The student loan interest tax credit is a valuable financial benefit designed to help borrowers manage the cost of their education debt. Available to eligible taxpayers, this credit allows individuals to reduce their federal tax liability by a portion of the interest paid on qualified student loans during the tax year. Unlike a deduction, which lowers taxable income, the student loan interest tax credit directly reduces the amount of tax owed, providing more immediate relief. To qualify, borrowers must meet specific income requirements and have loans used for higher education expenses. Understanding this credit can help students and graduates maximize their savings while navigating the challenges of repaying student loans.

| Characteristics | Values |

|---|---|

| Definition | A tax credit that allows eligible taxpayers to deduct a portion of the interest paid on qualified student loans from their taxable income. |

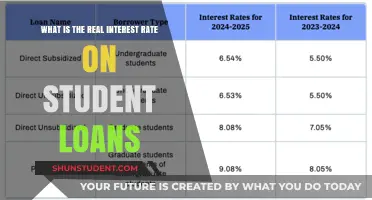

| Maximum Credit Amount (2023) | $2,500 per year. |

| Income Phaseout Range (2023) | Single filers: $75,000 - $90,000; Joint filers: $150,000 - $180,000. |

| Eligibility Requirements | Must have paid interest on a qualified student loan during the tax year. |

| Loan Eligibility | Loans must be for qualified higher education expenses (tuition, fees, etc.). |

| Tax Credit Type | Non-refundable (reduces tax liability but cannot result in a refund). |

| Claimed on Tax Form | IRS Form 1040, using Schedule 1. |

| Carryforward Option | Unused credit cannot be carried forward to future tax years. |

| Dependents Exclusion | If claimed as a dependent, the dependent cannot claim the credit. |

| Loan Purpose | Must be used for the taxpayer, spouse, or dependent's education. |

| Tax Year Applicability | Applies to the tax year in which the interest was paid. |

| Adjusted Gross Income (AGI) Limit | Credit phases out completely above the income phaseout range. |

| Qualified Education Expenses | Includes tuition, fees, room, board, books, supplies, and equipment. |

| Loan Exclusions | Does not apply to loans from family members or qualified employer plans. |

Explore related products

What You'll Learn

- Eligibility requirements for claiming the student loan interest tax credit

- Maximum deductible amount for student loan interest paid annually

- Income limits affecting eligibility for the tax credit

- Differences between student loan interest deduction and credit

- How to claim the credit on federal tax returns?

![]()

Eligibility requirements for claiming the student loan interest tax credit

The student loan interest tax credit is a non-refundable tax credit that allows eligible taxpayers to claim a portion of the interest paid on their student loans, reducing their overall tax liability. To claim this credit, taxpayers must meet specific eligibility requirements set by the Internal Revenue Service (IRS). One primary requirement is that the taxpayer must have paid interest on a qualified student loan during the tax year. Qualified student loans are those taken out solely to pay for eligible higher education expenses, such as tuition, fees, books, supplies, and room and board, for the taxpayer, their spouse, or dependents. Loans from related parties, such as family members, or qualified employer plans are not eligible for this credit.

To be eligible for the student loan interest tax credit, the taxpayer must also meet specific income requirements. As of the latest guidelines, the credit phases out for taxpayers with modified adjusted gross income (MAGI) above certain thresholds. For single filers, the phase-out begins at a specific MAGI level and is completely phased out at a higher level. Married couples filing jointly have a higher phase-out range. It is essential for taxpayers to calculate their MAGI accurately, as this determines their eligibility and the amount of credit they can claim. Taxpayers whose MAGI exceeds the upper limit are not eligible for the credit.

Another critical eligibility requirement is that the taxpayer must be legally obligated to pay the student loan interest. This typically means the loan is in the taxpayer's name, or they are a spouse or parent who has taken out the loan for a dependent. If a parent pays interest on a loan that is legally the child's responsibility, the child is considered the borrower for tax purposes, and only they can claim the credit. Additionally, the student loan must have been used for qualified education expenses during an academic period for which the student was enrolled at least half-time in a program leading to a degree, certificate, or other recognized credential.

