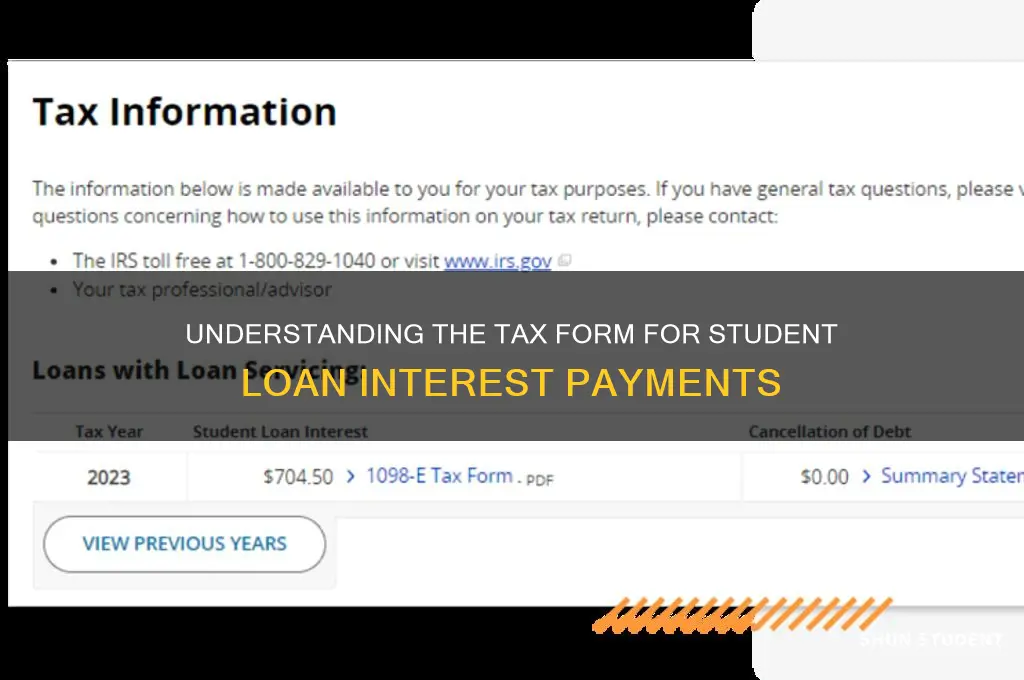

When it comes to filing taxes, understanding which forms to use can be crucial, especially for those who have paid student loan interest throughout the year. The specific tax form for reporting student loan interest paid is Form 1098-E, Student Loan Interest Statement. This form is provided by the lender and includes details such as the amount of interest paid during the tax year, which may be eligible for a tax deduction. Taxpayers can then use this information when filing their federal income tax return, typically on Schedule 1 (Form 1040), to claim the Student Loan Interest Deduction, potentially reducing their taxable income by up to $2,500, depending on their income level and other eligibility criteria.

| Characteristics | Values |

|---|---|

| Tax Form | IRS Form 1098-E (Student Loan Interest Statement) |

| Purpose | Reports student loan interest paid during the tax year |

| Issuer | Lender or loan servicer |

| Threshold for Issuance | Issued if $600 or more in interest was paid during the tax year |

| Filing Requirement | Not required to file with the IRS; keep for tax records |

| Tax Benefit | Allows taxpayers to claim the Student Loan Interest Deduction (up to $2,500) |

| Eligibility for Deduction | Available to taxpayers with modified adjusted gross income (MAGI) below certain limits |

| MAGI Limits (2023) | Phaseout begins at $75,000 ($155,000 for married filing jointly) |

| Deduction Phaseout Range (2023) | $75,000 - $90,000 ($155,000 - $185,000 for married filing jointly) |

| Qualified Loans | Loans taken for qualified education expenses (tuition, fees, etc.) |

| Non-Qualified Loans | Loans from family members or non-eligible educational loans |

| Where to Report on Tax Return | Line 21 of Schedule 1 (Form 1040) |

| Documentation Needed | Form 1098-E or statement from lender showing interest paid |

| Availability | Sent by lenders by January 31st of the following tax year |

| Electronic Access | Often available online through the lender’s portal |

| Retention Period | Keep with tax records for at least 3 years |

Explore related products

What You'll Learn

- Form 1098-E Overview: Details interest paid on qualified student loans, issued by lenders to borrowers

