Student loan interest rates are a critical factor in determining the overall cost of borrowing for education, as they directly impact the total amount repaid over the life of the loan. These rates can vary widely depending on the type of loan—federal or private—as well as the borrower's creditworthiness, repayment plan, and current economic conditions. Federal student loans typically offer fixed rates set by the government, while private loans often feature variable rates tied to market indices, making them more susceptible to fluctuations. Understanding the spread, or range, of these interest rates is essential for students and families to make informed decisions, minimize long-term debt, and choose the most affordable financing options for their educational goals.

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Rates

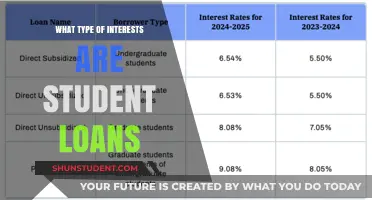

When considering student loans, one of the most critical factors to evaluate is the interest rate, as it significantly impacts the total cost of borrowing. Federal and private student loans offer different interest rate structures, and understanding the spread between these rates is essential for making informed financial decisions. Federal student loans, which are issued by the U.S. Department of Education, typically offer fixed interest rates that are set by Congress. These rates are often lower than those of private loans and are designed to be more accessible and affordable for students. For the 2023-2024 academic year, for example, undergraduate federal loans carry an interest rate of 5.5%, while graduate loans are at 7.05%, and PLUS loans (for parents and graduate students) are at 8.05%. These rates are standardized and do not fluctuate based on the borrower's credit history.

In contrast, private student loans are offered by banks, credit unions, and other financial institutions, and their interest rates can vary widely. Private loan rates are often variable, meaning they can change over time based on market conditions. Additionally, these rates are heavily influenced by the borrower's credit score and financial history. Borrowers with excellent credit may qualify for rates that are competitive with or even lower than federal loan rates, but those with poor or limited credit history often face significantly higher rates, sometimes reaching double digits. This variability creates a wide spread between the lowest and highest private loan rates, making federal loans a more predictable and often more affordable option for many students.

Another key difference between federal and private loan rates is the availability of borrower benefits and protections. Federal student loans come with advantages such as income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options, which can provide financial relief in times of hardship. These benefits are not typically offered with private loans, which generally have stricter repayment terms and fewer options for borrowers facing financial difficulties. The added security and flexibility of federal loans often justify their slightly higher rates compared to the best private loan offers, especially for borrowers with uncertain future income prospects.

The spread between federal and private loan rates can also be influenced by market trends and economic conditions. During periods of low interest rates, private lenders may offer more competitive rates, narrowing the gap with federal loans. However, when interest rates rise, private loan rates can increase substantially, widening the spread and making federal loans even more attractive. Prospective borrowers should monitor these trends and consider the long-term implications of choosing between fixed federal rates and variable private rates.

In summary, the spread between federal and private student loan interest rates is shaped by factors such as rate stability, borrower eligibility, and available protections. Federal loans provide consistent, lower fixed rates and valuable benefits, making them a safer choice for most students. Private loans, while potentially offering lower rates to well-qualified borrowers, come with higher risks due to variable rates and fewer safeguards. When evaluating student loan options, borrowers should carefully consider their financial situation, creditworthiness, and long-term goals to determine which type of loan best meets their needs.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Fixed vs. Variable Interest Types

When considering student loans, one of the most critical decisions borrowers face is choosing between fixed and variable interest rates. This choice significantly impacts the total cost of the loan over its lifetime. Fixed interest rates remain constant throughout the loan term, providing predictability and stability in monthly payments. For example, if a student loan has a fixed interest rate of 5%, the borrower will pay 5% interest every year until the loan is repaid, regardless of market fluctuations. This type of rate is ideal for borrowers who prefer a consistent repayment plan and want to avoid surprises in their budgeting.

On the other hand, variable interest rates fluctuate based on market conditions, typically tied to an index like the London Interbank Offered Rate (LIBOR) or the Prime Rate. Initially, variable rates may start lower than fixed rates, making them an attractive option for borrowers seeking lower upfront costs. However, this comes with the risk of rates increasing over time, potentially leading to higher monthly payments. For instance, if the market index rises, the interest rate on the loan will increase accordingly, which could make repayment more challenging, especially for borrowers on tight budgets.

The spread in student loan interest rates refers to the difference between the fixed and variable rates offered by lenders. This spread can vary widely depending on economic conditions, the lender’s policies, and the borrower’s creditworthiness. For example, during periods of low market interest rates, the spread between fixed and variable rates may narrow, making variable rates more appealing. Conversely, in a rising interest rate environment, the spread may widen, making fixed rates a safer choice to lock in lower costs.