The taxpayer claiming the credit must also have been enrolled in an eligible institution during the academic period covered by the loan. Eligible institutions include most accredited public, non-profit, and privately owned for-profit postsecondary institutions. The institution must participate in the federal student aid programs administered by the U.S. Department of Education. If the loan was used for a student who attended an ineligible institution or was not enrolled at least half-time, the interest paid on that loan does not qualify for the credit.

Lastly, the taxpayer cannot claim the student loan interest tax credit if they (or their spouse, if filing jointly) can be claimed as a dependent on someone else’s tax return. This rule ensures that the credit is not double-claimed by both the taxpayer and the person claiming them as a dependent. Additionally, the taxpayer must file their federal tax return using Form 1040 and complete Schedule 1 to calculate the credit. Meeting all these eligibility requirements is essential for successfully claiming the student loan interest tax credit and maximizing potential tax savings.

Maximizing Tax Savings: Standard Deduction for Single Student Loan Interest

You may want to see also

Explore related products

![]()

Maximum deductible amount for student loan interest paid annually

The student loan interest tax credit is a valuable benefit for borrowers who are repaying their student loans, allowing them to reduce their taxable income by a portion of the interest paid on their loans. This credit is designed to ease the financial burden of student loan repayment, particularly for those in the early stages of their careers. When it comes to the maximum deductible amount for student loan interest paid annually, it’s important to understand the limits set by the IRS. As of the most recent guidelines, borrowers can deduct up to $2,500 of the interest paid on qualified student loans each year. This amount is not a reimbursement but rather a dollar-for-dollar reduction in taxable income, which can lower the overall tax liability.

To qualify for this deduction, the interest paid must be on a loan taken out solely for qualified higher education expenses, such as tuition, fees, books, and room and board. The loan must also be used for the borrower, their spouse, or a dependent. Additionally, the borrower’s income plays a crucial role in determining eligibility for the full deduction. For the tax year 2023, the deduction begins to phase out for single filers with a modified adjusted gross income (MAGI) above $75,000 and is completely phased out for those earning more than $90,000. For married couples filing jointly, the phaseout begins at $155,000 and ends at $185,000. Understanding these income thresholds is essential to maximize the benefit of the deduction.

It’s worth noting that the maximum deductible amount of $2,500 is not automatically applied; borrowers must meet specific criteria to claim it. For instance, the borrower must be legally obligated to pay the interest, and the loan must be used for eligible educational expenses during an academic period for the borrower, their spouse, or a dependent. If the borrower’s parents paid the interest on a loan taken out in the borrower’s name, the IRS considers it as if the borrower paid the interest, making it eligible for the deduction. However, if the borrower is claimed as a dependent on someone else’s tax return, they cannot claim the deduction.

Another important aspect is that the $2,500 maximum is a combined limit for all qualified student loan interest paid during the year. If a borrower has multiple student loans, the total interest paid across all loans cannot exceed this cap for the deduction. Additionally, the deduction is claimed as an adjustment to income on Form 1040, meaning it can be taken even if the borrower does not itemize deductions. This makes it a particularly useful tool for reducing taxable income for borrowers who take the standard deduction.

Lastly, while the maximum deductible amount for student loan interest paid annually is fixed at $2,500, the actual benefit varies depending on the taxpayer’s marginal tax rate. For example, a borrower in the 22% tax bracket could save up to $550 ($2,500 × 0.22) on their federal taxes by claiming the full deduction. Borrowers should keep detailed records of their student loan interest payments, as lenders are required to send Form 1098-E, which reports the amount of interest paid during the year. This form is essential for accurately claiming the deduction and ensuring compliance with IRS rules. By staying informed about these details, borrowers can make the most of the student loan interest tax credit and reduce their tax burden effectively.

Discovering New Horizons: The Most Fascinating Aspect of Student Life

You may want to see also

Explore related products

![]()

Income limits affecting eligibility for the tax credit

The student loan interest tax credit, officially known as the Student Loan Interest Deduction (SLID), allows eligible taxpayers to deduct up to $2,500 of the interest paid on qualified student loans from their taxable income. However, eligibility for this tax credit is significantly influenced by income limits set by the IRS. Understanding these income thresholds is crucial, as exceeding them can reduce or eliminate the deduction entirely. For single filers, the phase-out begins at a modified adjusted gross income (MAGI) of $70,000 and is completely phased out at $85,000. For married couples filing jointly, the phase-out starts at $140,000 and ends at $170,000. These limits are adjusted periodically, so taxpayers should verify the current figures each tax year.

