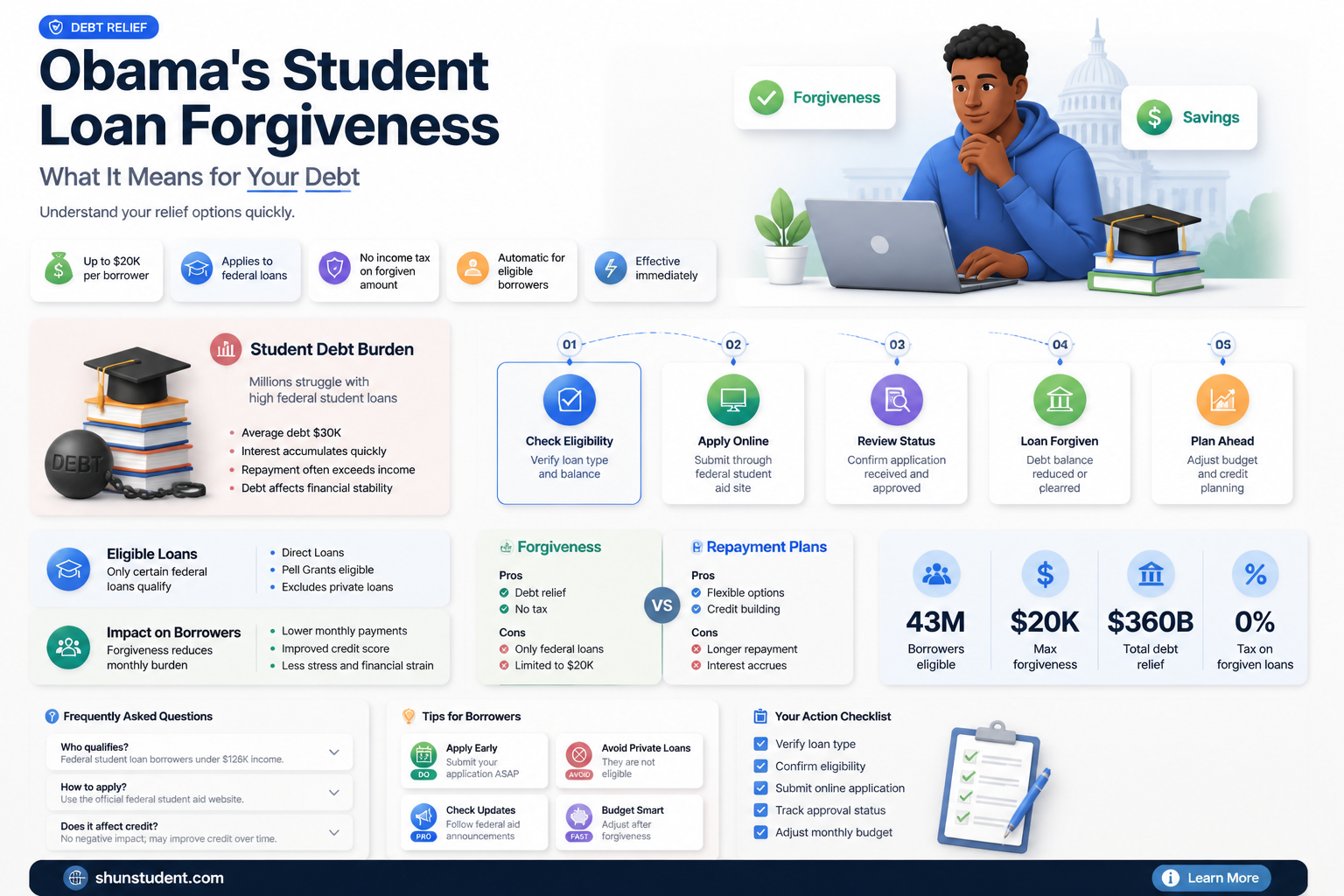

The question of whether student loans are forgiven under the Obama administration is a common concern among borrowers, stemming from policies like the Public Service Loan Forgiveness (PSLF) program and income-driven repayment (IDR) plans, which were expanded during President Obama’s tenure. While these initiatives aimed to provide relief for eligible borrowers, particularly those in public service or with high debt-to-income ratios, they do not equate to blanket forgiveness for all student loans. Borrowers must meet specific criteria, such as making consistent payments for a set period (typically 10 years) and working in qualifying public service roles. Misconceptions often arise due to the complexity of these programs, making it essential for individuals to understand their eligibility and the requirements for loan forgiveness under these Obama-era policies.

