The topic of student loan forgiveness has become a hot-button issue, with many borrowers seeking relief from their financial burdens. However, amidst the growing interest, there has been a surge in reports of suspicious calls claiming to offer student loan forgiveness programs. These calls often promise to eliminate or reduce loan balances in exchange for upfront fees or personal information, raising concerns about potential scams. As a result, many borrowers are left wondering whether these calls are legitimate or simply attempts to defraud them, making it crucial to understand the warning signs and protect oneself from falling victim to such schemes.

| Characteristics | Values |

|---|---|

| Unsolicited Calls | Scammers often initiate unsolicited calls claiming to offer student loan forgiveness. |

| Urgency or Pressure | They create a sense of urgency, claiming immediate action is required to avoid missing out. |

| Request for Payment | Scammers may ask for upfront fees or payments to process loan forgiveness. |

| Asking for Personal Information | They might request sensitive information like Social Security numbers, bank details, or loan account credentials. |

| Guaranteed Forgiveness | Scammers falsely guarantee loan forgiveness, even if the borrower doesn’t qualify. |

| Unknown or Spoofed Numbers | Calls often come from unfamiliar or spoofed phone numbers. |

| Lack of Official Documentation | Legitimate programs provide official documentation; scammers do not. |

| Promises of Instant Results | Scammers claim they can forgive loans immediately, which is unrealistic. |

| Threats or Intimidation | They may threaten legal action or credit damage if the borrower doesn’t comply. |

| Not Affiliated with Official Programs | Scammers are not affiliated with the U.S. Department of Education or legitimate loan servicers. |

| Too Good to Be True Offers | Offers that seem too good to be true, like complete loan forgiveness without eligibility checks. |

| No Written Agreement | Legitimate programs require written agreements; scammers avoid this step. |

| Poor Grammar or Unprofessionalism | Scammers may use poor grammar, unprofessional language, or vague details. |

| Verification Requests | Legitimate programs verify eligibility; scammers skip this step. |

| Third-Party Involvement | Scammers often claim to be from third-party companies, not official agencies. |

| No Record of Communication | Legitimate servicers keep records of communication; scammers do not. |

