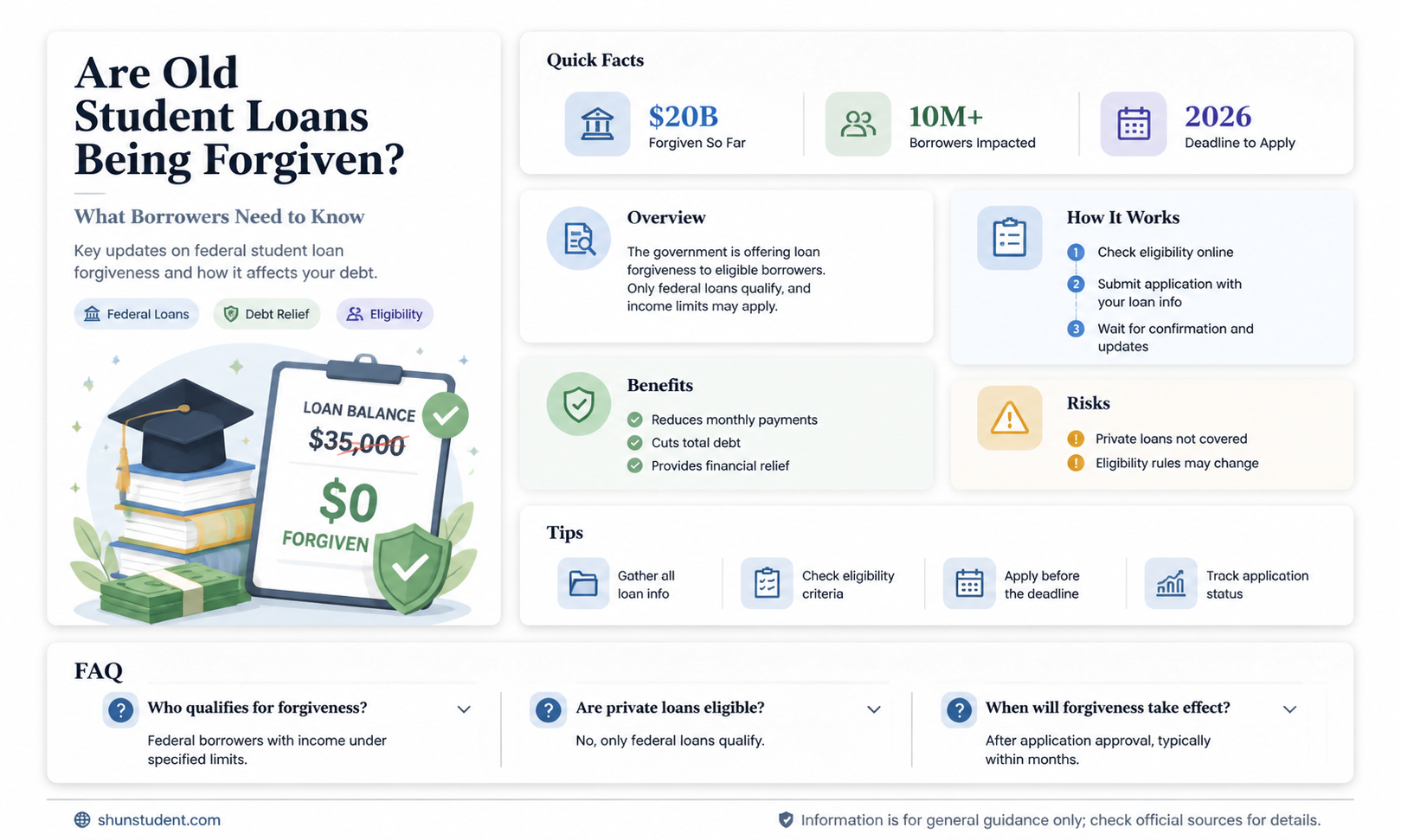

The topic of student loan forgiveness, particularly for older loans, has become a pressing issue in recent years, as millions of borrowers continue to struggle with mounting debt. With the cost of higher education skyrocketing and wages stagnating, many are left wondering if relief is on the horizon. The question of whether old student loans are being forgiven has gained traction, fueled by discussions around potential government policies, legal challenges, and advocacy efforts. As debates continue over the economic and social implications of widespread loan forgiveness, borrowers are eagerly awaiting clarity on whether their long-standing debts will finally be alleviated.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Limited to specific programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or income-driven repayment plans. |

| Recent Policy Changes | Biden administration's targeted loan forgiveness initiatives, including $1.2 billion in forgiveness for ITT Tech students (2023). |

| Income-Driven Repayment (IDR) Reform | Over 800,000 borrowers received $7.6 billion in forgiveness due to IDR account adjustments (2023). |