| Characteristics | Values |

|---|---|

| Program Name | Obama Student Loan Forgiveness (often refers to Income-Driven Repayment Plans and Public Service Loan Forgiveness) |

| Eligibility | Borrowers with federal student loans who meet specific criteria (e.g., income, employment in public service) |

| Loan Types Covered | Direct Loans (Federal Family Education Loan Program loans may need consolidation) |

| Forgiveness Conditions | 1. Income-Driven Repayment Plans: Forgiveness after 20-25 years of qualifying payments. 2. Public Service Loan Forgiveness (PSLF): Forgiveness after 120 qualifying payments while working full-time for a qualifying employer. |

| Income Requirements | For income-driven plans, payments are capped at a percentage of discretionary income (10-20%). |

| Employment Requirements | For PSLF, employment must be with a government or qualifying non-profit organization. |

| Tax Implications | PSLF forgiveness is tax-free; income-driven plan forgiveness may be taxable (though temporarily tax-free through 2025 under the American Rescue Plan Act). |

| Application Process | Submit an Employment Certification Form (PSLF) or enroll in an income-driven repayment plan. |

| Current Status | Active, but subject to changes in federal policy and regulations. |

| Recent Updates | Temporary waivers and expansions under the Biden administration (e.g., PSLF waiver expired Oct. 31, 2022; IDR Account Adjustment ongoing). |

| Common Misconceptions | Not all borrowers qualify; private loans are not eligible; forgiveness is not automatic. |

| Official Resources | Federal Student Aid website (studentaid.gov) for accurate and up-to-date information. |

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Forgiveness

Income-Driven Repayment (IDR) Forgiveness is a lifeline for borrowers struggling with federal student loans, offering a path to debt relief after 20 or 25 years of qualifying payments. Introduced under the Obama administration, these plans—such as Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR)—tie monthly payments to income and family size, capping them at 10–20% of discretionary income. The promise? Any remaining balance is forgiven after the repayment period, though borrowers may owe taxes on the forgiven amount.

To qualify, borrowers must first enroll in an IDR plan and maintain eligibility by recertifying income and family size annually. Payments made under these plans count toward forgiveness, even if they’re as low as $0. For example, a single borrower earning $35,000 annually with $50,000 in loans under REPAYE would pay roughly $167 monthly, with forgiveness kicking in after 240 payments (20 years). However, pitfalls exist: missing recertification deadlines or switching to a non-IDR plan can reset the payment counter, delaying forgiveness.

One critical but often overlooked detail is the tax implication of IDR forgiveness. Under current law, forgiven amounts are treated as taxable income, potentially resulting in a hefty bill. For instance, a borrower with $70,000 forgiven after 25 years could face a tax liability of $15,000–$20,000, depending on their tax bracket. To mitigate this, borrowers should plan ahead by setting aside funds or exploring temporary tax relief programs like the American Rescue Plan Act, which exempts student loan forgiveness from taxation through 2025.

Comparatively, IDR Forgiveness stands out from other relief programs like Public Service Loan Forgiveness (PSLF), which requires 10 years of payments and full-time public service employment. IDR is more accessible but demands a longer commitment. Borrowers must weigh their career trajectory, income stability, and tolerance for long-term debt management. For those with low incomes or high balances, IDR often provides the most realistic route to eventual forgiveness, despite its complexities.

Practical tips for maximizing IDR Forgiveness include consolidating FFEL or Perkins Loans into a Direct Consolidation Loan to make them eligible, tracking payments meticulously, and staying informed about policy changes. For instance, the Biden administration’s recent IDR Account Adjustment allows the Department of Education to retroactively count previously ineligible payments toward forgiveness—a game-changer for long-term borrowers. By proactively managing their loans and leveraging available tools, borrowers can turn IDR Forgiveness from a distant hope into a tangible reality.

Can AES Student Loans Qualify for Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF)

To qualify for PSLF, borrowers must meet three key criteria: work full-time for a qualifying employer, make 120 payments under an income-driven repayment plan, and have eligible federal Direct Loans. "Full-time" typically means 30 hours per week or the employer’s definition of full-time, whichever is greater. Qualifying employers include federal, state, local, or tribal government agencies, 501(c)(3) non-profits, and some other non-profits providing public services. Payments must be made on time and in full, and only Direct Loans—not FFEL or Perkins Loans—are eligible, though consolidation into a Direct Loan can make previously ineligible loans qualify. This specificity underscores the importance of meticulous planning and documentation.

One of the most common pitfalls borrowers face is misunderstanding the repayment plan requirement. Only payments made under an income-driven repayment plan (IDR)—such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE)—count toward PSLF. Standard 10-year repayment plans, for instance, do not qualify, even if payments are made on time. Borrowers should submit an Employment Certification Form (ECF) annually or when changing employers to ensure their payments are tracking correctly. This proactive approach helps identify and correct errors early, preventing disqualification later.