Explore related products

What You'll Learn

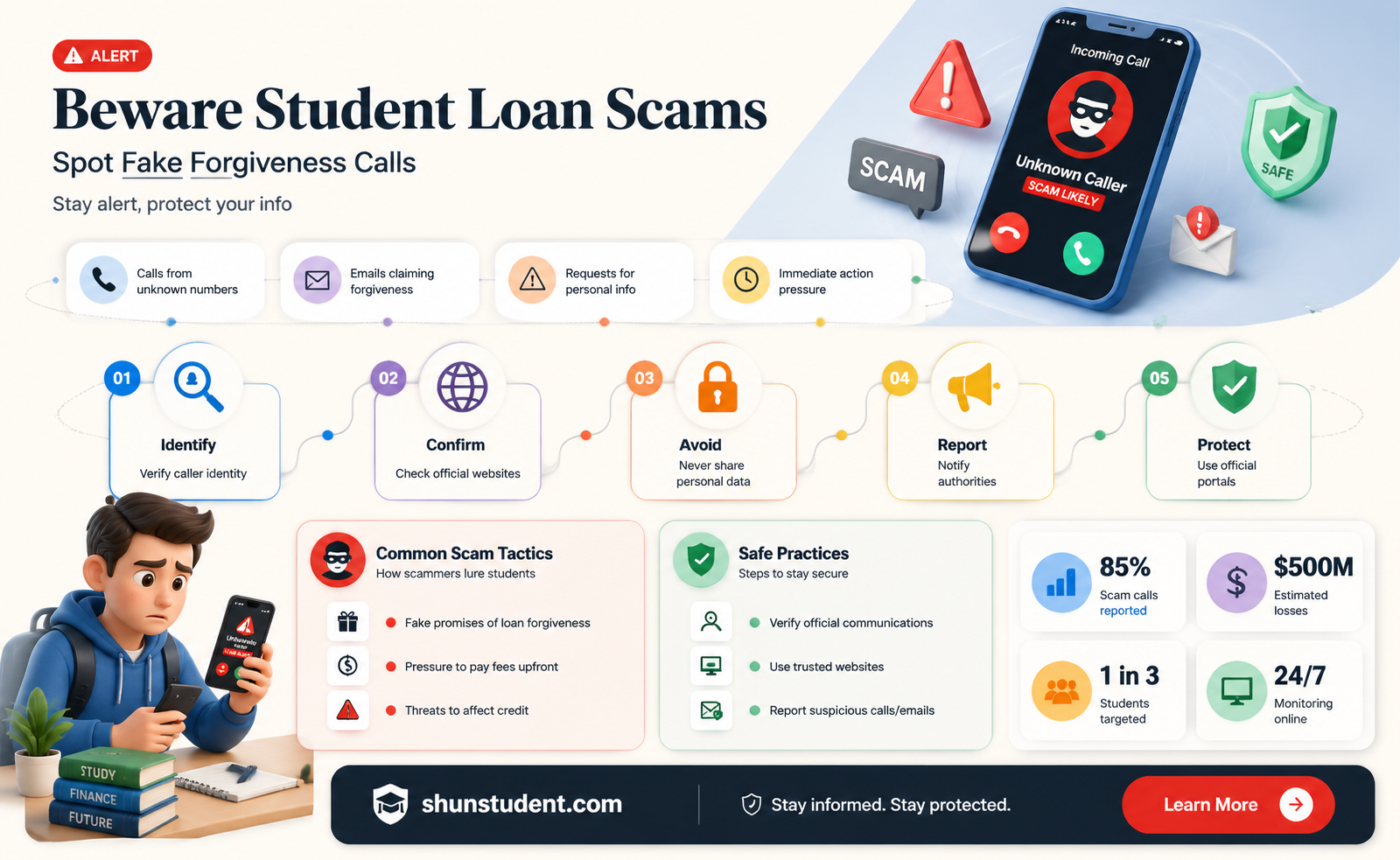

- Identifying Scam Calls: Key red flags to spot fraudulent student loan forgiveness offers over the phone

- Official Forgiveness Programs: Understanding legitimate government programs and their application processes

- Common Scam Tactics: How scammers pressure borrowers with urgency, fees, or fake promises

- Protecting Personal Information: Tips to safeguard data when discussing student loans on calls

- Reporting Scam Calls: Steps to report fraudulent activity to authorities and protect others

![]()

Identifying Scam Calls: Key red flags to spot fraudulent student loan forgiveness offers over the phone

Scam calls promising student loan forgiveness often begin with an urgent tone, claiming immediate action is required to avoid dire consequences. Legitimate loan servicers, however, rarely pressure borrowers with such tactics. If a caller insists you must act now or risk losing eligibility for forgiveness, it’s a red flag. Scammers exploit fear and urgency to bypass your critical thinking, so pause and verify the information independently before proceeding.

Another telltale sign is the request for upfront fees. Legitimate student loan forgiveness programs, such as those offered through the Department of Education, never require payment to process your application. If a caller demands money for "processing," "expediting," or "guaranteeing" forgiveness, hang up. Scammers often use phrases like "one-time fee" or "limited offer" to create a false sense of exclusivity, but these are tactics to extract cash, not to help you.

Be wary of callers who ask for sensitive personal information, such as your Federal Student Aid (FSA) ID, Social Security number, or bank account details. Legitimate servicers already have this information and would never request it unsolicited. Scammers use this data to commit identity theft or unauthorized transactions. If in doubt, contact your loan servicer directly using the official contact information on your account statement or the Department of Education’s website.

Lastly, pay attention to the caller’s tone and language. Scammers often use high-pressure sales tactics, making grandiose promises like "complete debt elimination" or "instant approval." They may also impersonate government agencies, using official-sounding names or titles to gain trust. Legitimate representatives are professional and transparent, providing clear, verifiable information without resorting to manipulative language. If something feels off, trust your instincts and end the call.

To protect yourself, follow these steps: first, never share personal information over the phone unless you initiated the call and verified the recipient’s identity. Second, research any program or company mentioned by the caller using trusted sources like the Better Business Bureau or the Federal Trade Commission. Finally, report suspicious calls to the FTC and your loan servicer to help prevent others from falling victim. Staying informed and cautious is your best defense against student loan forgiveness scams.

PSLF vs. Student Loan Forgiveness: Can You Apply for Both?

You may want to see also

Explore related products

![]()

Official Forgiveness Programs: Understanding legitimate government programs and their application processes

Legitimate student loan forgiveness programs exist, but they’re often misunderstood or overshadowed by scams. The U.S. Department of Education offers several official programs, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and Income-Driven Repayment (IDR) forgiveness. Each program has specific eligibility criteria, requiring borrowers to meet conditions like employment in qualifying public service roles, teaching in low-income schools, or making consistent payments under an IDR plan. Understanding these programs is crucial, as scammers often exploit confusion around their complexity to deceive borrowers.