For taxpayers whose income falls within the phase-out range, the deduction is gradually reduced based on a formula provided by the IRS. For example, if a single filer has a MAGI of $75,000, they are halfway through the phase-out range and would be eligible for half of the maximum $2,500 deduction. Taxpayers with incomes above the upper limits of the phase-out range are not eligible for the deduction at all. It’s important to note that these income limits apply to MAGI, which is your adjusted gross income (AGI) with certain deductions added back in, such as foreign earned income exclusions.

Married couples filing separately are not eligible for the student loan interest deduction, regardless of their income level. This restriction underscores the importance of choosing the appropriate filing status when claiming tax credits or deductions. Additionally, dependents whose parents claim them on their tax returns are also ineligible for the deduction, even if their income falls below the phase-out thresholds. These rules ensure that the tax benefit is targeted toward taxpayers who bear the primary responsibility for repaying student loans.

Taxpayers should also be aware that the income limits for the student loan interest deduction are not tied to inflation adjustments like some other tax provisions. As a result, the thresholds may remain unchanged for several years, potentially affecting more taxpayers as incomes rise over time. To maximize eligibility, individuals nearing the phase-out range may consider strategies such as contributing to retirement accounts or timing income and deductions to lower their MAGI. Consulting a tax professional can provide personalized guidance tailored to individual financial situations.

Lastly, it’s essential to distinguish between the student loan interest deduction and other education-related tax credits, such as the American Opportunity Tax Credit (AOTC) or Lifetime Learning Credit (LLC), which have their own income limits and eligibility criteria. While the SLID focuses solely on interest paid, these credits are designed to offset tuition and other educational expenses. Taxpayers may be eligible for multiple education-related benefits, but careful planning is required to ensure compliance with all applicable rules and income limits. Understanding these distinctions can help taxpayers optimize their tax savings while remaining within the bounds of IRS regulations.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Differences between student loan interest deduction and credit

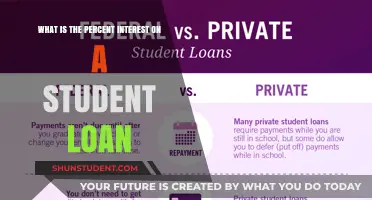

The student loan interest tax credit and the student loan interest deduction are both tax benefits designed to help borrowers manage the cost of their student loans, but they operate differently and offer distinct advantages. Understanding the differences between these two options is crucial for maximizing your tax savings.

Eligibility and Application: One of the primary distinctions lies in how these benefits are applied to your tax return. The student loan interest deduction is an above-the-line deduction, meaning you can claim it even if you don't itemize your deductions. This makes it accessible to a broader range of taxpayers. To qualify, you must have paid interest on a qualified student loan during the tax year, and your income must be below certain thresholds. The deduction can reduce your taxable income by up to $2,500, depending on your income and filing status. On the other hand, the student loan interest credit is a non-refundable tax credit, which directly reduces the amount of tax you owe, dollar for dollar. This credit is claimed using Form 8863 and is subject to specific eligibility criteria, including income limits and the requirement that the loan was used for qualified education expenses.

Impact on Tax Liability: The way these benefits impact your tax liability is another key difference. A tax deduction reduces your taxable income, which in turn lowers the amount of income subject to tax. This can result in a smaller tax bill or a larger refund, but the actual savings depend on your tax bracket. For instance, if you're in the 22% tax bracket, a $2,500 deduction would save you $550. In contrast, a tax credit provides a dollar-for-dollar reduction in the tax you owe. If you qualify for a $2,500 credit, your tax liability decreases by the full $2,500, which can be more beneficial, especially for those in lower tax brackets.