- Eligibility Criteria: Requirements for claiming the student loan interest deduction on taxes

- Deduction Limits: Maximum amount deductible annually based on income and filing status

- Filing Instructions: How to report student loan interest on your federal tax return

- Common Mistakes: Errors to avoid when claiming the student loan interest deduction

![]()

Form 1098-E Overview: Details interest paid on qualified student loans, issued by lenders to borrowers

Form 1098-E is a tax document specifically designed to report the interest paid on qualified student loans during the tax year. Issued by lenders to borrowers, this form is crucial for taxpayers who wish to claim the Student Loan Interest Deduction on their federal income tax return. The deduction allows eligible borrowers to reduce their taxable income by up to $2,500, depending on their income level and filing status. Form 1098-E provides the necessary information to support this deduction, ensuring compliance with IRS requirements.

The form includes key details such as the borrower’s name, address, and taxpayer identification number (TIN), as well as the lender’s name and TIN. Most importantly, it lists the total amount of interest paid on the student loan during the tax year. This figure is reported in Box 1 of the form. Borrowers should receive Form 1098-E from their lender by January 31 of the following year if they paid at least $600 in student loan interest. If the interest paid is less than $600, the lender may still provide the form or the borrower can request it.

To qualify for the deduction, the student loan must meet specific IRS criteria. It must have been taken out solely to pay for qualified higher education expenses, such as tuition, fees, books, and room and board, for the borrower, their spouse, or dependents. Additionally, the loan must have been used for education provided at an eligible institution. Form 1098-E does not determine eligibility for the deduction but serves as proof of the interest paid, which is a critical component of the deduction claim.

When filing taxes, borrowers should transfer the amount from Box 1 of Form 1098-E to their Schedule 1 (Form 1040) and then to their Form 1040. The IRS uses this information to verify the accuracy of the claimed deduction. It’s important to keep Form 1098-E and other related documents for at least three years in case of an audit or further review by the IRS. Properly utilizing Form 1098-E can help borrowers maximize their tax benefits while ensuring they remain in compliance with tax laws.

In summary, Form 1098-E is an essential tool for student loan borrowers seeking to claim the Student Loan Interest Deduction. It provides a clear record of the interest paid on qualified loans, issued by lenders to borrowers, and is a key document in the tax filing process. By understanding and accurately using Form 1098-E, borrowers can take full advantage of available tax benefits while maintaining proper documentation for IRS purposes.

Understanding UK Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Eligibility Criteria: Requirements for claiming the student loan interest deduction on taxes

To claim the student loan interest deduction on your taxes, you must meet specific eligibility criteria outlined by the Internal Revenue Service (IRS). This deduction allows taxpayers to reduce their taxable income by up to $2,500 for interest paid on qualified student loans during the tax year. The first requirement is that the loan must be a qualified student loan, which is defined as a loan taken out solely to pay for qualified higher education expenses. These expenses include tuition, fees, room and board, books, supplies, and other necessary costs for the taxpayer, their spouse, or dependents, at an eligible institution. Loans from related parties, such as family members, or qualified employer plans are not eligible for this deduction.

Another critical eligibility criterion is the taxpayer’s income level. The student loan interest deduction is subject to income phaseout limits, meaning the amount you can deduct decreases as your modified adjusted gross income (MAGI) increases. For the tax year 2023, single filers with a MAGI of more than $75,000 and joint filers with a MAGI of more than $155,000 begin to phase out of eligibility. Single filers with a MAGI exceeding $90,000 and joint filers with a MAGI exceeding $185,000 cannot claim the deduction at all. It’s essential to calculate your MAGI accurately to determine if you qualify for the full deduction, a partial deduction, or none at all.

The taxpayer’s filing status also plays a role in eligibility. If you are married, you must file a joint return to claim the deduction; married taxpayers filing separately are not eligible. Additionally, the taxpayer must be legally obligated to pay the interest on the student loan. This means that if a parent pays interest on a loan that is legally their child’s responsibility, the parent cannot claim the deduction. The deduction is only available to the person who is legally required to repay the loan.

Furthermore, the student loan must be in the taxpayer’s name, or the funds must have been used for a dependent’s qualified education expenses. If a parent takes out a loan in their name for their child’s education, the parent can claim the deduction, provided they meet all other eligibility criteria. However, if the child is no longer a dependent and takes over the loan payments, the child becomes eligible to claim the deduction instead.