To apply for PSLF, for example, borrowers must work full-time for a qualifying employer, such as a government or nonprofit organization, and make 120 eligible payments under an IDR plan. The process involves submitting an Employment Certification Form annually and a PSLF application after completing the required payments. Similarly, Teacher Loan Forgiveness requires teaching full-time for five consecutive years in a low-income school, with forgiveness amounts ranging from $5,000 to $17,500 depending on the subject taught. These programs are not automatic; borrowers must proactively apply and provide documentation to prove eligibility.

One common misconception is that forgiveness programs are widely accessible or easy to qualify for. In reality, strict criteria and paperwork requirements often limit eligibility. For instance, IDR forgiveness, which discharges remaining balances after 20–25 years of payments, is only available for federal loans under specific plans like REPAYE or PAYE. Private loans are ineligible for these programs, yet scammers frequently target private loan holders with false promises of forgiveness. Borrowers must verify their loan type and repayment plan before pursuing forgiveness.

To avoid scams, borrowers should only use official government resources, such as the Federal Student Aid website (studentaid.gov), to research and apply for forgiveness programs. Legitimate programs never require upfront fees or demand personal information over unsolicited calls. Instead, they provide clear guidelines and direct borrowers to submit applications through secure, official channels. By understanding the specifics of these programs and their application processes, borrowers can protect themselves from fraud while exploring legitimate paths to debt relief.

Stay Informed: Latest Updates on Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Common Scam Tactics: How scammers pressure borrowers with urgency, fees, or fake promises

Scammers often exploit the anxiety surrounding student loan debt by creating a false sense of urgency. They may claim that borrowers must act immediately to qualify for limited-time forgiveness programs or risk losing their eligibility forever. For instance, a common tactic involves sending text messages or leaving voicemails stating, “Your student loan forgiveness application expires in 24 hours—call now to secure your spot.” This high-pressure approach preys on fear, pushing borrowers to make hasty decisions without verifying the legitimacy of the offer. The reality is that official government loan forgiveness programs do not operate on such tight deadlines, and any claim of urgency should raise red flags.

Another red flag is the demand for upfront fees. Scammers frequently pose as debt relief companies, promising to negotiate lower payments or complete forgiveness for a fee. They might ask for payment via wire transfer, gift cards, or cryptocurrency, making it nearly impossible to recover the funds once the scam is realized. Legitimate loan servicers or government programs never require payment for assistance. Borrowers should be wary of any request for money in exchange for services related to loan forgiveness, especially if the company pressures them to pay before providing details about the process.

Fake promises are a cornerstone of these scams. Fraudsters may guarantee loan forgiveness or claim they can reduce monthly payments by 50% or more, regardless of the borrower’s financial situation. They often use official-sounding language or mimic government websites to appear credible. For example, a scammer might say, “We’re partnered with the Department of Education to offer exclusive forgiveness programs.” In reality, no third-party company can guarantee forgiveness, as eligibility depends on specific criteria like income and repayment plan enrollment. Borrowers should verify any claims by checking the official Federal Student Aid website or contacting their loan servicer directly.

To protect themselves, borrowers should follow a few practical steps. First, never share personal information like Social Security numbers or account details with unsolicited callers. Second, research any company claiming to offer loan forgiveness services through the Better Business Bureau or Consumer Financial Protection Bureau. Third, remember that legitimate loan forgiveness programs, such as Public Service Loan Forgiveness or Income-Driven Repayment plans, are free to apply for and do not require third-party assistance. By staying informed and cautious, borrowers can avoid falling victim to these predatory tactics.

Unemployed and Overwhelmed: A Guide to Student Loan Forgiveness

You may want to see also

Explore related products

![]()

Protecting Personal Information: Tips to safeguard data when discussing student loans on calls

Scammers often exploit the urgency and confusion surrounding student loan forgiveness programs, making unsolicited calls to collect personal information under false pretenses. To protect your data, start by verifying the caller’s identity. Legitimate loan servicers will never cold-call to request sensitive details like your Social Security number or bank account information. If you’re unsure, hang up and contact your loan servicer directly using the official number listed on your account statement or the Department of Education’s website. This simple step can prevent unauthorized access to your personal information.