| Public Service Loan Forgiveness (PSLF) | Over 750,000 borrowers have received $42 billion in PSLF forgiveness since 2021. |

| One-Time Adjustment (2023) | Borrowers in repayment for 20-25 years (depending on loan type) received automatic forgiveness. |

| Loan Types Covered | Federal student loans (Direct Loans, FFELP loans if consolidated into Direct Loans). |

| Private Loans Forgiveness | No federal forgiveness for private loans; only state or employer programs may apply. |

| Tax Implications | Forgiveness under PSLF or closed school discharge is tax-free; other programs may have taxable income. |

| Application Process | Automatic for some (e.g., IDR adjustments); others require application (e.g., PSLF, closed school discharge). |

| Remaining Debt | Over $1.7 trillion in federal student loan debt remains outstanding (as of 2023). |

| Legal Challenges | Broad student loan forgiveness plans (e.g., $10,000-$20,000 relief) blocked by Supreme Court in 2023. |

| Future Outlook | Targeted forgiveness likely to continue; broad relief uncertain without legislative action. |

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for loan forgiveness based on age, income, or repayment plans

- Government Policies: Recent federal or state initiatives to forgive older student loans

- Public Service Loan Forgiveness: How older loans fit into PSLF programs

- Bankruptcy Discharge: Possibility of discharging old loans through bankruptcy

- Loan Cancellation Scams: Warnings about fraudulent schemes targeting borrowers with old debt

![]()

Eligibility Criteria: Who qualifies for loan forgiveness based on age, income, or repayment plans

The age of your student loans doesn’t automatically qualify them for forgiveness, but specific eligibility criteria tied to age, income, and repayment plans can pave the way. For instance, borrowers over 65 may face unique considerations under programs like Income-Driven Repayment (IDR) plans, which cap monthly payments based on income and family size. If you’ve been in repayment for 20–25 years under such plans, the remaining balance could be forgiven, though this depends on the plan’s terms and your adherence to them. Age alone isn’t a qualifier, but it intersects with repayment history and plan selection.

Income plays a pivotal role in determining eligibility for loan forgiveness, particularly under income-driven repayment plans and the Public Service Loan Forgiveness (PSLF) program. For IDR plans, borrowers with incomes below 150% of the federal poverty line may qualify for $0 monthly payments, which still count toward forgiveness. For example, a single borrower earning less than $20,445 annually in 2023 could meet this threshold. PSLF, on the other hand, requires 10 years of qualifying payments while working full-time for a government or nonprofit organization, regardless of income level. The key is consistent, on-time payments under the right plan.

Repayment plans are the backbone of forgiveness eligibility, with each plan offering distinct pathways. IDR plans like Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) forgive remaining balances after 20–25 years of payments, depending on the plan. Standard repayment plans, however, do not lead to forgiveness unless you switch to an IDR plan. Borrowers must also recertify their income annually for IDR plans to avoid losing eligibility. Practical tip: Use the Federal Student Aid Loan Simulator to determine which plan aligns with your financial goals and forgiveness timeline.

A lesser-known but critical factor is the type of loan you hold. Only federal student loans qualify for age- or income-based forgiveness programs; private loans are ineligible. Direct Loans, FFEL Loans (if consolidated into the Direct Loan program), and Perkins Loans are examples of eligible federal loans. If you’re unsure about your loan type, log into your account at StudentAid.gov to verify. Consolidating loans, if necessary, can simplify repayment and open doors to forgiveness programs, but beware: consolidating resets the clock on IDR forgiveness timelines.

Finally, staying informed and proactive is essential. Eligibility criteria can shift with policy changes, as evidenced by recent updates to PSLF and IDR account adjustments. Borrowers should regularly review their repayment status, respond promptly to recertification requests, and explore waivers or temporary relief programs. For example, the IDR Account Adjustment in 2023 retroactively credited borrowers for certain deferment and forbearance periods, accelerating their path to forgiveness. Practical tip: Set calendar reminders for annual recertification and monitor Federal Student Aid announcements for updates that could benefit your situation.

Stay Informed: How to Get Notified About Student Loan Forgiveness Updates

You may want to see also

Explore related products

![]()

Government Policies: Recent federal or state initiatives to forgive older student loans

Recent federal initiatives have targeted older student loans with a focus on systemic relief, particularly through the Public Service Loan Forgiveness (PSLF) program and the Fresh Start initiative. Launched in 2022, the PSLF waiver temporarily relaxed rules, allowing borrowers to count past payments that previously didn’t qualify, benefiting those in public service roles. Simultaneously, the Fresh Start initiative, part of the Biden administration’s efforts, aims to help borrowers in default by reinstating their loans in good standing and removing negative credit reporting. These policies reflect a strategic shift toward addressing long-standing debt burdens for specific demographics.

