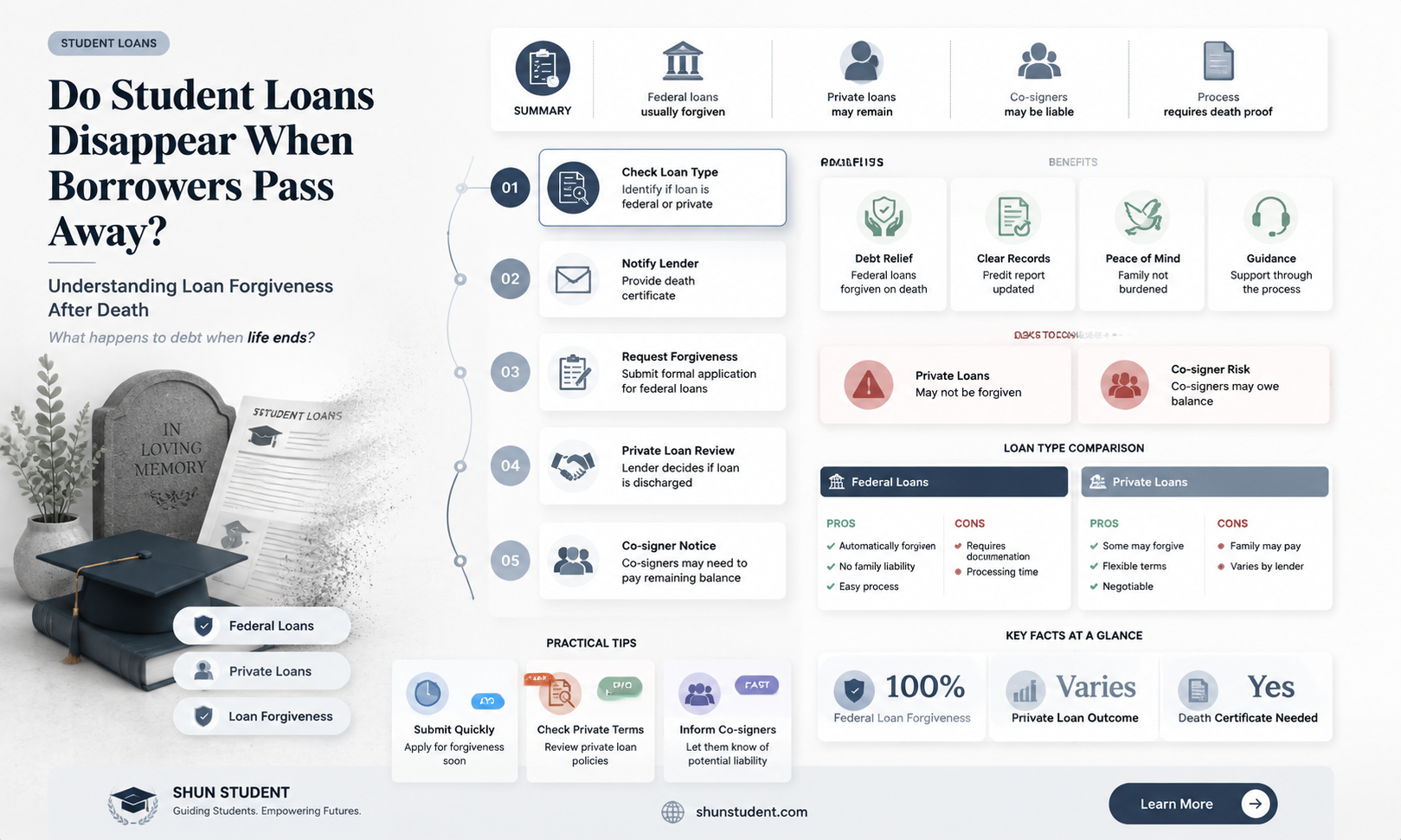

The question of whether student loans are forgiven upon the borrower's death is a critical concern for many individuals and their families. In the United States, the treatment of student loan debt after death depends on the type of loan. Federal student loans, such as Direct Loans and Perkins Loans, are typically discharged if the borrower passes away, relieving the estate and co-signers (if applicable) from the obligation. However, private student loans often have different policies, and forgiveness is not guaranteed; some lenders may require repayment from the borrower's estate or pursue co-signers for the remaining balance. Understanding these distinctions is essential for borrowers and their families to plan accordingly and avoid unexpected financial burdens.

