Student loan forgiveness has become a pressing concern for millions of borrowers, with many wondering if relief is automatic or requires specific actions. While certain programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, offer pathways to forgiveness after meeting eligibility criteria, they are not automatic. Borrowers must actively apply for these programs, ensure their loans qualify, and maintain compliance with program requirements. Additionally, recent initiatives like the one-time student loan forgiveness plan announced by the Biden administration in 2022 required borrowers to submit applications, further emphasizing that forgiveness is not granted without proactive steps. Understanding the nuances of these programs is crucial for borrowers seeking relief from their student loan debt.

Explore related products

What You'll Learn

![]()

Eligibility criteria for automatic loan forgiveness

Automatic student loan forgiveness isn’t a universal gift; it’s a targeted remedy tied to specific eligibility criteria. One key pathway is through Public Service Loan Forgiveness (PSLF), which requires 120 qualifying payments while working full-time for a government or nonprofit organization. Unlike manual applications for other forgiveness programs, PSLF can trigger automatic forgiveness if your employment certification history is complete and accurate. However, "automatic" here means the system recognizes your eligibility after 120 payments—it doesn’t waive the need for consistent documentation and proper loan type (Direct Loans only).

Another automatic forgiveness mechanism is tied to income-driven repayment (IDR) plans, which cap monthly payments based on income and family size. After 20–25 years of qualifying payments, the remaining balance is forgiven. While this process is technically automatic, borrowers must annually recertify their income and family size to stay eligible. Missed recertifications can reset the payment count, delaying forgiveness. For example, a borrower earning $40,000 with $100,000 in loans might pay as little as $100/month under an IDR plan, but only if they consistently update their financial details.

Disability discharge offers a more immediate form of automatic forgiveness for borrowers with permanent disabilities. The Department of Education matches loan holders against Social Security Administration data to identify eligible individuals, eliminating the need for a manual application in some cases. However, borrowers must still provide documentation if they don’t automatically qualify through data matching. This process underscores the importance of keeping contact information updated with loan servicers to ensure seamless notification.

Lastly, school closure discharges automatically forgive loans for students whose institutions shut down while they were enrolled or shortly after withdrawal. For instance, students of ITT Tech or Corinthian Colleges received automatic discharges without applying. Yet, this criterion is narrowly defined: borrowers must have been actively enrolled or withdrawn within 120–180 days of closure, depending on the program. Those who transferred credits or completed their program elsewhere may not qualify, highlighting the need to understand the fine print of automatic eligibility.

In summary, automatic loan forgiveness isn’t random—it’s a structured process tied to specific criteria like employment, repayment plans, disability status, or school closures. Borrowers must proactively meet documentation and eligibility requirements to benefit. While the system can recognize and process forgiveness without a formal application, staying informed and compliant is crucial to avoid pitfalls that could disqualify you from these programs.

Forgiving Student Loans: Economic Impact and Long-Term Consequences Explored

You may want to see also

Explore related products

![]()

Income-driven repayment plan requirements

Income-driven repayment (IDR) plans are not a one-size-fits-all solution, and understanding their requirements is crucial for borrowers seeking manageable student loan payments. These plans, which include options like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE), adjust monthly payments based on income and family size. To qualify, borrowers must demonstrate partial financial hardship, meaning their federal student loan debt is disproportionately high relative to their income. This assessment is not automatic; borrowers must actively apply for an IDR plan and recertify their income and family size annually to maintain eligibility.

The application process for IDR plans involves submitting documentation to prove income, such as tax returns or pay stubs. Borrowers can apply through their loan servicer’s website or by submitting a paper form. Once enrolled, payments are recalculated each year based on updated financial information. For example, a single borrower earning $40,000 annually with $50,000 in student loans might see their monthly payment drop from $500 under the Standard Repayment Plan to $200 under REPAYE. However, missing the annual recertification deadline can result in a return to the Standard Repayment Plan, often with a significantly higher monthly payment.