Income Limits and Phase-outs: Both benefits have income limits, but they differ in how they are applied. The student loan interest deduction starts to phase out for taxpayers with modified adjusted gross incomes (MAGI) above certain thresholds, which vary by filing status. For example, for single filers, the deduction is gradually reduced and eventually eliminated as income increases. The credit, however, has a different set of income limits, and once your income exceeds these limits, you are no longer eligible for the credit. These limits are also adjusted annually for inflation.

Qualified Expenses and Loans: While both benefits are related to student loan interest, the types of loans and expenses that qualify differ. The deduction generally applies to interest paid on any qualified student loan, including loans for undergraduate, graduate, and professional degrees. The credit, however, is more restrictive. It applies only to interest paid on loans for qualified education expenses during an academic period for which the student was enrolled at least half-time. This includes tuition, fees, and other required expenses, but not living expenses or transportation.

In summary, the student loan interest deduction and credit offer different approaches to providing tax relief for student loan borrowers. The deduction is more widely accessible and reduces taxable income, while the credit directly lowers tax liability but has stricter eligibility requirements. Understanding these differences can help borrowers make informed decisions when filing their taxes and potentially save more on their student loan expenses.

Understanding the Phase-Out of Student Loan Interest Deduction: What You Need to Know

You may want to see also

Explore related products

$13.9 $25

![]()

How to claim the credit on federal tax returns

The Student Loan Interest Deduction is a valuable tax benefit that allows eligible taxpayers to deduct up to $2,500 of the interest paid on qualified student loans from their taxable income. To claim this credit on your federal tax returns, you must meet certain criteria and follow specific steps. First, ensure that you have paid interest on a qualified student loan during the tax year. Qualified loans include those taken out for higher education expenses, such as tuition, fees, room, and board, for yourself, your spouse, or your dependents. Private loans, federal loans, and refinanced loans may all qualify, but the loan must have been used exclusively for educational expenses.

To begin the claiming process, gather all necessary documentation, including Form 1098-E, which is provided by your loan servicer and details the amount of interest paid during the year. If you do not receive this form and have paid at least $600 in interest, you can still claim the deduction by contacting your loan servicer for the required information. Additionally, have your income records ready, as your eligibility and the amount you can deduct may be phased out if your modified adjusted gross income (MAGI) exceeds certain thresholds. For the tax year 2023, the phase-out begins at $70,000 for single filers and $140,000 for married filing jointly, with the deduction completely phased out at $85,000 and $170,000, respectively.

When filing your federal tax return, use Form 1040 or Form 1040-SR, and attach Schedule 1 to report the student loan interest deduction. On Schedule 1, line 21, enter the amount of student loan interest you paid during the year, as shown on Form 1098-E or your loan servicer’s statement. Ensure that the amount does not exceed $2,500, as this is the maximum deductible amount. If you are claiming the deduction for the first time or have changed loan servicers, double-check that the interest reported is accurate and corresponds to qualified educational loans.

It’s important to note that you cannot claim the student loan interest deduction if you (or your spouse, if filing jointly) can be claimed as a dependent on someone else’s tax return. Additionally, the loan must have been used for eligible educational expenses during an academic period for which the student was enrolled at least half-time in a program leading to a degree, certificate, or other recognized credential. If you meet all eligibility requirements, claiming this deduction can reduce your taxable income, potentially lowering your overall tax liability.

Finally, consider using tax preparation software or consulting a tax professional to ensure accuracy and maximize your benefits. These resources can help you navigate the complexities of tax laws, confirm your eligibility, and identify any additional credits or deductions you may qualify for. By carefully following these steps and staying organized, you can successfully claim the student loan interest deduction on your federal tax returns and take full advantage of this valuable tax benefit.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Frequently asked questions

The student loan interest tax credit is a non-refundable tax credit that allows eligible taxpayers to reduce their federal income tax liability by a portion of the interest paid on qualified student loans during the tax year.

Eligibility depends on factors like income, filing status, and whether the loan was used for qualified education expenses. Generally, single filers with modified adjusted gross income (MAGI) below a certain threshold and those who paid interest on eligible student loans can claim the credit.

The maximum credit is $2,500 per year, but the actual amount depends on your income and the interest paid. The credit is phased out for higher-income taxpayers, and it cannot exceed the total interest paid during the year.