| Characteristics | Values |

|---|---|

| Federal Student Loans (Direct Loans, FFEL, Perkins) | Forgiven upon borrower's death. Co-signers (if any) are released from liability. |

| Private Student Loans | Forgiveness varies by lender. Some lenders forgive the debt, while others may require repayment from the estate or co-signer. |

| Documentation Required | Death certificate must be submitted to the loan servicer or lender. |

| Tax Implications (Federal Loans) | Forgiven debt is not considered taxable income as of the latest tax laws. |

| Tax Implications (Private Loans) | Forgiven debt may be taxable if the lender reports it as income to the IRS. |

| Impact on Co-Signer (Federal Loans) | Co-signer is released from liability. |

| Impact on Co-Signer (Private Loans) | Co-signer may remain liable unless the lender forgives the debt. |

| Estate Liability (Federal Loans) | No liability; debt is discharged. |

| Estate Liability (Private Loans) | Estate may be liable if the lender pursues repayment. |

| Spousal Liability (Federal Loans) | Spouse is not liable for the debt unless they co-signed. |

| Spousal Liability (Private Loans) | Spouse may be liable in community property states or if they co-signed. |

| Notification Process | Family or estate representative must notify the loan servicer or lender. |

| Timeframe for Forgiveness | Typically processed within 30-90 days after documentation is received. |

| Impact on Credit Report | Federal loans are removed from the credit report. Private loans may remain if not forgiven. |

| Recent Legislative Changes | No recent changes affecting forgiveness upon death for federal loans. |

Explore related products

$8.99 $19.95

What You'll Learn

![]()

Federal vs. Private Loan Policies

Federal and private student loans diverge sharply in their policies regarding loan forgiveness upon the borrower's death, creating vastly different outcomes for surviving family members. Federal loans, backed by the government, offer a clear path to discharge. If a borrower with a federal Direct Loan, Perkins Loan, or Federal Family Education Loan (FFEL) passes away, the debt is automatically forgiven. The process requires documentation, such as a death certificate, submitted to the loan servicer. This policy alleviates financial burden for grieving families, ensuring they are not held responsible for the deceased’s educational debt.

Private student loans, however, operate under no such mandate. Lenders are not required by federal law to forgive these loans upon the borrower’s death, and policies vary widely. Some private lenders may discharge the debt as a goodwill gesture, but many will attempt to collect from the borrower’s estate. If the estate lacks sufficient assets, the debt may be passed to a cosigner, if one exists. Without a cosigner, the loan might be written off, but this is not guaranteed. Borrowers with private loans should review their loan agreements or contact their lender to understand specific policies and consider purchasing loan protection insurance if available.

The disparity between federal and private loan policies highlights the importance of proactive planning. For federal loan holders, no additional steps are needed beyond ensuring the loan servicer is notified of the borrower’s death. For private loan holders, however, taking preventive measures is crucial. Adding a cosigner release clause, if possible, can protect loved ones from inheriting the debt. Alternatively, borrowers can explore refinancing options that include death discharge policies, though these are rare. Life insurance policies tailored to cover outstanding student debt are another practical safeguard, especially for borrowers with significant private loan balances.

Understanding these differences empowers borrowers to make informed decisions about their financial futures. Federal loans provide a safety net, while private loans demand vigilance and strategic planning. By reviewing loan terms, considering insurance options, and communicating with lenders, borrowers can minimize the risk of leaving a financial legacy for their families. In the absence of universal forgiveness policies, knowledge and preparation become the most effective tools for navigating this complex landscape.

Does the CARE Act Offer Student Loan Forgiveness? What You Need to Know

You may want to see also

Explore related products

![]()

Discharge Process for Borrowers

Upon the death of a borrower, the discharge process for student loans is a critical yet often overlooked aspect of financial planning. Federal student loans, including Direct Loans, Perkins Loans, and Federal Family Education Loans (FFEL), are typically discharged if the borrower passes away. This means the debt is forgiven, and the borrower’s estate or surviving family members are not held responsible for repayment. However, private student loans operate under different rules, and discharge is not guaranteed. Understanding the steps and requirements for this process is essential for both borrowers and their families.