Choosing between fixed and variable rates depends on the borrower’s risk tolerance and financial outlook. Borrowers who expect to repay their loans quickly or anticipate falling interest rates may benefit from variable rates. However, those who prefer long-term financial stability or predict rising interest rates should opt for fixed rates. It’s essential to analyze personal financial goals, market trends, and the potential long-term impact of each rate type before making a decision.

Lastly, refinancing options can provide flexibility for borrowers who initially choose variable rates but later wish to switch to fixed rates, or vice versa. Many lenders offer refinancing programs that allow borrowers to adjust their interest rate type based on changing financial circumstances or market conditions. Understanding the nuances of fixed and variable rates, as well as the spread between them, empowers borrowers to make informed decisions that align with their financial needs and goals.

Exploring Student Interest: How Many Are Drawn to Computer Science?

You may want to see also

Explore related products

$6.99

![]()

Credit Score Impact on Rates

When it comes to understanding the spread of student loan interest rates, one of the most critical factors influencing the rates borrowers receive is their credit score. Lenders use credit scores to assess the risk associated with lending money, and this risk assessment directly impacts the interest rates offered. Generally, student loans can be categorized into two main types: federal and private. Federal student loans, which are issued by the government, typically have fixed interest rates that are not heavily dependent on the borrower's credit score. However, private student loans, offered by banks, credit unions, and other financial institutions, are highly influenced by the borrower's creditworthiness.

A higher credit score often translates to lower interest rates on private student loans. This is because a strong credit score indicates to lenders that the borrower has a history of managing debt responsibly and is less likely to default on the loan. For instance, borrowers with excellent credit scores (typically above 750) may qualify for interest rates that are significantly lower than those with fair or poor credit scores. Conversely, individuals with lower credit scores (below 650) may face higher interest rates, sometimes with additional fees or stricter repayment terms. The spread between the lowest and highest interest rates offered can be substantial, often ranging from 3% to 12% or more, depending on the lender and market conditions.

It’s important for borrowers to understand how their credit score impacts the interest rate spread. For example, a borrower with a credit score of 780 might secure a private student loan with an interest rate of 4%, while someone with a credit score of 620 could be offered the same loan at 9%. This 5% difference in interest rates can add up to thousands of dollars in additional costs over the life of the loan. Therefore, improving one’s credit score before applying for a private student loan can be a strategic move to secure more favorable terms.

Another aspect to consider is the role of cosigners in mitigating the impact of a low credit score. If a borrower has a poor credit score, adding a cosigner with a strong credit history can help qualify for a lower interest rate. The lender will consider the cosigner’s creditworthiness in addition to the borrower’s, effectively reducing the perceived risk. However, this approach also means the cosigner is equally responsible for the loan, which can have implications for their own credit and financial health.

In summary, credit scores play a pivotal role in determining the interest rates on private student loans, creating a wide spread between rates offered to borrowers with excellent credit versus those with poor credit. Federal student loans, while less dependent on credit scores, still offer standardized rates that are generally lower than private options. Borrowers should prioritize building and maintaining a strong credit profile to access the most competitive rates, potentially saving significant amounts in interest over time. Understanding this relationship between credit scores and interest rates is essential for making informed decisions about student loan financing.

Understanding the Federal Student Loan Interest Paid Tax Form

You may want to see also

Explore related products

![]()

Subsidized vs. Unsubsidized Loans

When considering student loans, understanding the difference between subsidized and unsubsidized loans is crucial, especially in the context of interest rates and their long-term financial impact. Both types of loans are part of the federal student loan program, but they differ significantly in how interest accrues and who is responsible for paying it. This distinction directly affects the total cost of borrowing and repayment strategies.

Subsidized loans are need-based and offer a significant advantage: the government pays the interest on the loan while the borrower is in school at least half-time, during the grace period after graduation (typically six months), and during any approved deferment periods. This means the loan balance does not increase during these times, making subsidized loans a more affordable option for eligible students. Interest rates for subsidized loans are fixed and determined annually by the federal government, typically ranging from 4% to 6% in recent years. For example, as of 2023, the interest rate for undergraduate subsidized loans is 4.99%. The key benefit here is that borrowers avoid interest capitalization, which can save hundreds or even thousands of dollars over the life of the loan.

