When considering the impact of refinancing student loans, one critical question arises: are refinanced student loans still forgivable in the event of the borrower’s death? Unlike federal student loans, which typically offer death discharge, meaning the debt is forgiven if the borrower passes away, private refinanced loans often lack this protection. Private lenders are not required by law to forgive the debt, and their policies vary widely. Some may offer death discharge as a feature, but it’s not guaranteed. Borrowers must carefully review the terms of their refinanced loan agreement to understand their obligations and potential risks. This distinction highlights the importance of weighing the benefits of lower interest rates or better terms against the loss of federal protections like death discharge when refinancing student loans.

| Characteristics | Values |

|---|---|

| Federal Student Loans | Generally discharged upon borrower's death (no repayment required by estate or family). |

| Private Student Loans | Typically not discharged upon death; may require repayment from estate or co-signer. |

| Refinanced Federal Loans (Private Lender) | Lose federal benefits, including death discharge; repayment may be required from estate. |

| Refinanced Private Loans (Private Lender) | No change in terms; repayment typically required from estate or co-signer. |

| Co-Signer Liability | Co-signers may still be responsible for repayment after borrower's death (private loans). |

| Estate Responsibility | Estate may be required to repay refinanced loans, depending on lender terms. |

| State Laws | Some states have laws limiting estate recovery for student loans. |

| Lender Policies | Policies vary; some private lenders may offer death discharge as a benefit. |

| Life Insurance Policies | Some borrowers purchase life insurance to cover loan repayment in case of death. |

| Latest Data (as of 2023) | No federal protections for refinanced loans; private lenders dictate terms. |

Explore related products

What You'll Learn

- Refinanced vs. Federal Loans: Compare forgiveness policies for refinanced and federal student loans upon borrower's death

- Lender-Specific Policies: Explore how private lenders handle loan forgiveness in case of death

- Co-Signer Responsibility: Determine if co-signers remain liable after borrower's death

- State Laws Impact: Investigate how state laws affect forgiveness of refinanced student loans

- Insurance Options: Examine life insurance policies that cover refinanced student loans upon death

![]()

Refinanced vs. Federal Loans: Compare forgiveness policies for refinanced and federal student loans upon borrower's death

