that the interest begins to accrue at the time of disbursement, often before the borrower even starts using the funds for educational expenses. This immediate accrual of interest can be particularly burdensome for students who are not yet earning an income and may not have the means to make interest payments. Over time, this can lead to a situation where the loan balance grows rather than shrinks, even if the borrower is making on-time payments later on.

Borrowers should also be aware that the interest rates on Federal Unsubsidized Loans are fixed but can vary depending on the year the loan was taken out. These rates are set by Congress and are generally lower than those of private loans, but they still contribute to the overall cost of borrowing. It’s important to review the terms of your loan agreement to understand the specific interest rate applied to your unsubsidized loan and how it will affect your repayment obligations.

To mitigate the impact of accruing interest on Federal Unsubsidized Loans, borrowers have a few strategies at their disposal. Paying the interest while in school, even if it’s just the monthly accrual, can prevent capitalization and keep the loan balance from growing. Additionally, making interest payments during grace periods or deferment can help manage the overall cost of the loan. For those who cannot afford to pay the interest during these periods, understanding the long-term implications and planning for higher repayments after graduation is essential.

In summary, Federal Unsubsidized Loans are a critical component of many students’ financial aid packages, but they come with the significant drawback of immediate interest accrual. This feature distinguishes them from subsidized loans and requires borrowers to be proactive in managing their loan balances. By understanding how interest accrues and exploring strategies to minimize its impact, students can better navigate the complexities of unsubsidized loans and reduce their long-term financial burden.

Maximizing Tax Savings: Standard Deduction for Single Student Loan Interest

You may want to see also

Explore related products

![]()

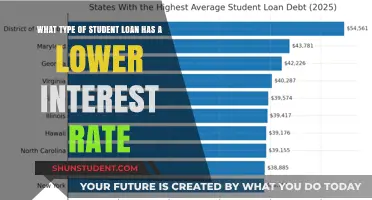

Private Student Loans: Interest typically accrues from the date of disbursement

Private student loans are a common financing option for students seeking to cover educational expenses, but they come with distinct terms that borrowers must understand, particularly regarding interest accrual. Unlike federal student loans, which may offer subsidized options where the government pays the interest while the borrower is in school, private student loans typically begin accruing interest from the date of disbursement. This means that as soon as the loan funds are released to the borrower or their school, interest starts to accumulate on the principal balance. This immediate accrual of interest is a critical factor that can significantly increase the total cost of the loan over time.

The mechanism of interest accrual in private student loans is straightforward but can be financially burdensome if not managed properly. Interest is calculated daily based on the outstanding loan balance and the applicable interest rate. For example, if a student borrows $10,000 with an annual interest rate of 6%, interest will begin to compound daily from the disbursement date. Over time, this can lead to a growing loan balance, even if the borrower is not required to make payments while in school. Borrowers who do not make interest-only payments during their academic period will face a larger repayment amount once the grace period ends, as the accrued interest is capitalized and added to the principal.

One of the key differences between private and federal student loans lies in the flexibility and borrower protections offered. Private lenders often require credit checks and may offer variable interest rates, which can fluctuate over the life of the loan, further complicating repayment. Additionally, private loans rarely provide income-driven repayment plans or loan forgiveness options, which are common with federal loans. This lack of flexibility underscores the importance of understanding the terms of private loans, especially the immediate accrual of interest, to avoid financial strain.

To mitigate the impact of interest accrual, borrowers should consider making interest payments while still in school, even if it is not required. Paying the accruing interest monthly prevents capitalization and keeps the overall loan balance from growing. Another strategy is to compare lenders and choose one with the lowest interest rate and favorable repayment terms. Some private lenders also offer interest rate discounts for enrolling in automatic payments or for borrowers with strong credit histories. Proactive management of private student loans from the outset can save borrowers thousands of dollars over the life of the loan.

In summary, private student loans are a financial tool that requires careful consideration due to their immediate interest accrual from the disbursement date. Borrowers must be aware of how daily interest calculations and capitalization can increase the total cost of the loan. By understanding these terms and exploring strategies to manage accruing interest, students can make informed decisions and minimize the long-term financial burden of their private loans. Always read the loan agreement thoroughly and consider consulting a financial advisor to navigate the complexities of private student loan borrowing.

Tax-Deductible Student Loan Interest: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Loan Repayment Plans: Interest continues to accrue during income-driven or extended repayment

When considering student loan repayment plans, it’s crucial to understand that interest continues to accrue even under income-driven or extended repayment options. These plans are designed to lower monthly payments based on income or extend the repayment period, but they do not stop interest from accumulating. For example, unsubsidized federal student loans, including Direct Unsubsidized Loans and Grad PLUS Loans, accrue interest from the moment they are disbursed. Under income-driven plans like Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), the reduced monthly payment may not cover the full interest amount, leading to capitalization—where unpaid interest is added to the principal balance, increasing the total loan cost over time.