PSLF is particularly beneficial for borrowers with high debt-to-income ratios, such as those in social work, teaching, or public health. For example, a teacher earning $45,000 annually with $100,000 in student loans could see monthly payments as low as $200 under an IDR plan. After 10 years of qualifying payments, the remaining balance—potentially $80,000 or more—would be forgiven tax-free. However, this outcome hinges on strict adherence to program rules, making it essential to stay informed and organized. The Temporary Expanded Public Service Loan Forgiveness (TEPSLF) initiative, introduced in 2018, offers a safety net for those who made payments under the wrong plan but meets other PSLF criteria.

In conclusion, PSLF is a powerful tool for public service workers burdened by student debt, but its complexity demands careful navigation. Borrowers should consolidate ineligible loans, enroll in an IDR plan, and certify their employment regularly. While the program’s requirements are strict, the potential for significant debt relief makes it a worthwhile pursuit for those committed to qualifying careers. By understanding and adhering to its rules, borrowers can turn PSLF from a bureaucratic hurdle into a lifeline for financial stability.

Student Loan Forgiveness and Taxes: What You Need to Report

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Program

Teachers, especially those in low-income schools, face unique financial challenges. The Teacher Loan Forgiveness Program, established under the Obama administration, offers a lifeline by forgiving up to $17,500 in federal Direct or FFEL Program loans for eligible educators. This program specifically targets teachers who commit to serving full-time for five consecutive years in schools designated as low-income by the Department of Education. To qualify, teachers must also meet specific criteria, such as having a bachelor’s degree, state certification, and teaching in a high-need subject area like math, science, or special education.

To maximize the benefits of this program, teachers should first verify their school’s eligibility using the Department of Education’s directory of low-income schools. Next, ensure your loans are part of the Direct Loan or FFEL Program, as private loans are ineligible. After completing the five-year service requirement, submit the Teacher Loan Forgiveness Application to your loan servicer. Keep detailed records of your employment and teaching assignments, as these will be required to prove eligibility. For those teaching in secondary schools, the forgiveness amount caps at $17,500, while elementary teachers can receive up to $5,000.

A common misconception is that all teachers automatically qualify for loan forgiveness. However, the program’s strict criteria mean not every educator will benefit. For instance, teachers in private schools or those who don’t meet the full-time requirement are ineligible. Additionally, the program does not cover PLUS loans or Perkins loans. Teachers should also be aware that forgiven amounts may be considered taxable income, depending on their financial situation. Consulting a tax professional can help mitigate potential tax liabilities.

Compared to other forgiveness programs like Public Service Loan Forgiveness (PSLF), the Teacher Loan Forgiveness Program offers a faster path to relief but with a lower maximum forgiveness amount. While PSLF requires 10 years of service and forgives the entire remaining balance, the teacher-specific program is ideal for educators seeking quicker, partial relief. Combining both programs strategically—for example, pursuing Teacher Loan Forgiveness first and then PSLF—can maximize overall savings. Ultimately, this program is a powerful tool for educators committed to serving in underserved communities, offering both financial relief and a meaningful career path.

Apply for $10,000 Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Obama’s Pay As You Earn (PAYE)

During his presidency, Barack Obama introduced several initiatives to address the growing student loan crisis, one of which was the Pay As You Earn (PAYE) repayment plan. Launched in 2012, PAYE was designed to make federal student loan payments more manageable for borrowers by capping monthly payments at 10% of their discretionary income. This plan was particularly aimed at low- and middle-income earners struggling under the weight of substantial student debt. Unlike standard repayment plans, which often require fixed monthly payments regardless of income, PAYE adjusts based on earnings, offering immediate relief to those with limited financial means.

To qualify for PAYE, borrowers must have taken out their first federal student loan after October 1, 2007, and received a direct loan disbursement after October 1, 2011. Additionally, borrowers must demonstrate partial financial hardship, meaning their monthly payment under a standard 10-year repayment plan would exceed what they would pay under PAYE. For example, a single borrower earning $30,000 annually with $50,000 in student loans would see their monthly payment drop from approximately $500 under a standard plan to around $150 under PAYE. This reduction can significantly ease financial strain, allowing borrowers to allocate funds to other essential expenses like rent, groceries, or savings.

One of the most appealing aspects of PAYE is its forgiveness component. After making 20 years of qualifying payments, any remaining balance on the loan is forgiven. For graduate school borrowers, the forgiveness period extends to 25 years. While this may seem like a long commitment, the reduced monthly payments make it a viable option for those with long-term financial challenges. However, it’s important to note that forgiven amounts may be considered taxable income, so borrowers should plan accordingly. For instance, a borrower with $100,000 in debt could save tens of thousands of dollars over two decades by choosing PAYE over a standard repayment plan.