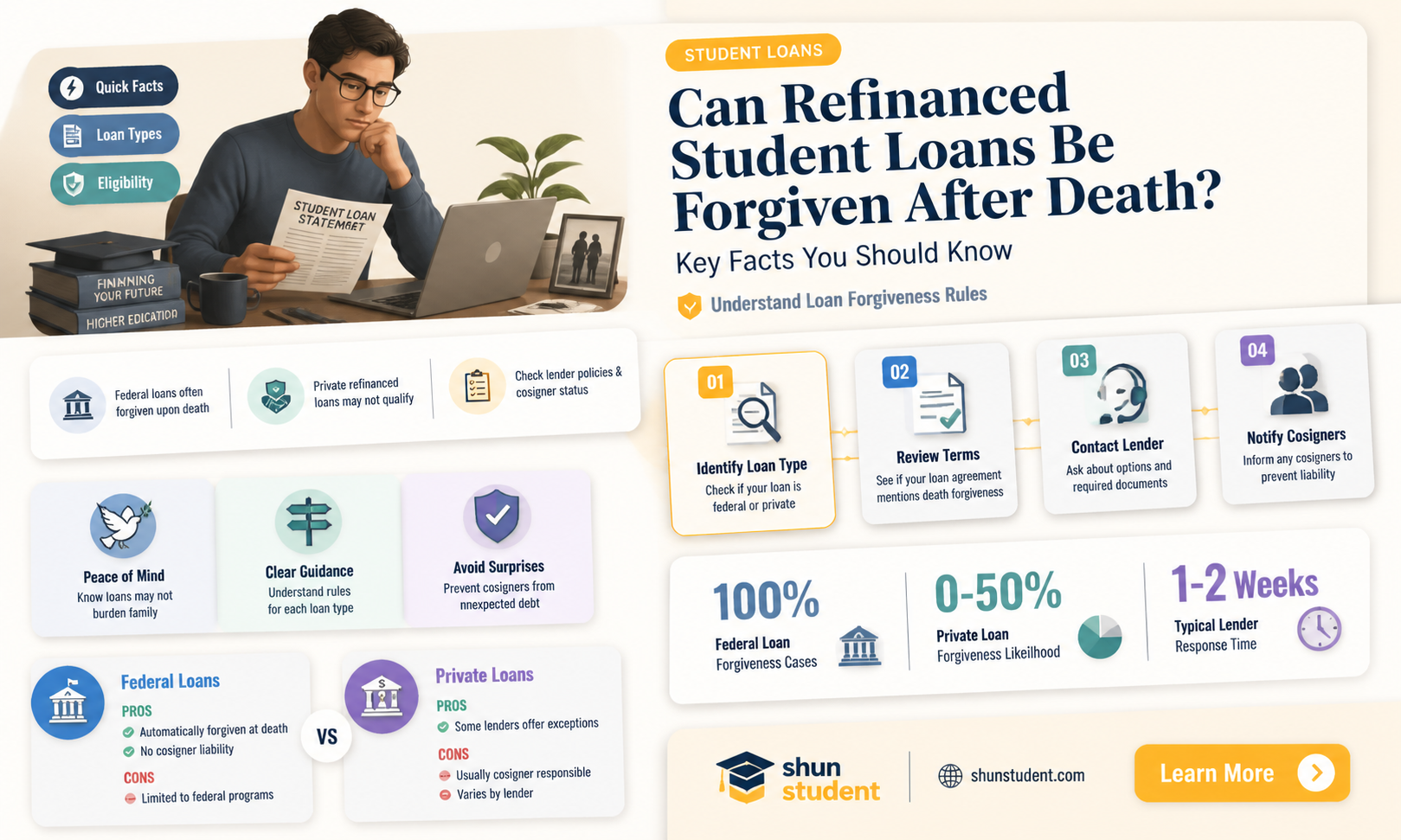

Upon a borrower's death, federal student loans are automatically discharged, offering a crucial safety net for families. This policy, governed by the Department of Education, ensures that surviving relatives are not burdened with the deceased’s educational debt. For example, Direct Loans, Federal Family Education Loans (FFEL), and Perkins Loans qualify for this forgiveness. Lenders require a certified death certificate to initiate the discharge process, which typically takes 12 weeks. This federal protection is a significant benefit, particularly for borrowers with substantial loan balances or those in precarious financial situations.

Refinanced student loans, however, operate under a vastly different framework. When borrowers refinance with private lenders, they often lose access to federal protections, including death discharge. Most private lenders do not forgive the remaining balance upon the borrower’s death, instead holding co-signers or the borrower’s estate liable. For instance, SoFi and Earnest, popular refinancing companies, explicitly state in their terms that the loan becomes the responsibility of the estate or co-signer. This lack of forgiveness can lead to unexpected financial strain for grieving families, particularly if the estate’s assets are insufficient to cover the debt.

A critical distinction lies in the treatment of co-signers. Federal loans discharge the debt entirely upon the borrower’s death, protecting co-signers from liability. In contrast, refinanced loans often require co-signers to assume responsibility for the remaining balance. This disparity underscores the importance of understanding loan terms before refinancing. For example, a parent co-signing a refinanced loan could face repayment obligations, even if the primary borrower passes away. Such scenarios highlight the trade-off between lower interest rates through refinancing and the loss of federal safeguards.

Borrowers considering refinancing should weigh these risks carefully. While refinancing can reduce monthly payments or interest rates, it may not be worth sacrificing the death discharge benefit. Practical steps include reviewing lender policies, consulting financial advisors, and exploring alternatives like life insurance to cover potential liabilities. For instance, a $100,000 life insurance policy could offset the risk of leaving a co-signer or estate liable for refinanced debt. Ultimately, the decision hinges on individual financial circumstances and the value placed on federal protections versus refinancing advantages.

Consolidate Student Loans and Unlock Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Lender-Specific Policies: Explore how private lenders handle loan forgiveness in case of death

Private lenders’ policies on loan forgiveness in the event of a borrower’s death vary widely, making it essential to scrutinize the fine print before refinancing student loans. Unlike federal loans, which are automatically discharged upon the borrower’s death, private lenders are not legally obligated to forgive the debt. However, some lenders, such as SoFi and CommonBond, have adopted borrower-friendly policies that include death discharge as a standard feature. Others may require proof of death, such as a death certificate, and may even assess the estate’s ability to repay before making a decision. This disparity underscores the importance of comparing lenders’ terms during the refinancing process.