Next, understand the red flags that signal a scam. Scammers often pressure you to act immediately, claiming your eligibility for forgiveness will expire if you don’t provide details right away. They may also ask for payment via unconventional methods, such as gift cards or cryptocurrency. Legitimate programs never require upfront fees or demand immediate action over the phone. If the caller’s tone feels aggressive or their requests seem suspicious, it’s a clear sign to end the conversation and report the call to the Federal Trade Commission (FTC).

A proactive approach to safeguarding your data involves limiting the information you share during calls. Even if the caller seems legitimate, avoid disclosing full Social Security numbers, account passwords, or financial details unless absolutely necessary. Instead, offer partial information (e.g., the last four digits of your SSN) and request that the caller verify your identity first. Additionally, enable multi-factor authentication on your loan accounts to add an extra layer of security, ensuring that even if scammers obtain some data, they can’t access your accounts.

Finally, stay informed about official student loan forgiveness programs and their communication methods. The Department of Education primarily communicates through written correspondence, such as emails or letters, and rarely initiates contact via phone. Familiarize yourself with the names of legitimate loan servicers and their policies. By educating yourself and remaining cautious, you can navigate discussions about student loans confidently while keeping your personal information secure.

Capitalized Student Loan Interest Forgiveness Under PSLF: What You Need to Know

You may want to see also

Explore related products

![]()

Reporting Scam Calls: Steps to report fraudulent activity to authorities and protect others

Scam calls about student loan forgiveness are rampant, preying on borrowers seeking financial relief. Reporting these calls isn’t just about protecting yourself—it’s a critical step in dismantling fraudulent networks and safeguarding others. Here’s how to act effectively.

Step 1: Document the Call Details

Immediately after receiving a suspicious call, jot down specifics: the caller’s phone number, any callback number provided, the name of the alleged company, and key phrases used (e.g., “immediate loan forgiveness” or “one-time offer”). If the call includes a recorded message, note its tone and urgency. Screenshots of caller IDs or voicemails can also serve as evidence. The Federal Trade Commission (FTC) emphasizes that detailed reports strengthen investigations, so precision matters.

Step 2: Report to Federal and State Authorities

Submit a formal complaint to the FTC at ReportFraud.ftc.gov or by calling 1-877-FTC-HELP. For student loan-specific scams, also notify the U.S. Department of Education’s Office of Inspector General (OIG) via their hotline at 1-800-MIS-USED or online at www.oig.ed.gov. If the scam involves identity theft, add a report to the IdentityTheft.gov platform. State attorney general offices often handle local scams, so file a parallel report there for faster regional action.

Step 3: Alert Your Loan Servicer and Credit Bureaus

Contact your federal student loan servicer (e.g., MOHELA, Nelnet) to flag potential fraud attempts. They can monitor your account for unauthorized changes. Simultaneously, place a free fraud alert with the three major credit bureaus (Equifax, Experian, TransUnion) to prevent identity theft. This step takes minutes but provides 90 days of protection, renewable as needed.

Cautions and Best Practices

Never share personal information (Social Security number, account details) during unsolicited calls. Legitimate loan forgiveness programs, like Public Service Loan Forgiveness, are free to apply for and never require upfront payment. Be wary of callers demanding payment via gift cards, cryptocurrency, or wire transfer—red flags for scams. Finally, avoid engaging with suspicious callers; hang up and report instead.

Reporting scam calls isn’t just bureaucratic busywork—it’s a civic duty. Each report contributes to databases used by law enforcement to track patterns, shut down fraudulent operations, and issue public warnings. By taking these steps, you not only protect yourself but also disrupt the cycle of deception targeting vulnerable borrowers. In the fight against student loan scams, your vigilance is a weapon. Use it.

Navigating Student Loan Forgiveness: Key Contacts for Debt Relief

You may want to see also

Frequently asked questions

No, not all calls are scams, but many are. Legitimate communications about student loan forgiveness typically come from official sources like the U.S. Department of Education or your loan servicer, often via email or mail, not unsolicited phone calls.

Scams often pressure you to act immediately, ask for upfront fees, or request personal information like your Social Security number or bank details. Legitimate programs never require upfront payments or ask for sensitive information over the phone.

Scammers may try to trick you into sharing login credentials or personal information, which they can use to access your account. Never share sensitive details with unsolicited callers.

Hang up immediately and verify the information by contacting your loan servicer or visiting the official Federal Student Aid website. Report the call to the Federal Trade Commission (FTC) to help prevent others from being scammed.

Yes, programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment plans exist. Apply directly through the U.S. Department of Education or your loan servicer, not through third-party companies offering "quick fixes."