In contrast, unsubsidized loans are available to all students regardless of financial need, but the borrower is responsible for paying the interest from the moment the loan is disbursed. If the borrower chooses not to pay the interest while in school, during the grace period, or during deferment, the unpaid interest is capitalized—added to the principal balance of the loan. This increases the total amount owed and the overall cost of the loan. Unsubsidized loans also have fixed interest rates, which are slightly higher than subsidized loans for undergraduate students (e.g., 4.99% for undergraduates and 6.54% for graduates as of 2023). The spread between subsidized and unsubsidized loan rates is minimal for undergraduates but widens for graduate students, making unsubsidized loans more expensive over time.

The choice between subsidized and unsubsidized loans depends on eligibility and financial strategy. Subsidized loans are ideal for borrowers who qualify based on financial need, as they minimize long-term costs by avoiding interest capitalization. Unsubsidized loans, while accessible to all, require careful consideration of the borrower’s ability to manage accruing interest. For instance, paying even a small amount of interest monthly while in school can significantly reduce the total repayment amount.

In summary, the spread in interest rates between subsidized and unsubsidized loans is modest for undergraduates but becomes more pronounced for graduate students. However, the primary difference lies in interest accrual and capitalization. Subsidized loans offer a financial cushion by pausing interest charges during specific periods, while unsubsidized loans require proactive management to prevent interest from compounding. Borrowers should prioritize subsidized loans when possible and carefully evaluate the long-term costs of unsubsidized options. Understanding these nuances ensures informed decision-making and more manageable student debt.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Current Market Rate Trends

As of the latest data, current market rate trends for student loan interest rates reflect a dynamic interplay between federal and private lending sectors, influenced by broader economic conditions, particularly Federal Reserve policies and inflationary pressures. Federal student loan interest rates, which are set annually based on the 10-year Treasury note auction, have seen upward adjustments in recent years. For the 2023-2024 academic year, undergraduate federal loans carry a fixed rate of 5.5%, while graduate loans are at 7.05%, and PLUS loans for parents and graduate students are at 8.05%. These rates represent a significant increase from the previous year, driven by the Federal Reserve’s aggressive rate hikes to combat inflation.

In the private student loan market, interest rates are variable and highly dependent on the borrower’s creditworthiness and the lender’s terms. Current trends show private loan rates ranging from approximately 4.5% to 14%, with variable rates often starting lower than fixed rates but carrying the risk of increasing over time. The spread between federal and private loan rates has widened, with federal loans generally offering more competitive fixed rates for borrowers with limited credit history. However, private loans may provide lower rates for borrowers with excellent credit, making them a viable option for refinancing or supplementing federal aid.

Economic indicators, such as inflation and unemployment rates, continue to influence student loan interest rates. As inflation remains elevated, lenders are pricing in higher risks, leading to increased borrowing costs. Additionally, the Federal Reserve’s monetary policy decisions directly impact the cost of borrowing, with rate hikes translating to higher student loan rates. Borrowers are advised to monitor these trends closely, as they can significantly affect long-term repayment obligations.

Another notable trend is the growing popularity of refinancing as a strategy to manage student loan debt. With federal rates rising, borrowers with strong credit profiles are exploring private refinancing options to secure lower rates. However, refinancing federal loans into private ones means losing access to federal benefits like income-driven repayment plans and loan forgiveness programs, so borrowers must weigh these trade-offs carefully.

Looking ahead, market analysts predict that student loan interest rates may stabilize or even decrease if inflation eases and the Federal Reserve pauses rate hikes. However, borrowers should remain proactive in understanding their loan terms and exploring options to minimize interest costs. Staying informed about current market rate trends is essential for making strategic financial decisions in the evolving landscape of student loan borrowing and repayment.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Frequently asked questions

As of the most recent update, federal student loan interest rates range from 4.99% to 7.54%, depending on the type of loan (e.g., undergraduate, graduate, PLUS loans) and the borrower's status (e.g., subsidized vs. unsubsidized).

Private student loan interest rates vary widely, typically ranging from 3% to 14% or more, depending on the lender, the borrower's creditworthiness, and market conditions. They can be lower or higher than federal rates but often lack the flexible repayment options and protections of federal loans.

Federal student loans have fixed interest rates, meaning the rate remains the same for the life of the loan. Private student loans can offer both fixed and variable rates, with variable rates fluctuating based on market indices like the LIBOR or Prime Rate.

For federal student loans, credit scores do not impact the interest rate, as rates are set by Congress. For private student loans, a higher credit score generally qualifies you for lower interest rates, while a lower score may result in higher rates or the need for a cosigner.