For borrowers considering refinancing, the first step is to request explicit documentation from potential lenders regarding their death discharge policies. Phrases like *“loans are discharged upon the borrower’s death”* or *“no further payments required”* should be sought in writing. Avoid lenders that use ambiguous language or fail to address this scenario altogether. Additionally, inquire about any conditions tied to forgiveness, such as exclusions for cosigners or limitations based on the cause of death. A proactive approach ensures that both the borrower and their loved ones are protected from unexpected financial burdens.

A comparative analysis of lender policies reveals distinct tiers of borrower protection. Tier-one lenders, such as Laurel Road and Earnest, not only discharge the loan but also waive any associated fees or penalties. Tier-two lenders may forgive the debt but leave cosigners liable, as seen with some regional banks. Tier-three lenders, often smaller institutions or those with less competitive offerings, may deny forgiveness altogether or require repayment from the estate. Understanding these tiers allows borrowers to align their refinancing decision with their long-term financial security and personal values.

Practical tips for navigating this landscape include involving a financial advisor or estate planner to assess the implications of refinancing on your overall financial plan. If a cosigner is involved, discuss the potential risks and explore alternatives like cosigner release programs offered by some lenders. Finally, consider purchasing a small life insurance policy to cover the loan balance, particularly if the lender’s forgiveness policy is unclear or inadequate. While this adds a cost, it provides peace of mind and ensures that your loved ones are not left with a financial burden in the event of your passing.

Navient Student Loan Forgiveness: Eligibility Criteria and Application Guide

You may want to see also

Explore related products

![]()

Co-Signer Responsibility: Determine if co-signers remain liable after borrower's death

Co-signers often step in to help borrowers secure student loans, but their liability doesn’t always end when the borrower passes away. Federal student loans typically offer death discharge, meaning the debt is forgiven upon the borrower’s death. However, refinanced student loans, which are private, operate under different rules. Most private lenders do not automatically discharge the debt, leaving co-signers on the hook for repayment. This stark contrast highlights the importance of understanding the terms of refinanced loans before committing as a co-signer.

To determine co-signer liability after a borrower’s death, start by reviewing the loan agreement. Look for clauses related to death discharge or co-signer release. Some private lenders, like SoFi and Laurel Road, offer death discharge policies, but these are the exception rather than the rule. If the agreement lacks such provisions, co-signers remain legally responsible for the debt. This responsibility can extend to spouses, parents, or other relatives who co-signed, potentially impacting their financial stability during an already difficult time.

One practical step co-signers can take is to purchase a life insurance policy for the borrower, ensuring the debt can be covered in the event of death. Another option is to explore co-signer release programs, though these are rarely available for refinanced student loans. If the borrower dies without such protections, co-signers should contact the lender immediately to discuss options, such as negotiating a settlement or seeking legal advice. Proactive measures can mitigate financial risk, but the ultimate takeaway is clear: co-signing a refinanced student loan is a long-term commitment that outlives the borrower.

Comparatively, federal loans offer a safety net that private refinanced loans do not. For instance, Parent PLUS loans and Direct Loans are forgiven upon the borrower’s death, shielding co-signers from liability. Refinanced loans, however, prioritize lender protection over borrower or co-signer relief. This disparity underscores the need for borrowers and co-signers to weigh the benefits of lower interest rates against the loss of federal protections. Before refinancing, consider whether the savings justify the increased risk for co-signers.

In conclusion, co-signers of refinanced student loans must recognize their potential lifelong liability. Unlike federal loans, most private refinanced loans do not offer death discharge, leaving co-signers responsible for the debt. To protect themselves, co-signers should scrutinize loan agreements, explore insurance options, and understand the risks involved. While refinancing can provide financial benefits, it comes with significant trade-offs that demand careful consideration.

Pell Grants and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

State Laws Impact: Investigate how state laws affect forgiveness of refinanced student loans

State laws wield significant influence over the fate of refinanced student loans in the event of a borrower's death, creating a patchwork of outcomes that defy generalization. While federal student loans typically offer automatic discharge upon the borrower's death, refinanced loans—which are private—are subject to the terms of the new loan agreement and the laws of the state where the contract is enforced. This variability means that a borrower’s estate or cosigner could still be on the hook for the debt, depending on jurisdiction. For instance, some states prohibit lenders from collecting on student loans after the borrower’s death, while others allow it, leaving survivors vulnerable to debt collection efforts.

Consider the example of Washington State, which enacted a law in 2019 requiring private student loan lenders to discharge debt upon the borrower’s death or permanent disability. This contrasts sharply with states like Texas, where no such protections exist, and lenders can pursue repayment from the borrower’s estate or cosigners. Such disparities underscore the importance of understanding state-specific laws before refinancing. Borrowers in states without protective legislation may want to explore life insurance policies or loan agreements with death discharge clauses to safeguard their loved ones.