At the state level, initiatives vary but often complement federal efforts by targeting local needs. For instance, Minnesota’s Student Loan Fairness Act caps interest rates on private loans and provides tax credits for borrowers, while New York’s "Get On Your Feet" program offers up to two years of loan forgiveness for recent graduates earning below a certain threshold. Such state-specific programs demonstrate a tailored approach to alleviating student debt, often focusing on retaining young professionals and stimulating local economies.

A comparative analysis reveals that federal policies tend to prioritize broad-scale relief, while state initiatives focus on niche populations or regional economic goals. For example, federal programs like PSLF target public servants nationwide, whereas state programs like California’s Student Loan Debt Relief Tax Credit cater to residents with incomes below $200,000. Borrowers should assess eligibility for both federal and state programs to maximize benefits, as these initiatives often overlap but serve distinct purposes.

Practical steps for borrowers include reviewing loan types (federal vs. private) and payment histories to determine eligibility for forgiveness programs. For instance, those with Federal Family Education Loans (FFEL) may need to consolidate into Direct Loans to qualify for PSLF. Additionally, staying informed about application deadlines—such as the October 31, 2023, cutoff for the PSLF waiver—is critical. Borrowers should also monitor state-specific programs through official government websites or financial aid offices to avoid missing localized opportunities.

In conclusion, while federal policies provide sweeping relief mechanisms, state initiatives offer targeted solutions that address unique regional challenges. Borrowers must proactively navigate these programs, leveraging both federal and state resources to achieve meaningful debt reduction. As policies continue to evolve, staying informed and taking decisive action remains key to unlocking forgiveness for older student loans.

Paraeducators and Student Loan Forgiveness: Eligibility and Options Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness: How older loans fit into PSLF programs

Older federal student loans, particularly those issued under the Federal Family Education Loan (FFEL) program, were historically ineligible for Public Service Loan Forgiveness (PSLF). However, the U.S. Department of Education introduced the Temporary Expanded Public Service Loan Forgiveness (TEPSLF) program in 2018 to address this gap. This initiative allows borrowers with FFEL loans to consolidate them into Direct Loans, making them eligible for PSLF. To qualify, borrowers must meet all PSLF requirements, including 120 qualifying payments while working full-time for a qualifying employer. This change has been a lifeline for many public servants burdened by older loans, offering a path to forgiveness that was previously inaccessible.

For borrowers with older loans, the first step is to consolidate FFEL or Perkins Loans into the Direct Loan program. This process, known as Direct Consolidation, is free and can be completed on the Federal Student Aid website. Once consolidated, borrowers must submit the PSLF Employer Certification Form to ensure their employer qualifies for the program. It’s critical to act promptly, as the TEPSLF program has a limited funding window, and applications are processed on a first-come, first-served basis. Borrowers should also review their payment history to confirm that all payments count toward the 120 required for forgiveness.

One common pitfall for borrowers with older loans is the misconception that all payments made before consolidation count toward PSLF. In reality, only payments made *after* consolidation under the Direct Loan program qualify. This means borrowers may need to restart their payment count, which can be frustrating but is a necessary step to align with PSLF requirements. Additionally, borrowers should ensure their loans are in an income-driven repayment (IDR) plan, as this is a prerequisite for PSLF eligibility. Plans like Revised Pay As You Earn (REPAYE) or Income-Based Repayment (IBR) can lower monthly payments and make forgiveness more attainable.

A key takeaway for borrowers with older loans is the importance of proactive management. Regularly updating employment certification forms, monitoring payment counts, and staying informed about policy changes can significantly increase the chances of successful forgiveness. For example, the limited PSLF waiver, introduced in 2021, temporarily allowed past payments on FFEL and Perkins Loans to count toward PSLF without consolidation, but this opportunity expired in October 2023. Such time-sensitive programs underscore the need for vigilance and swift action. By leveraging available resources and understanding the nuances of PSLF, borrowers with older loans can navigate the system effectively and work toward a debt-free future.

Can Private Student Loans Be Forgiven? Exploring Options and Realities

You may want to see also

Explore related products

![]()

Bankruptcy Discharge: Possibility of discharging old loans through bankruptcy

Bankruptcy discharge offers a potential lifeline for those burdened by old student loans, but it’s not a guaranteed solution. Under current U.S. law, student loans are notoriously difficult to discharge in bankruptcy due to the "undue hardship" standard, which requires borrowers to prove extreme financial distress. However, recent legal shifts and evolving interpretations of this standard have opened narrow pathways for relief. For instance, the *Brunner Test*, traditionally used to assess undue hardship, is being reevaluated in some jurisdictions, with courts adopting a more borrower-friendly approach. This means that older loans, particularly those accruing interest for decades, may now face greater scrutiny in bankruptcy proceedings.