Lastly, the educational institution where the loan funds were used must be an eligible institution. This includes most accredited public, nonprofit, and privately owned for-profit postsecondary institutions. The institution must participate in the federal student aid programs administered by the U.S. Department of Education. Loans used for education at institutions that do not meet these criteria are not eligible for the interest deduction. Understanding these requirements ensures that taxpayers can accurately determine their eligibility and properly claim the student loan interest deduction on their tax return, typically reported on Form 1040, Schedule 1.

Understanding the Current Student Plus Loan Interest Rate

You may want to see also

Explore related products

![]()

Deduction Limits: Maximum amount deductible annually based on income and filing status

When it comes to claiming a deduction for student loan interest paid, taxpayers must be aware of the deduction limits imposed by the IRS. The maximum amount deductible annually is not a fixed figure but rather depends on the taxpayer's income and filing status. For the tax year 2023, the student loan interest deduction begins to phase out for taxpayers with a modified adjusted gross income (MAGI) above $70,000 ($140,000 for married filing jointly). The deduction is completely phased out for single filers with a MAGI above $85,000 and married filing jointly with a MAGI above $170,000. Taxpayers whose income falls within these phase-out ranges can still claim a partial deduction, but the amount will be reduced based on their income level.

The deduction limit is further influenced by the taxpayer's filing status, with married filing jointly taxpayers eligible for a higher maximum deduction than single filers. For those who qualify, the maximum deductible amount is $2,500 per year, but this figure is subject to the phase-out rules mentioned earlier. It's essential to calculate the deduction carefully, taking into account the taxpayer's MAGI and filing status to ensure compliance with IRS regulations. Taxpayers can use the IRS's Student Loan Interest Deduction Worksheet to help determine their eligible deduction amount.

For taxpayers with incomes below the phase-out thresholds, the $2,500 maximum deduction can provide significant tax savings. However, it's crucial to note that the deduction is limited to the actual amount of interest paid during the tax year, up to the $2,500 cap. If a taxpayer pays less than $2,500 in student loan interest, their deduction will be limited to the actual amount paid. Additionally, the deduction is only available for interest paid on qualified student loans, which include loans taken out for the taxpayer, their spouse, or their dependent's education expenses.

Taxpayers who are married but filing separately are not eligible for the student loan interest deduction, regardless of their income level. This is an essential consideration for couples who may be considering their filing status options. Furthermore, the deduction is not available for taxpayers who are claimed as dependents on someone else's tax return. It's also worth noting that the student loan interest deduction is an above-the-line deduction, meaning it can be claimed even if the taxpayer does not itemize their deductions.

To claim the student loan interest deduction, taxpayers must complete Form 1040 or Form 1040-SR and attach Schedule 1. The deduction is reported on line 20 of the form, with the actual interest paid amount entered on line 1 of Schedule 1. Taxpayers should receive a Form 1098-E from their loan servicer, which reports the total interest paid during the tax year. It's essential to keep accurate records of student loan interest payments and to ensure that the deduction is calculated correctly to avoid any potential issues with the IRS. By understanding the deduction limits and eligibility requirements, taxpayers can maximize their tax savings and minimize their tax liability.

Understanding Student Loan Interest Rates: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![]()

Filing Instructions: How to report student loan interest on your federal tax return

When filing your federal tax return, reporting student loan interest paid during the tax year can help you claim the Student Loan Interest Deduction, which may reduce your taxable income. The primary tax form used for this purpose is Form 1098-E, Student Loan Interest Statement. This form is provided by your loan servicer if you paid $600 or more in student loan interest during the year. Even if you don’t receive a Form 1098-E, you can still report the interest paid if it’s less than $600, using your loan statements or online account records.

To begin, gather all necessary documentation, including Form 1098-E or your loan statements. On your federal tax return, the student loan interest deduction is claimed on Schedule 1 (Form 1040), Line 21. This line is specifically designated for reporting deductible student loan interest. If you’re using tax software, it will guide you through entering the information from Form 1098-E or your records. Ensure the amount you enter matches the total interest paid as reported on Form 1098-E or your loan statements to avoid discrepancies.