One critical aspect of IDR plans is their pathway to loan forgiveness. After 20 or 25 years of qualifying payments (depending on the plan), any remaining balance is forgiven. However, this forgiveness is not automatic; borrowers must remain in an IDR plan and make consistent, on-time payments throughout the required period. Additionally, forgiven amounts may be considered taxable income, though current legislation (as of 2023) provides temporary tax-free treatment for forgiven balances under certain conditions.

Borrowers should also be aware of the trade-offs. While IDR plans reduce monthly payments, they often extend the repayment period, resulting in more interest paid over time. For instance, a borrower with $100,000 in loans at 6% interest might pay $70,000 in interest over 25 years under REPAYE, compared to $30,000 over 10 years under the Standard Plan. To mitigate this, borrowers can make extra payments toward the principal, which reduces overall interest costs without penalty.

In summary, IDR plans offer a lifeline for borrowers struggling with student loan debt, but they require proactive management. By understanding the application process, recertification requirements, and long-term implications, borrowers can leverage these plans effectively to achieve financial stability and eventual loan forgiveness.

Does Trump's Student Loan Forgiveness Include Spouses? Key Details Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) process

The Public Service Loan Forgiveness (PSLF) program is not automatic; it requires deliberate action and adherence to specific criteria. Unlike some forgiveness programs that might trigger after a set number of payments, PSLF demands borrowers to actively apply after meeting all requirements. This process ensures accountability and verifies that applicants have fulfilled their commitment to public service.

To qualify for PSLF, borrowers must make 120 eligible payments while working full-time for a qualifying employer. These payments must be made under an income-driven repayment plan, which adjusts monthly payments based on income and family size. For example, a borrower earning $40,000 annually with $50,000 in loans might pay as little as $150 per month under the Pay As You Earn (PAYE) plan. Tracking these payments is crucial, as errors in payment counts are common and can delay forgiveness.

One of the most challenging aspects of PSLF is determining employer eligibility. Qualifying employers include government organizations at any level, 501(c)(3) nonprofit organizations, and some other types of nonprofits that provide public services. For instance, a teacher working at a public school or a nurse at a nonprofit hospital would meet this criterion. However, private companies, even those with public service missions, typically do not qualify. Borrowers should use the Department of Education’s Employer Certification Form annually to confirm their employer’s eligibility and track their progress.

After making 120 eligible payments, borrowers must submit a PSLF application to receive forgiveness. This step is often overlooked, as some assume forgiveness is automatic upon reaching the payment threshold. The application requires documentation of employment and payment history, making it essential to maintain thorough records. Approval rates for PSLF have historically been low due to administrative errors, such as incorrect payment counts or ineligible repayment plans. To avoid pitfalls, borrowers should consult resources like the Federal Student Aid website or seek guidance from loan servicers specializing in PSLF.

In summary, the PSLF process is a structured but not automatic pathway to loan forgiveness. Success hinges on understanding eligibility criteria, maintaining accurate records, and actively applying after meeting requirements. By taking proactive steps, borrowers can navigate this complex program and achieve debt relief for their commitment to public service.

Understanding Student Loan Forgiveness: A Comprehensive Guide to Debt Relief

You may want to see also

Explore related products

![]()

Employer certification for forgiveness programs

Employer certification is a critical step for borrowers seeking loan forgiveness through programs like Public Service Loan Forgiveness (PSLF) or employer-based repayment assistance. Unlike automatic forgiveness, which doesn’t exist for most federal or private loans, employer certification requires active participation from both the borrower and their workplace. This process verifies that the borrower’s employment qualifies them for forgiveness under specific criteria, such as working full-time for a government or nonprofit organization. Without this certification, borrowers risk disqualification, even if they meet all other program requirements.

To initiate employer certification, borrowers must complete and submit the Employment Certification Form (ECF) provided by the U.S. Department of Education. This form requires details about the employer, the borrower’s role, and their employment dates. Employers must sign and return the form, confirming the borrower’s eligibility. For PSLF, submitting this form annually or when switching jobs is recommended, as it tracks qualifying payments and ensures borrowers stay on track. Failure to obtain certification can lead to delays or denials in forgiveness applications, making timely submission essential.