Income-driven repayment plans are particularly prone to interest accrual because they cap monthly payments at a percentage of discretionary income. If the calculated payment is less than the monthly interest, the remaining interest is added to the loan balance. For instance, borrowers with low incomes or large loan balances may find that their payments barely cover the interest, causing their total debt to grow. This is especially true for Direct Unsubsidized Loans and Grad PLUS Loans, which are not subsidized by the government and thus accrue interest regardless of the borrower’s repayment status.

Extended repayment plans, which stretch the repayment period up to 25 years, also allow interest to accumulate significantly over time. While these plans reduce monthly payments by spreading them out, the longer repayment term means more interest accrues overall. Borrowers with federal student loans, including both subsidized and unsubsidized types, will see interest add up, though subsidized loans only accrue interest during repayment (not while in school or during grace periods). However, once in an extended repayment plan, even subsidized loans begin to accumulate interest continuously.

It’s important to note that private student loans also accrue interest during any repayment plan, often at higher rates than federal loans. Private lenders rarely offer income-driven or extended repayment options, and their interest capitalization policies can be more aggressive. Borrowers with private loans should carefully review their loan terms to understand how interest accrues and compounds, as it can significantly increase the total repayment amount.

To mitigate the impact of accruing interest, borrowers should explore strategies such as making extra payments toward the principal when possible or switching to a standard repayment plan if their financial situation improves. Additionally, borrowers in income-driven plans may qualify for interest subsidies under certain conditions, such as the REPAYE plan, which covers half of the unpaid interest on subsidized loans for the first three years. However, these subsidies are limited and do not eliminate interest accrual entirely. Understanding how interest accumulates under different repayment plans is essential for managing student loan debt effectively.

Smart Strategies to Reduce Your Student Loan Interest Rates

You may want to see also

![]()

Loan Deferment/Forbearance: Interest may still accrue, depending on loan type

When considering loan deferment or forbearance as options to temporarily pause student loan payments, it’s crucial to understand how interest accrual varies depending on the type of loan. Federal student loans fall into distinct categories regarding interest accumulation during deferment or forbearance. For subsidized federal loans, such as Direct Subsidized Loans, the government covers the interest that accrues while the loan is in deferment. This means borrowers are not responsible for paying this interest later, making deferment a more financially neutral option for these loans. However, this benefit is specific to subsidized loans and does not apply to all federal loan types.

In contrast, unsubsidized federal loans, including Direct Unsubsidized Loans, Stafford Unsubsidized Loans, and PLUS Loans, do accumulate interest during periods of deferment or forbearance. Since the government does not pay this interest, it is added to the loan’s principal balance, a process known as capitalization. This increases the total amount owed over time, as future interest is calculated on a higher principal. Borrowers should carefully weigh the long-term costs of allowing interest to capitalize, as it can significantly increase the overall repayment burden.

Private student loans operate under different rules, which are often less favorable for borrowers. Most private loans accrue interest during deferment or forbearance, and lenders rarely cover this cost. Additionally, private lenders may have stricter eligibility requirements for deferment or forbearance and may capitalize interest more frequently. Borrowers with private loans should review their loan agreements carefully to understand how interest accrual works during pauses in repayment and explore alternatives, such as making interest-only payments if available, to minimize long-term costs.

It’s also important to note that deferment and forbearance are not automatic; borrowers must apply for these options and meet specific eligibility criteria. For federal loans, deferment is typically granted for reasons such as returning to school, unemployment, or economic hardship, while forbearance is more discretionary and may be approved for a wider range of financial difficulties. Private loan lenders have their own criteria, which may be less flexible. Regardless of the loan type, borrowers should proactively communicate with their loan servicers to understand their options and the associated interest implications.

Finally, borrowers should consider the long-term financial impact of choosing deferment or forbearance. While these options provide temporary relief from monthly payments, the accrual of interest—especially on unsubsidized and private loans—can lead to higher overall debt. If possible, continuing to make payments, even if only toward the accruing interest, can help mitigate this increase. Borrowers should also explore alternative repayment plans, such as income-driven plans for federal loans, which may offer lower monthly payments without the need for deferment or forbearance. Understanding these nuances ensures borrowers make informed decisions that align with their financial goals.

Student Loans That Defer Interest: Types and Eligibility Explained

You may want to see also

Frequently asked questions

Unsubsidized federal student loans and most private student loans accumulate interest while the borrower is in school.

No, subsidized federal student loans do not accumulate interest while the borrower is enrolled in school at least half-time.

If the interest on unsubsidized loans is not paid while in school, it capitalizes (added to the principal balance), increasing the total amount to be repaid.

Yes, most private student loans begin accumulating interest as soon as the loan is disbursed, regardless of enrollment status.

Subsidized federal student loans and some grants or scholarships do not accumulate interest, but these are limited to specific eligibility criteria.