Analyzing these differences reveals a critical takeaway: refinancing student loans can inadvertently strip away federal protections, including death discharge, but state laws may step in to fill the gap—or leave a void. Borrowers must scrutinize both the loan agreement and their state’s legal framework to assess risk. For instance, if a borrower in a state without protections refinances a federal loan, they effectively trade forgiveness for potentially lower interest rates, a decision that could burden their family posthumously.

To navigate this complexity, borrowers should take proactive steps. First, consult a financial advisor or attorney to evaluate state laws and loan terms. Second, consider adding a death discharge clause to the refinancing agreement, though this may increase costs. Third, explore state-specific resources, such as New York’s Student Loan Bill of Rights, which mandates clear disclosures about refinancing risks. Finally, weigh the long-term implications of refinancing against the immediate financial benefits, especially if living in a state with limited protections.

In conclusion, state laws act as a double-edged sword in the realm of refinanced student loans and death forgiveness. While some states offer robust protections, others leave borrowers and their families exposed. By understanding these nuances, borrowers can make informed decisions that balance financial relief with long-term security, ensuring their legacy isn’t burdened by avoidable debt.

VA Disability Benefits: Student Loan Deferment Options for 50% Rating

You may want to see also

![]()

Insurance Options: Examine life insurance policies that cover refinanced student loans upon death

Refinanced student loans often complicate the forgiveness landscape, especially in the event of death. Unlike federal loans, which typically offer discharge upon the borrower’s passing, private refinanced loans lack standardized protections. This gap creates a financial risk for cosigners, spouses, or estates, as the debt may persist. Life insurance emerges as a strategic solution, but not all policies are created equal. To effectively shield refinanced student loans, policyholders must tailor coverage to the loan’s specifics, ensuring the death benefit matches the outstanding balance and terms.

When selecting a life insurance policy for this purpose, start by assessing the loan’s current and projected balance. Term life insurance is often ideal due to its affordability and customizable term lengths. For instance, if a borrower refinanced a $50,000 loan with a 10-year repayment plan, a 10-year term policy with a $50,000 death benefit would suffice. However, if the loan term exceeds the policy term, the coverage could lapse, leaving beneficiaries vulnerable. Permanent life insurance, such as whole life, offers lifelong coverage but at a higher cost, making it suitable for those with long-term financial obligations or additional estate planning needs.

Policy riders can enhance protection for refinanced student loans. An accelerated death benefit rider, for example, allows the insured to access a portion of the death benefit if diagnosed with a terminal illness, providing funds to pay off the loan early. Similarly, a waiver of premium rider ensures premiums are forgiven if the insured becomes disabled, keeping the policy active without financial strain. These add-ons, while increasing premiums slightly, offer critical flexibility and peace of mind.

A common oversight is failing to update beneficiaries or policy details after refinancing. If a borrower refinances a loan but neglects to adjust the insurance coverage, the death benefit might fall short of the new balance. Regular reviews—annually or after significant financial changes—are essential. Additionally, transparency with beneficiaries about the policy’s purpose ensures they know to use the payout for the loan, preventing unintended use of funds.

Finally, compare policies from multiple insurers to find the best fit. Premiums vary based on age, health, and coverage amount, so obtaining quotes from at least three providers is advisable. Online calculators can estimate costs, but consulting an insurance agent or financial advisor ensures alignment with long-term goals. By proactively addressing this niche need, borrowers can safeguard their loved ones from the burden of refinanced student debt, even in the worst-case scenario.

Student Loan Forgiveness: How Many Borrowers Have Benefited So Far?

You may want to see also

Frequently asked questions

It depends on the type of loan and the refinancing terms. Federal student loans are typically discharged upon the borrower's death, but refinancing federal loans into private loans often removes this benefit. Private refinanced loans may or may not offer death discharge, depending on the lender's policies.

No, refinancing federal student loans into private loans usually eliminates the death discharge benefit. Federal loans are automatically forgiven upon the borrower's death, but private refinanced loans are subject to the lender's terms, which often do not include automatic forgiveness.

Some private lenders offer death discharge as a feature, but it’s not guaranteed. You’ll need to check the specific terms of your refinanced loan agreement. If the lender does not include this benefit, the loan may become the responsibility of your estate or cosigner (if applicable) after your death.