For federal student loans, the discharge process begins with submitting proof of death to the loan servicer. This typically involves providing a certified copy of the death certificate. Once received, the servicer will initiate the discharge, and any remaining balance will be forgiven. It’s important to act promptly, as delays can lead to unnecessary complications. For example, if the loan is in an automatic payment plan, payments may continue until the discharge is processed, so notifying the servicer immediately is crucial. Additionally, co-signers, if any, are released from liability for federal loans upon the borrower’s death.

Private student loans, on the other hand, require a more nuanced approach. Unlike federal loans, private lenders are not obligated to discharge the debt upon the borrower’s death. However, many lenders have policies in place for forgiveness in such cases. Borrowers or their families must review the loan agreement to determine if death discharge is an option. If it is, they must contact the lender directly and provide the necessary documentation, such as a death certificate. Some states also have laws requiring private student loan discharge, so researching local regulations is advisable. For instance, lenders in states like Virginia and Washington are legally required to forgive private student loans upon the borrower’s death.

A practical tip for borrowers is to maintain organized records of all loan documents, including terms and conditions, and to inform a trusted family member or executor of their estate about the location of these documents. This ensures that the discharge process can be initiated smoothly in the event of death. Additionally, borrowers with private loans may consider purchasing a life insurance policy to cover the debt, providing financial protection for their loved ones. While this adds an extra cost, it can offer peace of mind and prevent financial hardship for survivors.

In conclusion, the discharge process for student loans upon a borrower’s death varies significantly between federal and private loans. Federal loans are automatically forgiven, requiring only proof of death to initiate the process. Private loans, however, depend on the lender’s policies and state laws, making it essential to review loan agreements and take proactive steps, such as maintaining records and considering life insurance. By understanding these differences, borrowers and their families can navigate this challenging process with greater clarity and confidence.

Can Cosigners Benefit from Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Co-Signer Responsibilities After Death

In the event of a borrower's death, co-signers may find themselves unexpectedly entangled in financial obligations. Federal student loans are typically discharged upon the borrower's death, but private loans often lack this safeguard. Co-signers, who agreed to assume responsibility if the borrower defaults, may be held liable for the remaining balance. This harsh reality underscores the importance of understanding the terms of private student loans before committing as a co-signer.

Consider a scenario where a parent co-signs a $50,000 private student loan for their child. If the child passes away, the lender may demand full repayment from the co-signer, regardless of their financial situation. Some lenders offer death discharge policies, but these are not universal. Co-signers should scrutinize loan agreements for clauses related to death or disability, as these can significantly impact their liability. Additionally, purchasing a life insurance policy for the borrower, with the co-signer as a beneficiary, can provide a financial buffer in such tragic circumstances.

From a legal standpoint, co-signers are treated as primary borrowers when the original borrower dies. This means lenders can pursue collection efforts, including wage garnishment or legal action, against the co-signer. To mitigate this risk, co-signers should explore options like loan refinancing or negotiating with the lender for a reduced settlement. Documentation is critical; co-signers should request a formal notice of the borrower’s death and proof of the remaining balance to ensure transparency in the repayment process.

Persuasively, co-signers must proactively protect themselves before tragedy strikes. Discussing the possibility of death with the borrower, though uncomfortable, is essential for financial planning. Co-signers should also consider consulting an attorney to understand their rights and potential liabilities. While federal loans offer automatic discharge, private loans require vigilance and strategic planning to avoid becoming a lifelong financial burden.

In conclusion, co-signer responsibilities after a borrower’s death are complex and often unforgiving, particularly with private student loans. By understanding loan terms, exploring protective measures, and seeking legal advice, co-signers can navigate this challenging terrain with greater confidence and preparedness.

Can Federal Student Loans Be Forgiven? Exploring Options for Relief

You may want to see also

Explore related products

![]()

Tax Implications for Heirs

Upon the death of a student loan borrower, the tax implications for heirs can be complex and depend heavily on the type of loan and the jurisdiction involved. For federal student loans, the debt is typically discharged, meaning heirs are not responsible for repayment. However, private student loans may not offer the same forgiveness, and lenders could seek repayment from the borrower’s estate. This distinction is critical because it directly influences the tax treatment of any forgiven debt or assets used for repayment.

When federal student loans are discharged due to the borrower’s death, the forgiven amount is generally not considered taxable income for the heir or the estate. This provision, introduced in the Tax Cuts and Jobs Act of 2017, applies through December 31, 2025, unless extended by Congress. For example, if a borrower with a $50,000 federal student loan passes away, the discharge of this debt would not trigger a taxable event for the heir. However, heirs should retain documentation of the discharge to substantiate this tax treatment if audited.