To pursue this route, borrowers must file an adversary proceeding within their bankruptcy case, specifically requesting a discharge of student loans. This involves presenting evidence of inability to maintain a minimal standard of living, a persistent financial hardship, and good-faith efforts to repay the debt. Documentation is critical—gather tax returns, bank statements, medical bills, and loan repayment histories to build a compelling case. While success rates remain low, recent cases, such as *Rosen v. National Collegiate Student Loan Trust*, demonstrate that courts are increasingly sympathetic to long-term financial struggles, especially for older borrowers.

A cautionary note: bankruptcy discharge is not a quick fix. It requires legal fees, court appearances, and a thorough understanding of the process. Additionally, not all student loans qualify; private loans may have different criteria than federal loans. Borrowers should consult an attorney specializing in student loan bankruptcy to assess their eligibility. For those with older loans, this path may be worth exploring, particularly if other forgiveness programs, like Public Service Loan Forgiveness or income-driven repayment plans, have been exhausted.

Finally, the landscape of student loan discharge in bankruptcy is evolving. Proposed legislative changes, such as the *Fresh Start Through Bankruptcy Act*, aim to simplify the process by eliminating the undue hardship requirement for student loans. While these reforms are not yet law, they signal a growing recognition of the need for relief. For now, older borrowers facing insurmountable debt should view bankruptcy discharge as a viable, albeit challenging, option—one that requires persistence, preparation, and a strategic legal approach.

Understanding Student Loan Forgiveness: How It Works and Who Qualifies

You may want to see also

Explore related products

![]()

Loan Cancellation Scams: Warnings about fraudulent schemes targeting borrowers with old debt

As the debate over student loan forgiveness continues, borrowers with old debt are increasingly vulnerable to fraudulent schemes promising quick relief. Scammers exploit confusion around government policies, preying on those desperate to shed their financial burden. These schemes often mimic official communications, using convincing language and logos to appear legitimate. Understanding the tactics of these scams is crucial for protecting yourself and your finances.

One common scam involves companies charging upfront fees to enroll borrowers in supposed loan forgiveness programs. Legitimate loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, never require payment for application or enrollment. Scammers may promise immediate cancellation or reduced payments, only to disappear with your money. Always verify the legitimacy of any service by checking with your loan servicer or the Department of Education directly.

Another red flag is unsolicited offers claiming to expedite loan forgiveness. Fraudsters often use high-pressure tactics, urging borrowers to act immediately to avoid missing out on a "limited-time opportunity." These offers may include fake testimonials or guarantees of success. Remember, genuine loan forgiveness processes take time and require documentation. If an offer seems too good to be true, it likely is.

To safeguard against these scams, follow these practical steps: first, never share personal information, such as your Federal Student Aid (FSA) ID or Social Security number, with unverified entities. Second, monitor your loan account regularly for unauthorized changes. Third, report suspicious activity to the Federal Trade Commission (FTC) and your loan servicer immediately. Staying informed and cautious is your best defense against falling victim to loan cancellation scams.

In comparison to legitimate debt relief options, fraudulent schemes lack transparency and accountability. While programs like PSLF or borrower defense to repayment require effort and patience, they offer real, long-term solutions. Scams, on the other hand, provide temporary hope but lead to financial loss and increased stress. By recognizing the signs of fraud and staying proactive, borrowers can navigate the complexities of student loan forgiveness without falling prey to deceitful practices.

Can SCOTUS Block Student Loan Forgiveness? Legal Battle Explained

You may want to see also

Frequently asked questions

No, not all old student loans are eligible for forgiveness. Eligibility depends on factors like loan type (federal or private), repayment plan, and specific forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans.

Yes, certain forgiveness programs have time limits. For example, income-driven repayment plans may forgive remaining balances after 20–25 years of qualifying payments, while PSLF requires 10 years of eligible payments.

Private student loans are generally not eligible for forgiveness programs. However, some lenders may offer settlement options or hardship programs, but these are rare and not guaranteed.

Recent government policies, such as targeted debt cancellation or expansions to existing programs, may apply to old loans. However, these initiatives are often limited to specific groups (e.g., low-income borrowers or those defrauded by schools).

Review your loan type and repayment history. Federal loan borrowers can visit the Federal Student Aid website or contact their loan servicer to explore forgiveness options like PSLF or income-driven plans. Private loan borrowers should contact their lender directly.