Next, transfer the amount from Schedule 1, Line 21, to Form 1040, Line 16. This integrates the deduction into your overall tax return, potentially lowering your taxable income. It’s important to note that the Student Loan Interest Deduction is an above-the-line deduction, meaning you can claim it even if you don’t itemize deductions. However, there are income limits and eligibility criteria, so review IRS guidelines to ensure you qualify. For example, as of the latest tax year, the deduction begins to phase out for single filers with modified adjusted gross income (MAGI) above $70,000 and is completely phased out at $85,000.

If you’re married filing jointly, the phaseout range is $140,000 to $170,000. Additionally, the loan must have been used for qualified higher education expenses, and the borrower must be legally obligated to repay the debt. Dependents cannot claim this deduction if someone else (such as a parent) claims them as a dependent on their tax return. Double-check these requirements to ensure eligibility before filing.

Finally, review your completed tax return for accuracy before submitting it. Errors in reporting student loan interest can delay processing or trigger IRS inquiries. If you’re unsure about any step, consider consulting a tax professional or using reputable tax software to guide you through the process. Properly reporting student loan interest can provide valuable tax savings, so take the time to ensure it’s done correctly.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Common Mistakes: Errors to avoid when claiming the student loan interest deduction

When claiming the student loan interest deduction, taxpayers often encounter pitfalls that can lead to errors or missed opportunities. One common mistake is failing to use the correct tax form, which is Form 1040 or Form 1040-SR, along with Schedule 1. The student loan interest deduction is reported on line 21 of Schedule 1, which then transfers to your main tax return. Using outdated forms or omitting Schedule 1 entirely can result in the deduction being overlooked or rejected by the IRS. Always ensure you’re using the most current version of these forms to avoid complications.

Another frequent error is misunderstanding the eligibility requirements for the deduction. Not all student loans qualify, and the interest paid must be for a loan used exclusively for qualified higher education expenses. For example, consolidating a qualified student loan with a personal loan can disqualify the interest from being deductible. Additionally, the deduction is phased out for taxpayers with higher incomes, so failing to check the income limits can lead to incorrect claims. Verify that your loan and financial situation meet all IRS criteria before claiming the deduction.

Taxpayers often overlook the importance of accurate documentation. Lenders are required to send Form 1098-E, which reports the amount of interest paid during the tax year. However, if you don’t receive this form or if the amount is incorrect, it’s your responsibility to obtain the correct information. Claiming the wrong amount of interest can trigger IRS scrutiny or result in a denied deduction. Keep detailed records of your loan payments and interest statements to ensure accuracy.

A common oversight is claiming interest paid by someone else. For example, if a parent pays the interest on a child’s student loan, the child cannot claim the deduction unless they are legally obligated to repay the loan. Similarly, if an employer reimburses the interest as part of an employee benefit, it cannot be deducted. Understanding who is legally responsible for the loan and who paid the interest is crucial to avoiding this mistake.

Lastly, failing to consider the impact of other tax credits or deductions can lead to errors. For instance, if you claim the American Opportunity Tax Credit or the Lifetime Learning Credit for the same student in the same year, you cannot deduct the interest paid on loans for that student’s qualified expenses. Double-dipping on benefits is not allowed, and attempting to do so can result in penalties. Carefully review your tax situation to ensure you’re maximizing benefits without violating IRS rules.

By avoiding these common mistakes—using the wrong forms, misunderstanding eligibility, lacking proper documentation, claiming ineligible interest, and overlooking conflicts with other credits—taxpayers can confidently and accurately claim the student loan interest deduction. Always double-check your information and consider consulting a tax professional if you’re unsure about any aspect of the process.

Understanding the Refundable Student Loan Interest Amount: A Comprehensive Guide

You may want to see also

Frequently asked questions

The tax form for reporting student loan interest paid is Form 1098-E, Student Loan Interest Statement. This form is provided by the lender and includes the amount of interest paid during the tax year.

No, you do not need to attach Form 1098-E to your tax return. However, you should keep it for your records and use the information it provides to claim the Student Loan Interest Deduction on Schedule 1 (Form 1040).

If you don’t receive Form 1098-E by January 31, contact your loan servicer to request it. If you still cannot obtain it, you can report the interest paid using your loan statements or other documentation, but ensure the amount is accurate to avoid issues with the IRS.