In contrast, private student loans may not be forgiven upon the borrower’s death, and lenders could pursue repayment from the estate. If the estate lacks sufficient assets, the lender might write off the debt as uncollectible. In such cases, the forgiven debt could be treated as taxable income to the estate, increasing its tax liability. For instance, if a private student loan of $30,000 is written off, the estate might owe taxes on this amount, reducing the net value available for distribution to heirs.

Heirs can take proactive steps to mitigate tax implications. First, they should verify the type of student loan (federal or private) and review the loan agreement for death discharge provisions. Second, consulting a tax professional or estate attorney can provide clarity on potential tax liabilities and strategies to minimize them. Third, heirs should ensure the estate’s tax returns accurately reflect any forgiven debt, especially for private loans. Practical tips include keeping detailed records of loan types, discharge notices, and correspondence with lenders or servicers.

Ultimately, understanding the tax implications for heirs when a borrower dies requires careful consideration of loan type, jurisdictional rules, and proactive planning. While federal student loans offer clear relief from both repayment and taxation, private loans demand vigilance to avoid unexpected tax burdens. By staying informed and seeking expert guidance, heirs can navigate this complex landscape with greater confidence and financial security.

Does Student Loan Forgiveness Include Private Loans? Key Facts Explained

You may want to see also

Explore related products

![]()

Documentation Required for Forgiveness

In the event of a borrower's death, federal student loans are typically discharged, offering a measure of financial relief to grieving families. However, this process is not automatic; it requires specific documentation to initiate the loan forgiveness. The first critical step is obtaining an official death certificate, which serves as the primary evidence of the borrower's passing. This document must be a certified copy, issued by the relevant government authority, and should clearly state the date and cause of death. Without this essential proof, loan servicers cannot proceed with the forgiveness process, leaving the estate or co-signers potentially liable for the debt.

The next crucial piece of documentation is the loan account information. Survivors or representatives must provide details such as the loan account number, the name of the loan servicer, and the type of federal loan (e.g., Direct Loan, FFEL Program loan). This information is vital for the servicer to locate the specific loan and begin the discharge process. It is advisable to gather all loan statements and correspondence related to the debt to ensure a smooth and efficient application. In some cases, a simple phone call to the loan servicer can help identify the exact documents needed, as requirements may vary slightly depending on the loan type.

For private student loans, the process can be more complex and less forgiving. Many private lenders do offer death discharge, but the terms are often outlined in the loan agreement. Here, the documentation may include not only the death certificate but also the original loan contract, which specifies the conditions under which the loan can be forgiven. Some lenders might require additional proof, such as a letter from the executor of the estate or a court-appointed representative, to ensure the request is legitimate. It is essential to review the loan agreement carefully and contact the lender directly to understand their specific requirements.

A common challenge in this process is the potential for delays or rejections due to incomplete or incorrect documentation. To avoid this, it is recommended to create a comprehensive checklist of required documents. This checklist should include the death certificate, loan account details, and any additional forms provided by the loan servicer or lender. For federal loans, the U.S. Department of Education provides a specific form for death discharge, which must be completed accurately. Ensuring all information is up-to-date and correctly filled out can significantly expedite the forgiveness process, providing much-needed closure during a difficult time.

In summary, while the death of a student loan borrower can lead to loan forgiveness, the process demands careful attention to documentation. From official death certificates to detailed loan information and specific forms, each piece of paperwork plays a critical role. Understanding these requirements and preparing the necessary documents can help survivors navigate this challenging process with greater ease, ensuring that financial burdens do not add to the emotional strain of loss.

Stafford Loan Forgiveness: Eligibility and Options Explained

You may want to see also

Frequently asked questions

Yes, federal student loans are discharged upon the borrower's death. The loan servicer will require proof of death, such as a death certificate, to process the discharge.

It depends on the lender's policy. Some private lenders may forgive the loan upon death, while others may require repayment from the borrower's estate. Check the loan agreement or contact the lender for details.

For federal student loans, cosigners are released from liability upon the borrower's death. For private loans, it depends on the lender's policy—some may hold cosigners responsible, while others may discharge the debt.

For federal student loans, forgiven debt due to death is not considered taxable income. However, for private loans, forgiven debt may be taxable depending on the lender's policies and IRS regulations. Consult a tax professional for specific guidance.