One common challenge in employer certification is navigating the complexities of qualifying employers. For instance, not all nonprofits are eligible under PSLF; only those classified as 501(c)(3) organizations qualify. Similarly, government positions at the federal, state, or local level are eligible, but political appointments or partisan roles may not be. Borrowers must carefully review their employer’s status and consult resources like the PSLF Help Tool to confirm eligibility before submitting the ECF. Missteps here can render years of payments ineligible for forgiveness.

Employers also play a proactive role in facilitating certification. Some organizations, particularly large nonprofits or government agencies, have dedicated HR staff to assist with PSLF documentation. Borrowers should inquire about such support and leverage it to streamline the process. Additionally, employers can benefit from helping employees pursue forgiveness, as it enhances job satisfaction and retention. For example, offering workshops on loan forgiveness or providing pre-filled ECFs can reduce administrative burdens for both parties.

In conclusion, employer certification is far from automatic but is a manageable process with proper preparation. Borrowers should familiarize themselves with program requirements, maintain open communication with their employers, and submit certifications regularly. Employers, meanwhile, can support their staff by providing resources and guidance. By working together, both parties can ensure borrowers maximize their chances of achieving loan forgiveness, turning a complex process into a collaborative success.

Medical Student Loan Forgiveness: How Many Apply for Relief?

You may want to see also

Explore related products

![]()

Loan servicer role in automatic forgiveness

Loan servicers play a pivotal role in the automatic forgiveness process for student loans, acting as the intermediary between borrowers and the Department of Education. Their responsibilities include tracking qualifying payments, maintaining accurate records, and applying forgiveness once eligibility criteria are met. For instance, under the Public Service Loan Forgiveness (PSLF) program, servicers must verify employment certifications and count payments toward the required 120-month threshold. Without their diligence, borrowers risk delays or denials in forgiveness, even if they meet all program requirements.

Consider the steps servicers take to facilitate automatic forgiveness. First, they enroll borrowers in income-driven repayment (IDR) plans, which are often pathways to forgiveness after 20–25 years of qualifying payments. Second, they monitor payment histories to ensure each payment counts toward forgiveness. For example, a borrower on the Revised Pay As You Earn (REPAYE) plan must make 240–300 monthly payments, depending on loan type. Servicers must accurately track these payments, adjusting for periods of economic hardship or forbearance that may not qualify. Missteps here can reset the forgiveness clock, costing borrowers years of progress.

However, servicers’ roles are not without challenges. The complexity of forgiveness programs, coupled with high caseloads, can lead to errors. For instance, a 2021 audit revealed that some servicers miscalculated payment counts for IDR forgiveness, leaving borrowers unaware of their progress. To mitigate this, borrowers should proactively request annual payment counts and cross-reference them with their records. Additionally, servicers are required to notify borrowers when they reach forgiveness milestones, but these communications are often overlooked or misunderstood. Borrowers must stay vigilant, treating servicers as partners rather than sole guardians of their forgiveness journey.

A comparative analysis highlights the disparity in servicer performance. Some, like MOHELA (the designated PSLF servicer), have streamlined processes for handling employment certifications and payment tracking. Others struggle with outdated systems and training gaps, leading to inconsistencies. Borrowers can advocate for themselves by consolidating loans with high-performing servicers or filing complaints with the Federal Student Aid Ombudsman when issues arise. For example, if a servicer fails to process an employment certification within 60 days, borrowers can escalate the issue to ensure their forgiveness timeline remains intact.

In conclusion, while automatic forgiveness programs are designed to simplify debt relief, the servicer’s role is far from passive. Their accuracy, communication, and compliance with program rules directly impact borrowers’ outcomes. Practical tips include regularly reviewing payment counts, keeping detailed records of employment certifications, and staying informed about program updates. By understanding and engaging with their servicer’s responsibilities, borrowers can navigate the path to forgiveness with greater confidence and control.