Critics argue that PAYE and similar income-driven plans create a moral hazard by encouraging borrowers to take on more debt than they can afford, expecting eventual forgiveness. However, this perspective overlooks the systemic issues driving the student loan crisis, such as skyrocketing tuition costs and limited financial literacy among young borrowers. PAYE serves as a practical solution within the current framework, providing relief to millions while policymakers address root causes. Borrowers considering PAYE should weigh the long-term benefits against potential tax implications and consult resources like the Federal Student Aid website to determine eligibility and calculate estimated payments.

In practice, PAYE has been a lifeline for many, but it’s not a one-size-fits-all solution. Borrowers with high incomes or those nearing the end of their repayment term may find other plans more advantageous. For example, a borrower earning $80,000 annually might discover that their PAYE payment is only slightly lower than a standard plan, making the extended repayment period less appealing. To maximize benefits, borrowers should annually recertify their income and family size, as changes in financial circumstances can adjust their monthly payment. Ultimately, PAYE represents a critical tool in Obama’s efforts to address student debt, offering flexibility and hope to borrowers navigating an increasingly complex financial landscape.

Navigating Student Loan Forgiveness: Key Contacts for Debt Relief

You may want to see also

Explore related products

![]()

Loan Forgiveness for Closed Schools

Students who attended schools that closed while they were enrolled or shortly after they withdrew may qualify for loan forgiveness under the Closed School Discharge program. This federal initiative, part of the broader Obama-era efforts to address student debt, offers a lifeline to borrowers left in limbo by institutional failures. To apply, borrowers must meet specific criteria: the school must have closed while the student was enrolled or within 120 days of their withdrawal, and the borrower must not have transferred credits to another institution. Documentation, such as transcripts or withdrawal notices, is critical to proving eligibility.

Consider the case of ITT Technical Institute, which closed in 2016, leaving thousands of students stranded. Many former ITT students successfully applied for Closed School Discharge, erasing their federal loans entirely. This example highlights the program’s potential but also underscores the need for proactive borrower action. Applications must be submitted to the loan servicer, and approval is not automatic. Borrowers should avoid pitfalls like continuing their education at a comparable institution, which can disqualify them from this relief.

Persuasively, the Closed School Discharge program is one of the most straightforward paths to loan forgiveness, yet it remains underutilized due to lack of awareness. Borrowers often mistakenly assume they must repay loans even when their school has closed, or they fear the process is overly complex. In reality, the application is relatively simple, requiring only a form and supporting documents. Advocacy groups and legal aid organizations can assist borrowers in navigating the process, ensuring they receive the relief they’re entitled to.

Comparatively, while other forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans require years of payments or specific employment, Closed School Discharge offers immediate relief without such conditions. However, it’s limited to those directly affected by school closures, making it a niche solution. Borrowers ineligible for this program may explore other options, such as Borrower Defense to Repayment, which applies if the school misled students. Understanding these distinctions is key to maximizing available relief.

Practically, borrowers should take immediate steps if their school closes. First, confirm eligibility by checking the Department of Education’s list of closed schools. Next, gather all relevant documents, including enrollment records and communication from the school. Finally, submit the discharge application to the loan servicer promptly, as delays can complicate the process. For those unsure of their eligibility or facing resistance from servicers, consulting with a student loan attorney or nonprofit counselor can provide clarity and support. This proactive approach ensures borrowers don’t miss out on a critical opportunity to eliminate their debt.

Student Loan Pause: Does It Accelerate Your Path to Forgiveness?

You may want to see also

Frequently asked questions

The term "Obama Student Loan Forgiveness" often refers to the Pay As You Earn (PAYE) repayment plan introduced under President Obama in 2012. It caps monthly payments at 10% of discretionary income and offers forgiveness after 20 years of qualifying payments.

Borrowers with federal Direct Loans who demonstrate partial financial hardship and enroll in an income-driven repayment plan, such as PAYE, may qualify. Loans must have been disbursed after October 1, 2007, and before October 1, 2011, for PAYE eligibility.

No, only federal student loans under specific income-driven repayment plans, such as PAYE, qualify for forgiveness after 20 years. Private loans and certain federal loans (e.g., FFEL or Perkins loans not consolidated into Direct Loans) are not eligible.

To apply, submit an income-driven repayment plan application through your loan servicer. Ensure your loans are eligible (Direct Loans) and provide proof of income. Stay enrolled in the plan and make qualifying payments for 20 years to be considered for forgiveness.