Income-Based Repayment and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

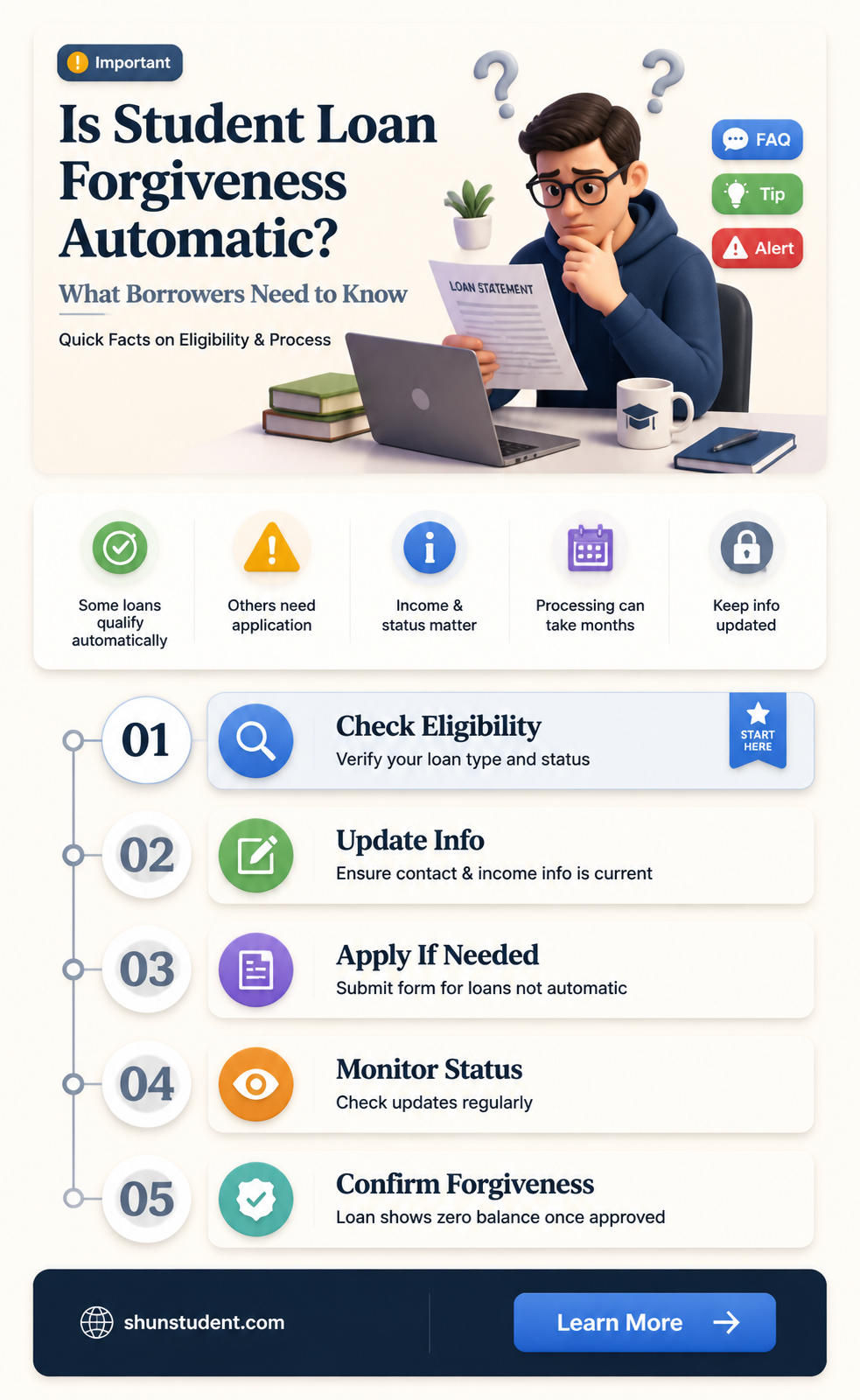

No, student loan forgiveness is not automatic for everyone. Eligibility depends on specific programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, and requires meeting certain criteria and applying for forgiveness.

You typically need to apply for student loan forgiveness. Programs like PSLF or income-driven repayment forgiveness require submitting an application and proving eligibility, even after meeting the required conditions.

No, forgiveness under income-driven repayment plans is not automatic. You must submit an application for forgiveness once you’ve made the required number of qualifying payments (usually 240–300).

In rare cases, such as school closures or total and permanent disability discharge, forgiveness may be automatic after verification. However, most forgiveness programs require an active application process.